A delicate juggling act: Mortgages, kids and saving

The Masons want to pay off the mortgages on two properties while saving enough to put four kids through university

Advertisement

The Masons want to pay off the mortgages on two properties while saving enough to put four kids through university

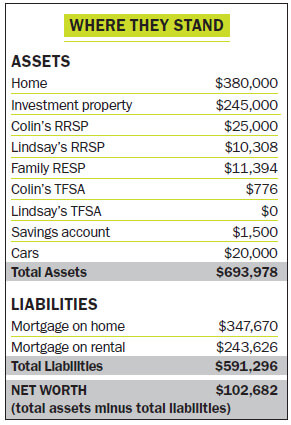

Since the Masons married in 2008, the couple (whose names we’ve changed to protect privacy) have pooled most of their assets into real estate. They held on to the first home they bought in 2007 and kept it as a rental when they bought their current home two years ago. The mortgage on their principal residence is around $348,000, with around $244,000 owing on the other house.

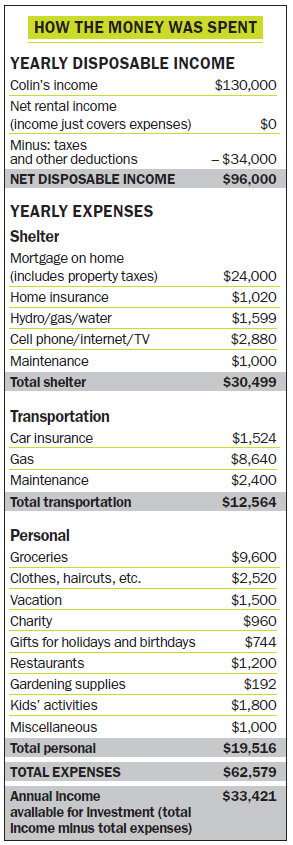

“The rental property carries itself and we basically break even on it,” says Colin, a 32-year-old welder, who earns a sizeable $130,000 paycheque annually. “We’re on track to pay the rental off in 15 years and our home in 19. We want to be completely mortgage-free by age 50. I like the idea of having a regular stream of income and since I don’t know much about stocks, this plan with the rental suits me. “But we’ve been told that it would be better to pay our own home off quicker and take more time paying off the rental for tax reasons. We’re not sure if that’s really true.”

Lindsay, on the other hand, has completely different ideas about the types of investments the couple should be making. While Colin wants to buy another rental property, Lindsay can barely tolerate owning one. “I hate dealing with tenants and late rent. I think it’s more stress than it’s worth,” she says. “I think we should take our focus away from real estate and diversify. We have to find a balance.”

One of her top goals is to pay for a big chunk of their kids’ post-secondary education and she believes the best way to do that is through the Registered Education Savings Plan (RESP), which provides lucrative government grants. Right now, the couple has around $11,000 in a family RESP and the kids’ Universal Child Care Benefit of $300 per month per child goes directly into the account. “But I worry we’re not contributing enough,” says Lindsay. “We’d like to be able to pay the majority of their post-secondary education and since we plan on having another child soon, I know that will be a huge challenge.”

Lindsay also wants to see them bulk up their own savings. They’ve largely ignored their TFSAs up until now, but she’d like to start contributing $1,500 per month, or about $18,000 per year, in order to make up for all their combined missed contribution room. “We’ll top up my TFSA first and then do his,” says Lindsay. And even though Colin has a defined benefit pension plan with his employer, the couple contributes $75 per week—or $3,900 per year—into his RRSP. Lindsay, however, hasn’t contributed anything to her RRSP since she quit working in 2012 to focus exclusively on their kids. “I’ve heard about spousal RRSPs but I’m not sure what they are exactly and if they’d be of benefit to us,” she says.

The couple’s low risk tolerance also has them feeling uneasy about how to grow the investments in the RESP, TFSAs and RRSPs they already have. “We’re both so conservative that I don’t know if it’s really possible for us to feel comfortable holding much more than a balanced mutual fund,” says Lindsay. Even Colin has contemplated selling their rental property and using the proceeds to invest in their various accounts to build their investments that much quicker.

Working in the Masons’ favour is the fact that they have more than $33,000 in net income available for investments annually and no other debt apart from their mortgages. “We recently paid off Colin’s truck and my Honda,” says Lindsay. “That leaves us with a substantial amount of money each year to invest and hopefully have a little left for some fun with the kids.”

Lindsay and Colin attribute their strong saving habits and financial ambition, in large part, to their upbringings. Lindsay’s parents were both janitors and she remembers how they used coupons for all their shopping. “My parents passed away with nothing to show for all their hard work. They certainly didn’t have anything to offer my two sisters and me. I had to work two jobs to put myself through college.”

Since the Masons married in 2008, the couple (whose names we’ve changed to protect privacy) have pooled most of their assets into real estate. They held on to the first home they bought in 2007 and kept it as a rental when they bought their current home two years ago. The mortgage on their principal residence is around $348,000, with around $244,000 owing on the other house.

“The rental property carries itself and we basically break even on it,” says Colin, a 32-year-old welder, who earns a sizeable $130,000 paycheque annually. “We’re on track to pay the rental off in 15 years and our home in 19. We want to be completely mortgage-free by age 50. I like the idea of having a regular stream of income and since I don’t know much about stocks, this plan with the rental suits me. “But we’ve been told that it would be better to pay our own home off quicker and take more time paying off the rental for tax reasons. We’re not sure if that’s really true.”

Lindsay, on the other hand, has completely different ideas about the types of investments the couple should be making. While Colin wants to buy another rental property, Lindsay can barely tolerate owning one. “I hate dealing with tenants and late rent. I think it’s more stress than it’s worth,” she says. “I think we should take our focus away from real estate and diversify. We have to find a balance.”

One of her top goals is to pay for a big chunk of their kids’ post-secondary education and she believes the best way to do that is through the Registered Education Savings Plan (RESP), which provides lucrative government grants. Right now, the couple has around $11,000 in a family RESP and the kids’ Universal Child Care Benefit of $300 per month per child goes directly into the account. “But I worry we’re not contributing enough,” says Lindsay. “We’d like to be able to pay the majority of their post-secondary education and since we plan on having another child soon, I know that will be a huge challenge.”

Lindsay also wants to see them bulk up their own savings. They’ve largely ignored their TFSAs up until now, but she’d like to start contributing $1,500 per month, or about $18,000 per year, in order to make up for all their combined missed contribution room. “We’ll top up my TFSA first and then do his,” says Lindsay. And even though Colin has a defined benefit pension plan with his employer, the couple contributes $75 per week—or $3,900 per year—into his RRSP. Lindsay, however, hasn’t contributed anything to her RRSP since she quit working in 2012 to focus exclusively on their kids. “I’ve heard about spousal RRSPs but I’m not sure what they are exactly and if they’d be of benefit to us,” she says.

The couple’s low risk tolerance also has them feeling uneasy about how to grow the investments in the RESP, TFSAs and RRSPs they already have. “We’re both so conservative that I don’t know if it’s really possible for us to feel comfortable holding much more than a balanced mutual fund,” says Lindsay. Even Colin has contemplated selling their rental property and using the proceeds to invest in their various accounts to build their investments that much quicker.

Working in the Masons’ favour is the fact that they have more than $33,000 in net income available for investments annually and no other debt apart from their mortgages. “We recently paid off Colin’s truck and my Honda,” says Lindsay. “That leaves us with a substantial amount of money each year to invest and hopefully have a little left for some fun with the kids.”

Lindsay and Colin attribute their strong saving habits and financial ambition, in large part, to their upbringings. Lindsay’s parents were both janitors and she remembers how they used coupons for all their shopping. “My parents passed away with nothing to show for all their hard work. They certainly didn’t have anything to offer my two sisters and me. I had to work two jobs to put myself through college.”

Even today, Lindsay still knows how to stretch a dollar. “I handle all the finances. Colin just makes the money,” she laughs. In particular, she excels at getting good deals on food. “I love Fridays. It’s grocery day. I go early and check out the discount rack. People always laugh at me when they hear that, but I buy milk and peppers at great prices and just freeze them.” Combined with her well-learned prowess for couponing, she’s able to get huge discounts on her grocery bill. “Last week, I saved $74 off our regular $200 bill. That’s significant.”

Colin, too, grew up in a household where money was tight. The oldest of four siblings, his parents divorced when he was only 10. “But my mom was good with money and we made it through,” says Colin. “She worked two jobs and we kids knew she was always doing the best she could for us.”

No doubt this type of shared experience attracted Colin and Lindsay to each other when they first met at a local pub in 2004. “He was very talkative and asked a lot of questions, which attracted me to him,” says Lindsay. At the time, Colin was studying welding at a local trade school while she was working on a certificate in office administration. After their courtship and marriage came daughter Maureen in 2010, son Matthew in 2012 and baby Alison in 2013.

In 10 years Lindsay plans to return to work as an office administrator, making $40,000 annually. But for now she enjoys being home with the kids. Maureen is already taking dance classes and horseback riding lessons, and the other two will start their own activities in a few years as well. Colin, meanwhile, enjoys helping out with the kids by taking them to the park a few times a week to allow Lindsay a bit of downtime. “That definitely gives me a break,” she says.

Despite their thrifty and economical ways, the couple does have some slightly more extravagant future plans. Once a year the family visits Colin’s mom in B.C. and one day they hope to own a small cabin there—maybe when both properties are paid off. “We’d love to do more road trips and rafting with the kids,” says Colin. “Our daughter Maureen has been bugging us to go to Disney World so maybe we’ll do that one day soon, too. As for me, I’d like to eventually see all the best waterfalls in the world.”

For now, they’re busy enjoying the kids, taking it one day at a time and creating a solid financial plan for the future. Once they have it in place, they can look forward to achieving their goals together.

Even today, Lindsay still knows how to stretch a dollar. “I handle all the finances. Colin just makes the money,” she laughs. In particular, she excels at getting good deals on food. “I love Fridays. It’s grocery day. I go early and check out the discount rack. People always laugh at me when they hear that, but I buy milk and peppers at great prices and just freeze them.” Combined with her well-learned prowess for couponing, she’s able to get huge discounts on her grocery bill. “Last week, I saved $74 off our regular $200 bill. That’s significant.”

Colin, too, grew up in a household where money was tight. The oldest of four siblings, his parents divorced when he was only 10. “But my mom was good with money and we made it through,” says Colin. “She worked two jobs and we kids knew she was always doing the best she could for us.”

No doubt this type of shared experience attracted Colin and Lindsay to each other when they first met at a local pub in 2004. “He was very talkative and asked a lot of questions, which attracted me to him,” says Lindsay. At the time, Colin was studying welding at a local trade school while she was working on a certificate in office administration. After their courtship and marriage came daughter Maureen in 2010, son Matthew in 2012 and baby Alison in 2013.

In 10 years Lindsay plans to return to work as an office administrator, making $40,000 annually. But for now she enjoys being home with the kids. Maureen is already taking dance classes and horseback riding lessons, and the other two will start their own activities in a few years as well. Colin, meanwhile, enjoys helping out with the kids by taking them to the park a few times a week to allow Lindsay a bit of downtime. “That definitely gives me a break,” she says.

Despite their thrifty and economical ways, the couple does have some slightly more extravagant future plans. Once a year the family visits Colin’s mom in B.C. and one day they hope to own a small cabin there—maybe when both properties are paid off. “We’d love to do more road trips and rafting with the kids,” says Colin. “Our daughter Maureen has been bugging us to go to Disney World so maybe we’ll do that one day soon, too. As for me, I’d like to eventually see all the best waterfalls in the world.”

For now, they’re busy enjoying the kids, taking it one day at a time and creating a solid financial plan for the future. Once they have it in place, they can look forward to achieving their goals together.

Start a spousal RRSP. The Masons should continue contributing $75 per month to RRSPs but it makes sense to put that contribution towards a spousal RRSP for Lindsay. “Even though we now have income splitting in retirement, Lindsay doesn’t have a pension, so it’s wise to build up some capital in her name,” says Garbens.

If they do all this, when they retire at 60, they’ll have a paid-off home, a paid-off rental property with a healthy income stream, topped-up TFSAs, substantial RRSPs, a good defined benefit pension plan for Colin, as well as other savings. “They’ll have plenty of money to travel as well as other fun extras,” says Kvick. “They’ll have no money worries at all.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.

Start a spousal RRSP. The Masons should continue contributing $75 per month to RRSPs but it makes sense to put that contribution towards a spousal RRSP for Lindsay. “Even though we now have income splitting in retirement, Lindsay doesn’t have a pension, so it’s wise to build up some capital in her name,” says Garbens.

If they do all this, when they retire at 60, they’ll have a paid-off home, a paid-off rental property with a healthy income stream, topped-up TFSAs, substantial RRSPs, a good defined benefit pension plan for Colin, as well as other savings. “They’ll have plenty of money to travel as well as other fun extras,” says Kvick. “They’ll have no money worries at all.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected] If we use your story, your name will be changed to protect your privacy.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Silent divorces can quietly drive up financial stakes. Delays, hidden assets, and lack of formal separation can turn emotional...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Learn how to protect your family from inherited debt, unexpected taxes, and estate pitfalls. Experts share tips on wills,...

Explore retirement living options—from aging in place to assisted care—and learn how to start supportive, practical conversations with aging...

Retirement planning for couples with a significant age difference calls for realistic projections but also flexibility.

Money stress is straining relationships across Canada. Here’s what a new survey reveals, and how couples can have healthier,...

Many adult children know the basics of their parents’ money, but not the details. Discover why full financial visibility...

Sponsored By

RBC

Preparing to support yourself in your elder years is a cultural norm in Canada that newcomers must adapt to....

Find the 2026 Canadian federal and provincial tax brackets for 2025 income. Learn how marginal tax rates work, estimate...