A leaner portfolio for better results

Consider using low-cost index mutual funds

Advertisement

Consider using low-cost index mutual funds

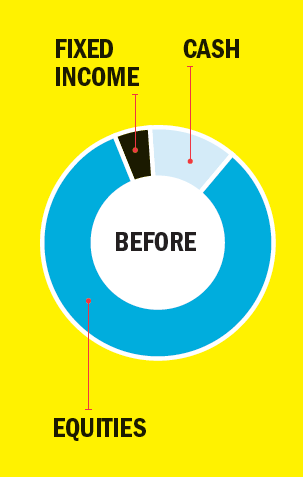

Mark Morin, 29, is a Montreal mining engineer who started building his five-figure portfolio with resource stocks back in 2010. When those didn’t perform well, he added several Canadian and U.S. blue-chip stocks as well as some equity mutual funds. His total holdings now include more than 30 investments—including stock in 25 different U.S. and Canadian companies. About 60% of his holdings are in RRSPs and the remainder in TFSAs and non-registered accounts. Just recently, Mark started building a new portfolio with TD’s e-Series funds. “I’m spread too thin,” he says. “I want something simpler and more cost-effective.”

Mark Morin, 29, is a Montreal mining engineer who started building his five-figure portfolio with resource stocks back in 2010. When those didn’t perform well, he added several Canadian and U.S. blue-chip stocks as well as some equity mutual funds. His total holdings now include more than 30 investments—including stock in 25 different U.S. and Canadian companies. About 60% of his holdings are in RRSPs and the remainder in TFSAs and non-registered accounts. Just recently, Mark started building a new portfolio with TD’s e-Series funds. “I’m spread too thin,” he says. “I want something simpler and more cost-effective.” Investment adviser Shannon Dalziel of PWL Capital agrees Mark needs a simpler and more broadly based portfolio for the long term. She advises he reduce his number of holdings and increase his exposure to global markets by investing in low-cost, broadly diversified exchange-traded funds (ETFs) or index mutual funds. Since Mark is already on the right track with the TD e-Series funds in his RRSP, Dalziel suggests he continue along this path and build a full portfolio with these funds in all of his registered and non-registered accounts. While the TD e-Series funds have a slightly higher management expense ratio (MER) than comparable ETFs, there are no trading fees. “Buying and selling is straightforward,” says Dalziel.

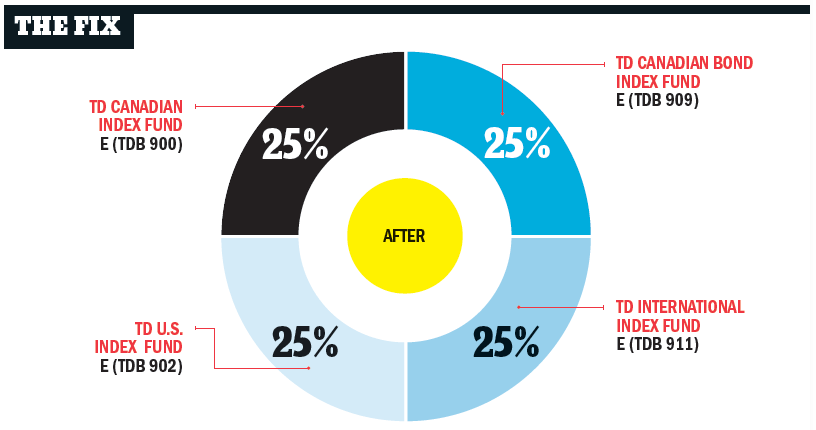

Because Mark has a long time horizon, she also recommends he consider an aggressive portfolio split as follows: 25% in fixed income, 25% in Canadian equities, 25% in U.S. equities and 25% in international equities. (Using TD e-Series funds, the average underlying MER of this portfolio is just 0.42%.)

Mark needs to be careful about asset location, too. The e-Series bond fund, which is fully taxable, should be held entirely in his RRSP. The Canadian index fund should go in his non-registered account to maximize the Canadian dividend tax credit. All remaining equity funds can go in his RRSP and TFSA.

Finally, Mark should meet with a tax accountant to understand the implications of selling his non-registered stocks. “It may be best just to bite the bullet and sell everything at once and start his portfolio over again from scratch,” says Dalziel.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Investment adviser Shannon Dalziel of PWL Capital agrees Mark needs a simpler and more broadly based portfolio for the long term. She advises he reduce his number of holdings and increase his exposure to global markets by investing in low-cost, broadly diversified exchange-traded funds (ETFs) or index mutual funds. Since Mark is already on the right track with the TD e-Series funds in his RRSP, Dalziel suggests he continue along this path and build a full portfolio with these funds in all of his registered and non-registered accounts. While the TD e-Series funds have a slightly higher management expense ratio (MER) than comparable ETFs, there are no trading fees. “Buying and selling is straightforward,” says Dalziel.

Because Mark has a long time horizon, she also recommends he consider an aggressive portfolio split as follows: 25% in fixed income, 25% in Canadian equities, 25% in U.S. equities and 25% in international equities. (Using TD e-Series funds, the average underlying MER of this portfolio is just 0.42%.)

Mark needs to be careful about asset location, too. The e-Series bond fund, which is fully taxable, should be held entirely in his RRSP. The Canadian index fund should go in his non-registered account to maximize the Canadian dividend tax credit. All remaining equity funds can go in his RRSP and TFSA.

Finally, Mark should meet with a tax accountant to understand the implications of selling his non-registered stocks. “It may be best just to bite the bullet and sell everything at once and start his portfolio over again from scratch,” says Dalziel.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?