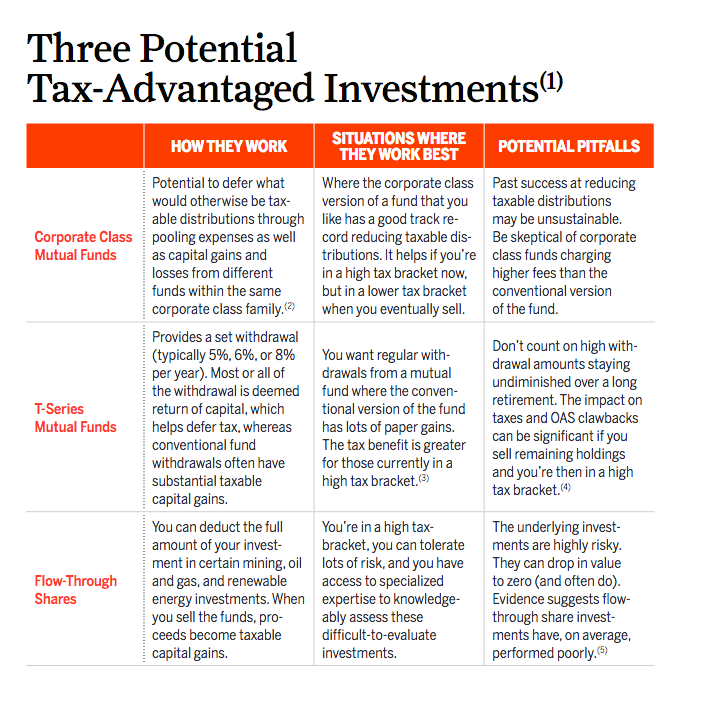

3 investments that ease your tax burden

In non-registered accounts, consider how each investment treats taxable income

Advertisement

In non-registered accounts, consider how each investment treats taxable income

Notes: (1) When investing in non-registered accounts. (2) Until Dec. 31, 2016, corporate class shares can also avoid triggering immediate taxable capital gains when switching funds within the same corporate class family. (3) Generally you can switch from the conventional version of the fund to the T-series version of the same fund without triggering a tax event. If a conventional fund doesn’t have much unrealized capital gains, or you expect to be in a high tax bracket when you sell the remaining fund holdings, then setting up a Systematic Withdrawal Plan (SWP) for a conventional fund might be a good alternative. (4) Generally the set withdrawal rates apply to the net asset value at the end of the previous year. A high withdrawal rate like 8% stands a strong chance of outpacing fund returns and so tends to diminish fund balances, in which case the 8% withdrawal rate would be applied to a diminishing balance. You also should monitor the adjusted cost base (ACB). Return of capital withdrawals lower the ACB. In some situations, the ACB could eventually go to zero, after which all withdrawals would be in the form of taxable capital gains. If the ACB gets close to zero, often it is a good idea to stop withdrawals to avoid triggering taxable capital gains, if you can afford to do so. (5) Several studies have shown that, on average, investors in flow-through shares would have been better off just investing in the corresponding resource stock market indexes, even after accounting for the sizable tax advantage of the flow-through shares. One such study is Rates of Return on Flow-Through Shares: Investors and Governments Beware by Vijay Jog, University of Calgary School of Public Policy research paper, February 2016.

Notes: (1) When investing in non-registered accounts. (2) Until Dec. 31, 2016, corporate class shares can also avoid triggering immediate taxable capital gains when switching funds within the same corporate class family. (3) Generally you can switch from the conventional version of the fund to the T-series version of the same fund without triggering a tax event. If a conventional fund doesn’t have much unrealized capital gains, or you expect to be in a high tax bracket when you sell the remaining fund holdings, then setting up a Systematic Withdrawal Plan (SWP) for a conventional fund might be a good alternative. (4) Generally the set withdrawal rates apply to the net asset value at the end of the previous year. A high withdrawal rate like 8% stands a strong chance of outpacing fund returns and so tends to diminish fund balances, in which case the 8% withdrawal rate would be applied to a diminishing balance. You also should monitor the adjusted cost base (ACB). Return of capital withdrawals lower the ACB. In some situations, the ACB could eventually go to zero, after which all withdrawals would be in the form of taxable capital gains. If the ACB gets close to zero, often it is a good idea to stop withdrawals to avoid triggering taxable capital gains, if you can afford to do so. (5) Several studies have shown that, on average, investors in flow-through shares would have been better off just investing in the corresponding resource stock market indexes, even after accounting for the sizable tax advantage of the flow-through shares. One such study is Rates of Return on Flow-Through Shares: Investors and Governments Beware by Vijay Jog, University of Calgary School of Public Policy research paper, February 2016.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The GST quick method can simplify tax reporting for small businesses—but it’s not right for everyone. Here’s who qualifies...

Changes to Canada’s Disability Tax Credit will make it easier to qualify, reduce CRA red tape, and expand access...

You might be missing valuable tax credits, deductions, and filing opportunities. Here are nine ways to maximize your tax...

Tax instalments can be confusing. Learn how the CRA calculates quarterly payments, when you can adjust them, and how...

How Canadians with disabilities can navigate tax season, including credits, deductions, and programs that can help offset higher costs...

Your CRA My Account may hold uncashed cheques, credits, and tax info you’ve missed. Here are 5 key areas...

Filing your taxes isn’t just a requirement—it’s the first step to accessing benefits, credits, and financial opportunities in Canada....

Make the most of your 2026 tax refund with smart strategies to pay down debt and build savings, so...

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...