How to pay off debt and save for the future

Can two young chiropractors with a big mortgage and more than $140,000 in combined student loans and line-of-credit debt still find money to start saving and investing for the future?

Advertisement

Can two young chiropractors with a big mortgage and more than $140,000 in combined student loans and line-of-credit debt still find money to start saving and investing for the future?

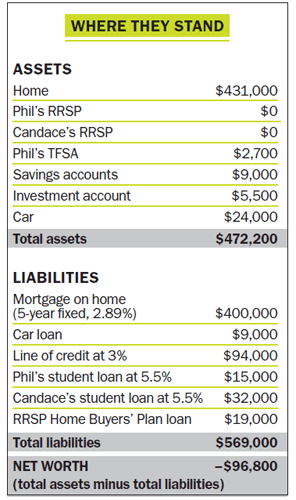

Phil and Candace Ranjan are smart people. In fact, the two chiropractors have four university degrees between them. And for a young married couple still in their 20s, they also have a healthy combined income of $110,000. But the pair, who live in London, Ont., also has three huge liabilities: $47,000 in student loans, $94,000 on a line of credit and a $400,000 mortgage on a home they purchased last year for $431,000. In total, they are starting married life deep in the red, with net liabilities of $96,800. “We have huge expenses and absolutely no spending money,” says Phil, 29. “We’re professionals but we’re not earning to our fullest potential. We know we need to pay down our debt but aren’t sure which way is best. And we’d love to start investing but we just can’t seem to save any money. It’s frustrating.”

The Ranjans (whose names we’ve changed to protect privacy) married last fall. They spent two years saving up for the cost of their wedding and $31,000 for a down payment on the 1950s-style red brick bungalow they now own. “It’s a fixer-upper, but it’s near nature trails and we really love that,” says Candace, 28. “We figure we’ll be doing small renovations for a few years. We want to spend $2,000 this spring to lay more tile.”

Another ongoing expense is the cost of setting up practice. Right now, they both work for Phil’s father—a chiropractor who plans to retire in 10 years. “You can buy a business yourself but that’s expensive,” says Phil. He explains that chiropractors starting their careers must practice with an associate, and usually give up 40% of their salary to that mentoring associate for three years. “My dad is only having me give up 20% and Candace none at all. That’s a good deal for us.”

Living in Phil’s parents’ basement for free between 2011 and 2013 was another boon for the couple—it was instrumental in helping them save money for their wedding and home down payment. And because Phil graduated from chiropractic school in 2011, a year before Candace, he was also able to whittle down his student debt from $30,000 to $15,000. “I’ve always wanted to be debt-free,” he says. “That’s important to me.”

Where the couple has really fallen short fiscally was in failing to take a harder look at their joint finances until last October, when they moved into their new home. The mortgage aside, the majority of their debt is tied up in Candace’s post-secondary education costs.

“Chiropractic college alone was $22,000 a year for each of us,” says Phil. “My parents stepped up to the plate each year with $10,000 and the remaining $12,000 a year was funded through student loans.” Candace also had help with financing from her parents but not to the same extent. “Tuition, books and residency fees were overwhelming,” she says. “My parents gave me $500 a month towards rent but nothing else.” Candace now has $94,000 outstanding on her line of credit—most of it for chiropractic college expenses—and another $32,000 in student loans.

“My biggest worry is Candace’s line-of-credit debt,” says Phil. “We feel trapped by it.” They’d like to pay off their student loans first, which carry a 5.5% interest rate. But Phil has heard rumors from friends that the interest rate on Candace’s line of credit can, at a moment’s notice, be raised to 6% from its current 3%. “The details of how her line of credit works in particular are a mystery to me, but I don’t want to appear pushy so I don’t ask any questions,” he says. “But having it makes me nervous. I’m curious to find out if we could transfer the loan to another bank and try to get a lower rate.”

Additional costs Phil and Candace never foresaw were how expensive work insurance and chiropractic association membership fees would be. Right now, they pay $3,126 annually in malpractice insurance, almost $2,000 in disability insurance, and $1,669 in critical illness insurance for two policies each worth $100,000. “I like the idea of getting $100,000 right away in case one of us gets critically ill,” says Phil. “And if by age 65 we haven’t used it, we get our premiums back. It’s like a forced savings plan for us.”

They are also paying $1,850 per year for two whole life policies, also worth $100,000 each. “It’s permanent insurance,” says Candace. “We pay the premiums for 10 years, then don’t have to pay any more. That seems like a good deal to us.”

Annual professional membership fees to the Ontario Chiropractic Association (OCA), the College of Chiropractors of Ontario (CCO) and the Acupuncture Council of Ontario (ACO) also eat up about $5,000 of their expenses. “We’re happy with our malpractice insurance but, coupled with other insurance costs, that totals more than $13,000 per year. That’s a huge expense that crept up on us,” admits Candace. “A good friend of ours sold us most of our insurance,” adds Phil.

Despite all these expenses and considerable debt, one thing working in Phil and Candace’s favour is their great work ethic. “I’ve always tried to save as much as possible and contribute to my own education bills,” says Phil, who spent his summers off from school working at a variety of part time jobs in his native London. Candace, who grew up in Ottawa, has also had part-time jobs since starting university. “I worked for a steel factory for three summers, watching the molds and making sure they didn’t overflow,” she says. “It was a safety inspector’s job and it was boring work, but it paid very well.”

It was in university while both were studying kinesiology that the couple met. “I even went to a class I wasn’t supposed to be in so I could meet her,” says Phil. “She was just such a friendly person that I was drawn to her from the start.” Then, in 2007, Phil entered Chiropractic College. Candace followed a year later.

Today, another concern the couple has is whether they’re too focused on putting every spare penny they have toward debt elimination. Should they also be building their investment portfolio using RRSPs and TFSAs? They used all the money from their RRSPs—$19,000—for the Home Buyers Plan last summer and are on track to pay it back in 12 years. They have $9,000 in a savings account earmarked for repairs to their home. They also have an emergency fund made up of $5,500 in an investment account holding guaranteed investment certificates (GICs), as well as $2,700 in Phil’s TFSA. He plans to contribute just $600 to the TFSA this year. “We really want to get started with a savings program,” says Phil. “I just don’t know if we should start now, or after the line of credit and student loans are paid off. It’s hard to say what’s best in the long run.”

The good news is that because Phil and Candace are self-employed, and because they also have tax credits remaining from their post-secondary education, their tax bill is low—just $12,000 a year between them. So this year, after all expenses are paid, they hope to have a net income of about $8,000.

They’d also love to learn more about investing and maybe even buy a rental property in a few years. “I think real estate is a great investment when we can afford it,” says Phil. “I love the idea of having someone else pay off my mortgage. But for now, I still have a huge one of my own so I probably shouldn’t get ahead of myself.”

The couple’s main focus is their goal of being debt free in 15 years. They realize that goal is a lofty one, but they’re also counting on having more future income as they continue to grow their business and get more clients. “We’re both self-employed so our income will vary, but in five to seven years I should be able to earn $200,000 and Candace about $150,000,” says Phil. “That’s heartening.”

And one day soon they’d also like to start a family. “We’re looking forward to being parents,” says Candace. “It’s the key to a happy life for us. We can’t wait.”

Phil and Candace Ranjan are smart, young professionals at a busy time in their lives. Since graduating two years ago, they’ve started jobs, gotten married, and even bought a house. “That’s amazing,” says Annie Kvick, a fee-for service planner with Money Coaches Canada in North Vancouver. “It’s difficult for young people just starting out but Phil and Candace are being smart with their money. That will pay off in the end.”

There are also savings to be had with the couple’s insurance, says Jack Bendaham, an independent insurance broker in Thornhill, Ont. “But they need to make sure they have the right policies in place—and at the right cost.”

To eliminate their debt in 15 years and start an investment plan, the Ranjans need to do the following:

Pay off student loan debt first. The interest rate on the Ranjans’ student loans is 5.5%. “Pay off Candace’s $32,000 student loan in five years,” says Kvick. “It should be a priority. Then Phil’s.” When those are paid, Kvick says the Ranjans should take the money that was going to student loans and put it towards their line-of-credit debt.

Phil shouldn’t worry about fluctuating interest rates on Candace’s line of credit. Kvick adds, “Just keep paying your bills on time and improving your credit score. If you do that, increases will be minimal.”

Another factor working in the Ranjans’ favour are the larger salaries they can anticipate as they become more established in their careers. “As their income increases over the years, 50% of any salary increase should go towards the debt,” says Kvick. “If they follow this plan, their non-mortgage debt will be paid off in 12 years.”

Look at your insurance. The Ranjans are paying more than $5,400 towards disability, critical illness and life insurance coverage. That’s a lot. If the Ranjans feel strapped for cash, insurance expert Jack Bendaham says they should consider cancelling their whole life policies and replace them with term insurance. That move alone would save them $1,850 a year.

“The couple should have enough life insurance to pay off their debt plus at least five times their annual income,” Bendaham says. “And since kids will be in the picture soon, I think they should buy a $1 million joint-to-die 20-year term life insurance policy. It will cost them only about $900 a year. The younger you are, the less expensive insurance can be.”

Regarding their critical illness insurance, Bendaham says it’s expensive but feels they need it. However, they can modify the policy to save some money. “They can save themselves about $300 annually by cancelling the ‘return of premium’ rider which adds 20% to their premium—maybe more.”

Contribute to RRSPs. Right now, the Ranjans have $8,270 available for investment every year. Kvick advises the couple to put $4,000 to Phil’s RRSP and $4,000 in a spousal RRSP for Candace each year. The money should be invested 80% in equities and 20% in fixed income because of their long time horizon before retirement.

“They can use their TFSA as an emergency fund,” says Kvick. “A portion of the tax refund from the RRSP contributions can be put towards the TFSA and the rest toward their student debt.”

Get the help of an adviser. If the Ranjans feel they need an adviser, the MoneySense Approved tool is a great place to look for a fee-for-service planner. “It’s also a good idea for them to have an annual financial check-up with an adviser to make sure they stay on plan,” says Kvick. Because if they stay the course, they should be completely debt-free in 15 years, “which is amazing.”

Only at that time should they consider investing in a rental property. “Options will open up for them,” says Kvick. “They’ll be in great financial shape, whatever they decide to do.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected] if we use your story, your name will be changed to protect your privacy.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Navigating student financial aid in Canada? Learn how loans, grants, scholarships, and private options can help pay for post-secondary...

Disabled students in Canada face higher costs for postsecondary education. Here’s a guide to grants, scholarships, and supports that...

Canada is built around borrowing, credit scores, and financing. For many newcomers, adapting to that system can feel overwhelming.

Placing a few bets during the World Cup may feel low-stakes, but experts say it’s easy to lose track...

A new study shows that 41% of Canadians believe bankruptcy is a moral failing, at a time when insolvencies...

As side hustles become more popular, Canadians are looking for bank accounts that can help them track their income,...

Bank of Canada holds its 2.25% rate for a fourth time amid inflation risks from oil prices, affecting mortgages,...

Most Canadian parents are saving for their child’s education, but few feel confident it will be enough. Here’s why...

Canadians appear to be managing economic pressures overall, but deeper data and lender results reveal growing pockets of credit...