Income splitting, higher TFSA limits coming: Reports

New fitness tax credits also expected ahead of election

Advertisement

New fitness tax credits also expected ahead of election

READ: Income splitting: A three-billion dollar promise »

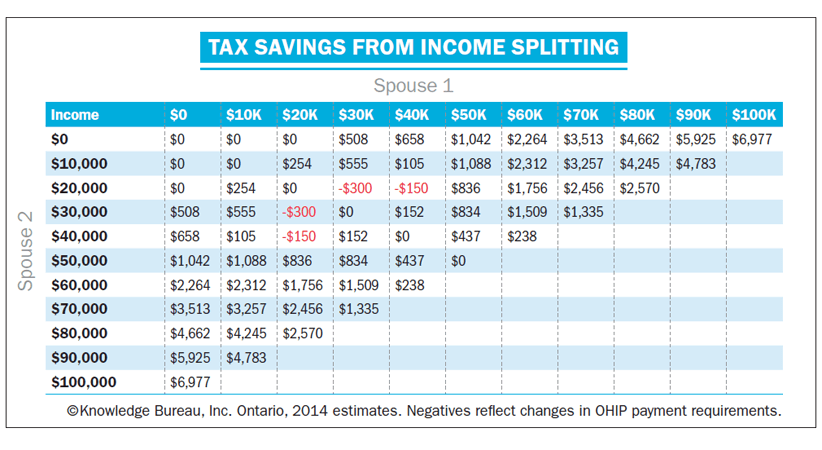

Income splitting a boon to families »

The Conservatives also promised to up the existing annual TFSA contribution limit from $5,500 to $10,000, the Post said. The Child Fitness Tax Credit is also expected to double to $1,000 and an adult fitness tax credit introduced to cover up to $500 in registration fees.

Full details will be made available in the fall fiscal update, scheduled for later this month—approximately one year ahead of the next federal election.

READ: Income splitting: A three-billion dollar promise »

Income splitting a boon to families »

The Conservatives also promised to up the existing annual TFSA contribution limit from $5,500 to $10,000, the Post said. The Child Fitness Tax Credit is also expected to double to $1,000 and an adult fitness tax credit introduced to cover up to $500 in registration fees.

Full details will be made available in the fall fiscal update, scheduled for later this month—approximately one year ahead of the next federal election.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

Most registered retirement savings plans are eventually converted to registered retirement income funds. Here’s what to know about RRIF...

Learn about Canada’s carbon tax, launched in 2019 and ended in 2025.

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

The hidden costs of doing it alone: Why Canadian DIY investors should consider guidance from a professional planner.

If you have tax-free savings accounts in Canadian and U.S. dollars, here’s how to avoid overcontributing.

Direct deposit puts tax refunds, benefits and other government payments into your bank account faster. Here’s how to sign...