Where to invest $10,000

As your portfolio grows, lucrative new options open up. Both low-fee mutual funds and index funds are a good bet for five-figure investors

Advertisement

As your portfolio grows, lucrative new options open up. Both low-fee mutual funds and index funds are a good bet for five-figure investors

If you start with a $10,000 portfolio that grows at 10% per year, after the first year you’ll have $11,000. But after two years you won’t just have $12,000 because the $1,000 you earned in the first year also starts to work for you. Instead, your nest egg will have grown to $12,100 (assuming the growth compounds once per year). While that extra $100 might not sound like much, that compounding effect really adds up over long periods.

In fact, if you check back in on the portfolio after 30 years, you’ll find the impact is astounding. Without compounding, the portfolio would have grown to $40,000. But with compounding it shoots up to nearly $175,000, more than four times as much.

This is where annual fees—like those levied on many funds and financial services—come in. They represent the vampires of compounding.

If you invest $10,000 in a fund that earns 10% per year before fees and it charges 2.5% annually, then after 30 years you wouldn’t wind up with almost $175,000. Instead, your nest egg would stand at just under $88,000. The seemingly small 2.5% annual fee sucked up more than half of your gains.

Unfortunately, annual fees often range between 2.0% to 2.5% in Canada and in some instances they’re even higher.

If you start with a $10,000 portfolio that grows at 10% per year, after the first year you’ll have $11,000. But after two years you won’t just have $12,000 because the $1,000 you earned in the first year also starts to work for you. Instead, your nest egg will have grown to $12,100 (assuming the growth compounds once per year). While that extra $100 might not sound like much, that compounding effect really adds up over long periods.

In fact, if you check back in on the portfolio after 30 years, you’ll find the impact is astounding. Without compounding, the portfolio would have grown to $40,000. But with compounding it shoots up to nearly $175,000, more than four times as much.

This is where annual fees—like those levied on many funds and financial services—come in. They represent the vampires of compounding.

If you invest $10,000 in a fund that earns 10% per year before fees and it charges 2.5% annually, then after 30 years you wouldn’t wind up with almost $175,000. Instead, your nest egg would stand at just under $88,000. The seemingly small 2.5% annual fee sucked up more than half of your gains.

Unfortunately, annual fees often range between 2.0% to 2.5% in Canada and in some instances they’re even higher.

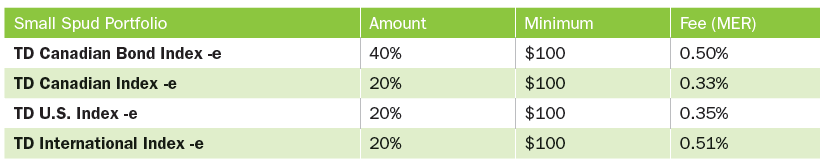

Plant your spuds

Plant your spuds

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Haven’t filed taxes in years? Learn the risks, hidden costs, and step-by-step ways Canadians can catch up and reclaim...

Switching jobs or getting laid off? Here’s how it affects your taxes, from higher brackets to severance and EI...

A recent EQ Bank survey found that more Canadians are relying on this year’s tax refunds to pay for...

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Home exchanges are changing how we travel, making it more affordable, flexible, and personal. Here’s how platforms like HomeExchange...

Filing your 2025 taxes in 2026? Here are the key changes, cancelled credits, and CRA updates Canadians need...

If it feels impossible to get ahead, you’re not imagining it. Here’s how inequality and policy choices are...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

I have $10,000 that I would like to safely invest with a good interest. I am 78 years old with no assess and living from my government pension. I have that money in a TD chequein account but I think I am wasting getting some interest. Any suggestion? Thank you.

Due to the large volume of comments we receive, we regret that we are unable to respond directly to each one. We invite you to email your question to [email protected], where it will be considered for a future response by one of our expert columnists. For personal advice, we suggest consulting with your financial institution or a qualified advisor.