When to tap into government pensions

Take them early or defer? Here’s how to get the most out of OAS and CPP

Advertisement

Take them early or defer? Here’s how to get the most out of OAS and CPP

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Retirement Club for Canadians offers a sounding board and resources for people who manage retirement finance all on their...

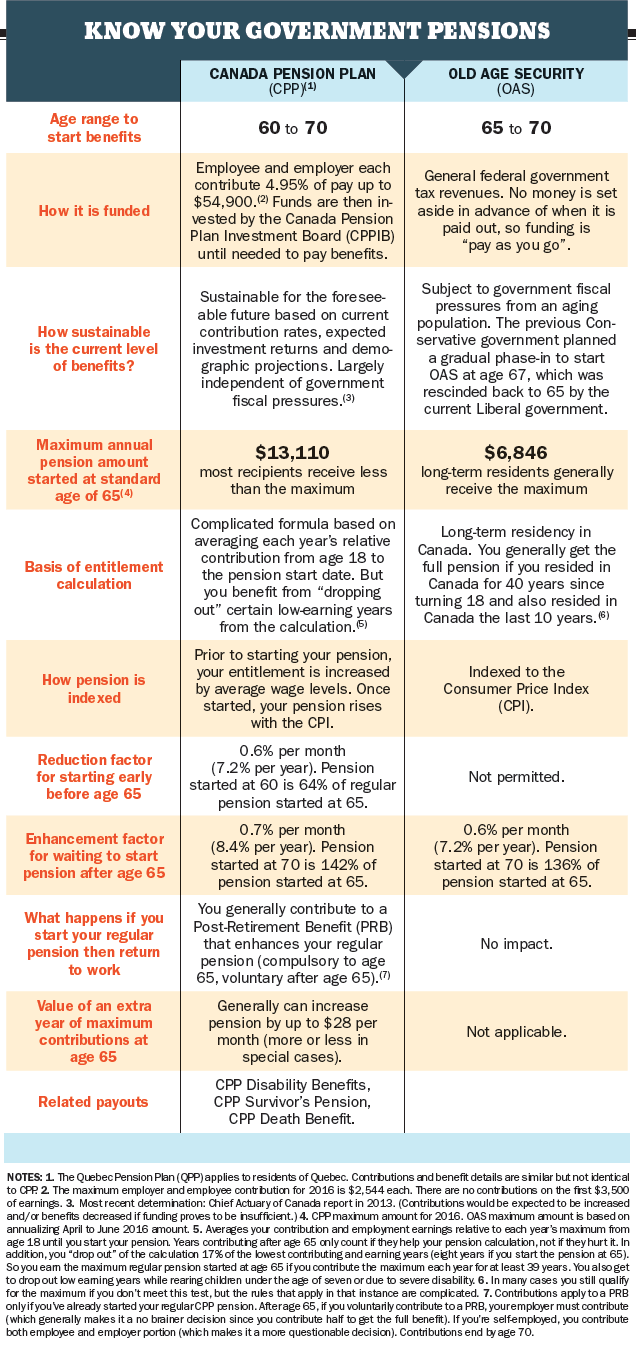

Here’s how Canada’s Old Age Security pension works, who’s eligible for OAS, when you can start receiving OAS, and...

The benefits of depleting savings to avoid estate taxes depends on many variables. But if you live a decade...

Should you hold equities? Fixed income? An annuity? Or all three? Financial advisors debate the options in today’s “tariffied”...

Some Canadian seniors enter retirement without savings or run out of money over time. Here’s how they can stay...

Here’s how Canada’s retirement pension plan works, who’s eligible for CPP, when you can start receiving CPP, and CPP...

There’s more than one way to optimize your income after retiring. Some strategies can boost wealth, and others may...

The senior vice president of retail and wealth at Meridian shares the importance of budgeting and investing in your...

Here are two ways to manage the effects of tariffs in Canada, plus three statements to prepare to ensure...

If I have an employer pension that I will begin at age 65 will my govt pensions be clawed back. I am recieving cpp disability’s now due to cancer and I was told that would continue to age 75. At age 65 I expect to start recieving OAS if I’m still alive and my union pension. What’s the best way to receive the most amount of earnings without being penalized?

Due to the large volume of comments we receive, we regret that we are unable to respond directly to each one. We invite you to email your question to [email protected], where it will be considered for a future response by one of our expert columnists. For personal advice, we suggest consulting with your financial institution or a qualified advisor.