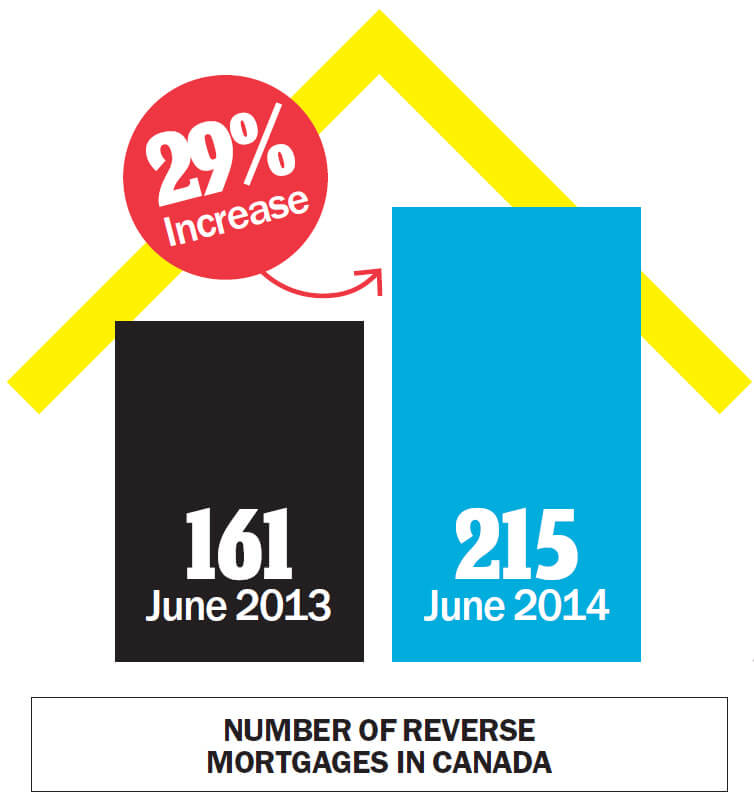

Why there’s a sudden surge in reverse mortgages

Soaring home prices likely to blame

Advertisement

Soaring home prices likely to blame

Source: HomEquityBank

Source: HomEquityBank

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Whether for income or day trading, these ETFs are more complex and potentially risky products than they first appear....

As the cost of living climbs, financial help from family and increased credit use are becoming survival strategies for...

Thinking about selling a property that’s not currently your primary residence? Knowing its value is essential to calculating—and not...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

The co-founder of online prenuptial agreement startup Jointly talks about leaving Big Law, tracking spending as a system, and...