Why I’m not opening a joint bank account with my husband-to-be

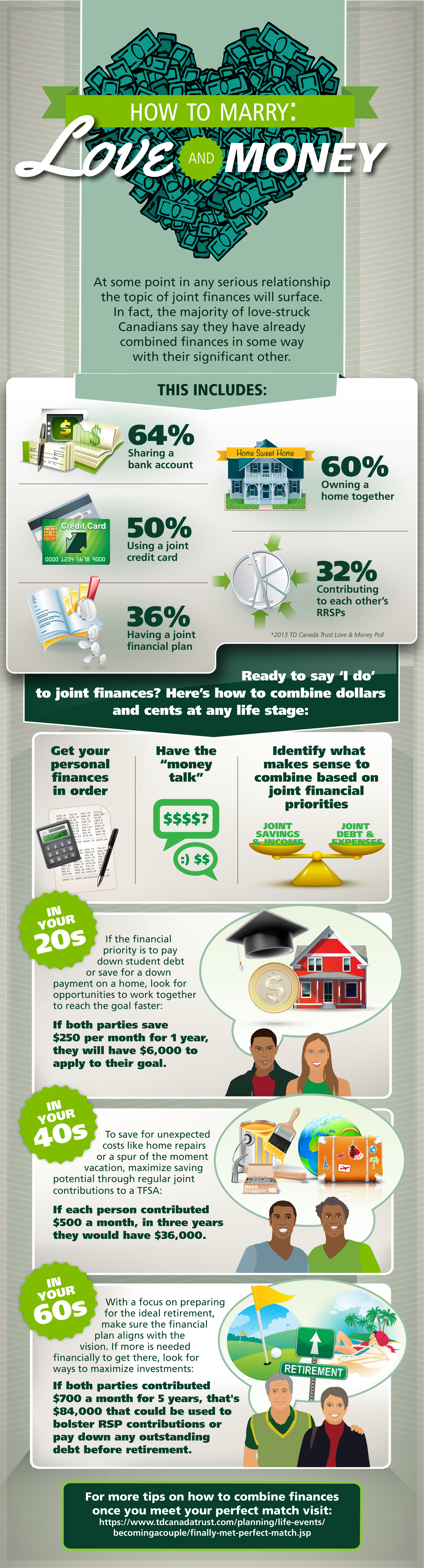

We've chosen not to go the route of 64% of couples.

Advertisement

We've chosen not to go the route of 64% of couples.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The latest earnings reports for Canadian investors from the cybersecurity and convenience-store giants.

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

Created By

Ratehub

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Good news for Canadian investors in these apparel and grocery companies, as both report higher earnings and sales.