Why tax season is turning into a debt trap for Canadians (and how to avoid it)

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how to avoid a surprise bill or debt spiral.

Advertisement

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how to avoid a surprise bill or debt spiral.

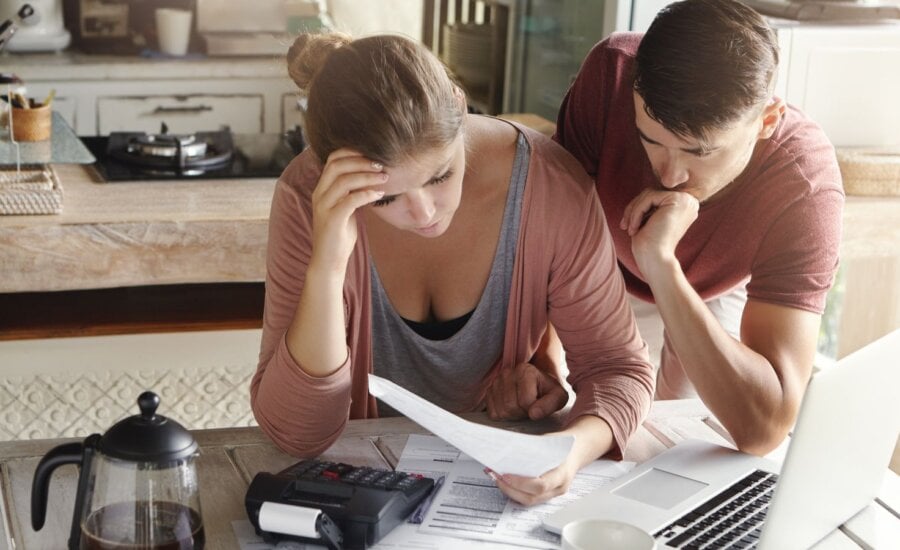

If you typically carry a credit card balance, you’re in good company. The recent Study of the Canadian Consumer (Winter 2026) by Vividata shows that more than 1 in 3 Canadians (36%) usually have a credit card balance from month to month. What’s striking, however, is the study’s finding that 49% of card holders are living paycheque to paycheque. That financial fragility is what makes tax season especially risky.

Many Canadians rely on their tax refunds to pay down debt or catch up financially, but when those refunds are smaller than expected (or, worse, turn into a bill), it can push already-stretched households further into debt, creating a cycle that’s hard to break.

We spoke with Stacy Yanchuk Oleksy, CEO of Money Mentors, about the challenges Canadians are facing, how to avoid a surprise bill at tax time, and what to do if you owe money after filing your return.

The Vividata study polled 75,000 people nationwide to get an idea of the state of Canadians’ personal finances. Here’s what the responses revealed:

These responses, plus the fact that nearly half (49%) of Canadians who are in debt are living paycheque to paycheque, suggest that Canadians are struggling to make ends meet. And more people are relying on tax refunds to stay afloat, which can be a problem if they end up owing rather than getting a refund.

“Financial strain is a function over time,” said Yanchuk Oleksy. And Canadians have had a tough few years. Post-COVID prices are still high, despite inflation cooling to pre-pandemic levels. Unfortunately, wages haven’t kept up with inflation, and many people have had to dip into savings or lean on credit to get by.

The study also showed that younger generations (between the ages of 25 and 34) are most likely to hold consumer debt. Yanchuk Oleksy says this is because younger generations have had more access to credit cards, widespread opportunities to use buy now pay later plans, and the pressure of keeping up with their peers’ purchasing habits compared to older generations.

Related reading: Credit counselling calls surge as Canadians struggle with rising costs

We mentioned that more Canadians plan on using their tax refunds to pay off credit card debt, but taxpayers aren’t guaranteed a refund. In fact, you might owe once you file. Since Yanchuk Oleksy is a debt expert, we asked her about the best ways Canadians can avoid a surprise bill from the Canada Revenue Agency (CRA). Here are the strategies she recommends:

Check your credit eligibility

Prosper Canada has an incredibly useful financial tool on its website. Enter your demographic information into its Benefits Wayfinder tool to see a list of provincial and federal credits or programs you’re likely eligible for. The tool even tells you whether or not separate applications are required or if you just need to file your personal taxes.

For Canadians already carrying balances, adding tax debt on top can quickly snowball—especially if they turn to high-interest credit to cover what they owe.

There are few things worse than going through the process of filing your taxes only to learn that you owe money, especially if you already have credit card debt that you can’t pay off. Before you panic, take a breath and consider your options.

Deadlines, tax tips and more

Yanchuk Oleksy says to pay the tax bill if you can afford it. If not, contact the CRA and explain that you’re having trouble making the payment. She notes that the CRA is always open to working with taxpayers to find a payment plan that works for everyone. “They’re there to help and make it work.”

On the other hand, if you ignore the bill or miss payments and don’t respond to the CRA’s attempts to contact you, you’re only making the situation more challenging. Maybe you’re already at that point and don’t know where to turn. Don’t hesitate to reach out to a non-profit credit counselling agency for support. They can help you create a manageable budget that includes the tax debt, and point you towards valuable community resources.

Affordability has definitely been a focus for the federal government. As a response to higher prices and economic uncertainty, Parliament introduced the Canada Groceries and Essentials Benefit Act, which replaces the GST/HST credit. With this new legislation, eligible Canadians will receive:

Times are tight for many Canadians, and carrying a credit card balance has become a reality for many households. But relying on tax refunds to stay ahead can be risky if a balance turns into a bill. Planning ahead by adjusting tax withholdings, tracking your income, and understanding available credits can help reduce the chance of being caught by surprise when you file. If you’re already facing tax debt, acting early and seeking support can help make it more manageable.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

From home office costs to travel expenses, discover the tax deductions employees may qualify for and how to claim...

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Before buying a home in Canada, U.S. citizens should understand the cross-border tax and ownership rules that can have...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...

More Canadians are exploring alternatives to the Big Six. Learn what to compare before switching banks and how to...

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.

Rising temperatures can mean higher electricity bills. Experts share simple ways Canadians can stay cool while using less energy.