Growth fund manager overweight in European stocks

TGF has no holdings in Canada

Advertisement

TGF has no holdings in Canada

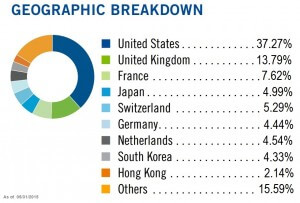

He started by saying the fund is 18% overweight in European stocks, 15% underweight in the U.S., and later in the interview revealed the fund no longer has any exposure to Canada, even though as a global equity fund, you might expect it to own perhaps a 3% index weighting.

“As of today, the fund (TGF) has no holdings in Canada, zero,” he told me, “That’s not an anti-Canada statement. It’s simply the fact this is a market that’s relatively overweight financial companies and we see more value in European financials, especially recently because they fell so much in the first quarter.”

Like the managers before him, Harper says he’s “geographically agnostic.” By that, he means that the fund does not start with a top-down geographic perspective but from a bottom-up stock-by-stock process based on valuations. The geographic mix that results is purely a byproduct of that discipline, which is why it’s always interesting to hear their views on relative valuations around the world.

So while you might expect a global index fund to be half in the U.S., TGF was only 37% in the U.S. as of May 31. “The U.S. is becoming a bit of a fully valued market. Earnings are at all time highs, which is testimony to the fact QE actually worked and companies have been very aggressive on their margins. They’re well above the 2007 peak in earnings and valuations are starting to reflect that.”

So U.S. stocks are trading at a 10% premium to their long-term values. “That’s not to say there’s not some value in the U.S. Our largest holding is Microsoft, which has done very well recently. There’s just more value in Europe.” As of April, a Templeton fact sheet shows that other top 10 U.S. holdings include Citigroup Inc., Comcast Corp., CVS Health Corp. and biotech firms Amgen Inc. and Gilead Sciences.

Europe is the opposite: trading at a 10% discount to their longer term values. In Europe, “earnings of companies are still way below their 2007 peak, partly because they were very slow on QE but now we’re seeing a bit of that. Touch wood that Greece will be resolved very soon.”

The obvious question is how the ongoing volatility over Greece affects its view on European stocks in general. The fund has no direct exposure to Greek equities and very few holdings in Portugal, Italy or Spain.

But you’d think European financial stocks with exposure to Greece would be at risk, I ask.

“Greece is very interesting,” Harper replied, “If you’d asked the same question three years ago I’d have been concerned because we have exposure to European financials. A number of those companies have exposure to the Greek financial system but over the last two or three years they rebuilt their tier-one capital ratios and companies like ING reduced their exposure to Greek lending. I cover the reinsurance industry and know that back in 2012-2013, Munich Re had $4 or $5 billion exposure to Greek bonds but that’s now in the hundreds of millions. They’re reduced their exposure so if there is to be an event, the impact would be relatively small. I don’t think it’s a big issue.”

He started by saying the fund is 18% overweight in European stocks, 15% underweight in the U.S., and later in the interview revealed the fund no longer has any exposure to Canada, even though as a global equity fund, you might expect it to own perhaps a 3% index weighting.

“As of today, the fund (TGF) has no holdings in Canada, zero,” he told me, “That’s not an anti-Canada statement. It’s simply the fact this is a market that’s relatively overweight financial companies and we see more value in European financials, especially recently because they fell so much in the first quarter.”

Like the managers before him, Harper says he’s “geographically agnostic.” By that, he means that the fund does not start with a top-down geographic perspective but from a bottom-up stock-by-stock process based on valuations. The geographic mix that results is purely a byproduct of that discipline, which is why it’s always interesting to hear their views on relative valuations around the world.

So while you might expect a global index fund to be half in the U.S., TGF was only 37% in the U.S. as of May 31. “The U.S. is becoming a bit of a fully valued market. Earnings are at all time highs, which is testimony to the fact QE actually worked and companies have been very aggressive on their margins. They’re well above the 2007 peak in earnings and valuations are starting to reflect that.”

So U.S. stocks are trading at a 10% premium to their long-term values. “That’s not to say there’s not some value in the U.S. Our largest holding is Microsoft, which has done very well recently. There’s just more value in Europe.” As of April, a Templeton fact sheet shows that other top 10 U.S. holdings include Citigroup Inc., Comcast Corp., CVS Health Corp. and biotech firms Amgen Inc. and Gilead Sciences.

Europe is the opposite: trading at a 10% discount to their longer term values. In Europe, “earnings of companies are still way below their 2007 peak, partly because they were very slow on QE but now we’re seeing a bit of that. Touch wood that Greece will be resolved very soon.”

The obvious question is how the ongoing volatility over Greece affects its view on European stocks in general. The fund has no direct exposure to Greek equities and very few holdings in Portugal, Italy or Spain.

But you’d think European financial stocks with exposure to Greece would be at risk, I ask.

“Greece is very interesting,” Harper replied, “If you’d asked the same question three years ago I’d have been concerned because we have exposure to European financials. A number of those companies have exposure to the Greek financial system but over the last two or three years they rebuilt their tier-one capital ratios and companies like ING reduced their exposure to Greek lending. I cover the reinsurance industry and know that back in 2012-2013, Munich Re had $4 or $5 billion exposure to Greek bonds but that’s now in the hundreds of millions. They’re reduced their exposure so if there is to be an event, the impact would be relatively small. I don’t think it’s a big issue.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

The first home savings account was created to help you save more money for a home purchase. Here’s how...

While ethical investors are hanging on, the number of advisors offering the methodology has pulled back, according to a...

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

Here’s why mutual funds don’t travel well across international borders—and what Canadian investors can do instead.

Should you hold equities? Fixed income? An annuity? Or all three? Financial advisors debate the options in today’s “tariffied”...