How the new 10% minimum down payment works

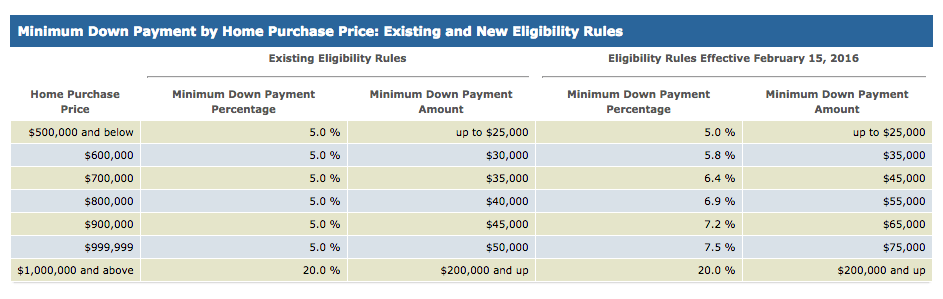

We crunched the numbers to figure out the new graduated system for homes over $500,000

Advertisement

We crunched the numbers to figure out the new graduated system for homes over $500,000

| House Price | 2015 Minimum Down Payment Required | 2016 Minimum Down Payment Required |

| $500,000 | 5% = $25,000 | 5% = $25,000 |

| $800,000 | 5% = $40,000 | 5% on first $500,000 = $25,000 + 10% on next $300,000 = $30,000, for a total DP of $55,000 |

→ delay buying to save more

→ purchase a cheaper home

→ try and get secondary funding (either through the bank of mom and dad, or through higher-interest financing)

“There’s been a number of moves, over the last few years, in an attempt to regulate Canada’s housing market,” says Richards. “CMHC has already increased its mortgage default insurance premiums twice in 24 months; they’ve increased the down payment on homes worth $1 million or more to 20% and they increased the down payment made on rentals to 20%—and none of these changes have really cooled Canada’s two hot housing markets. Today’s announcement was a much less severe change, so it’s doubtful it will have a huge impact.” The Department of Finance released this chart that illustrates how the new minimum down payment breaks out: Read more from Romana King at Home Owner on Facebook »

Read more from Romana King at Home Owner on Facebook »

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Thinking about selling a property that’s not currently your primary residence? Knowing its value is essential to calculating—and not...

Home sales are down, prices are softening, and buyers are hesitant—but conditions may be shifting as summer gains momentum.

CMHC Eco Plus is a new program that encourages Canadian home buyers to opt for energy efficiency. Here’s how...

Condo owners hoping to buy a house are stuck in a stalled market as sales in Canada continue to...

CMHC says rents in some major cities are easing due to increased supply and slower immigration, but renters are...

A MoneySense reader asks about survivor benefits for spouses. Here’s how defined benefit and CPP survivor payments work in...

Created By

Ratehub

If you’re thinking about buying your first recreational property, now may be the right time. Here's what to know.

We’ve put together all the tools and strategies you need to manage the shock of renewing your home loan...

If you’re worried about a recession in Canada, you’re not alone. Here’s what to expect and how you can...