The right way to draw down on retirement savings

Stave off retirement ruin with some quick math

Advertisement

Stave off retirement ruin with some quick math

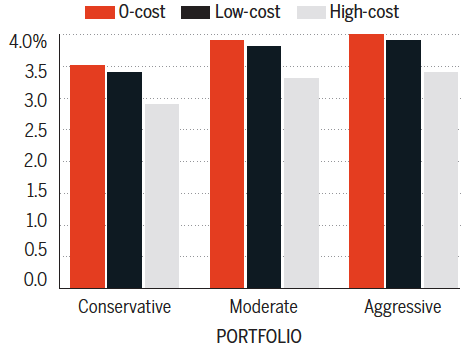

Notes: This figure models expense ratios of 0% (for 0-cost), and 0.25% (for low-cost), and 1.25% (for high-cost). This figure’s projections, generated by the Vanguard Capital Markets Model, are based in U.S. dollars as of December 31, 2011, and assume an 85% overall portfolio success rate.

Source: Vanguard

Jonathan Chevreau is Founder of the Financial Independence hub and co-author of Victory Lap Retirement. Read more of his Retired Money column here.

Notes: This figure models expense ratios of 0% (for 0-cost), and 0.25% (for low-cost), and 1.25% (for high-cost). This figure’s projections, generated by the Vanguard Capital Markets Model, are based in U.S. dollars as of December 31, 2011, and assume an 85% overall portfolio success rate.

Source: Vanguard

Jonathan Chevreau is Founder of the Financial Independence hub and co-author of Victory Lap Retirement. Read more of his Retired Money column here.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Artificial intelligence is best at overcoming the friction that stops you from taking up new pursuits, users insist.

Could moving your RRIF into segregated funds lower estate taxes? Maybe—but higher fees and other trade-offs could leave your...

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving benefits, and...

We check in on some champions of early retirement nearing their own finish line of financial independence.

What inflation, investment return, and life expectancy assumptions should Canadians use for retirement planning? Here’s what financial planners recommend.

The Saskatchewan Pension Plan gives Canadians another way to save for retirement, with low fees, locked-in contributions, and...

The FIRE movement promises early retirement, but high costs and income realities make it difficult. Here’s what the math...

Experts explore whether financial independence is compatible with long-term travel, highlighting remote work, geoarbitrage, and cost-efficient “bleisure” lifestyles.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...