Why I’m not opening a joint bank account with my husband-to-be

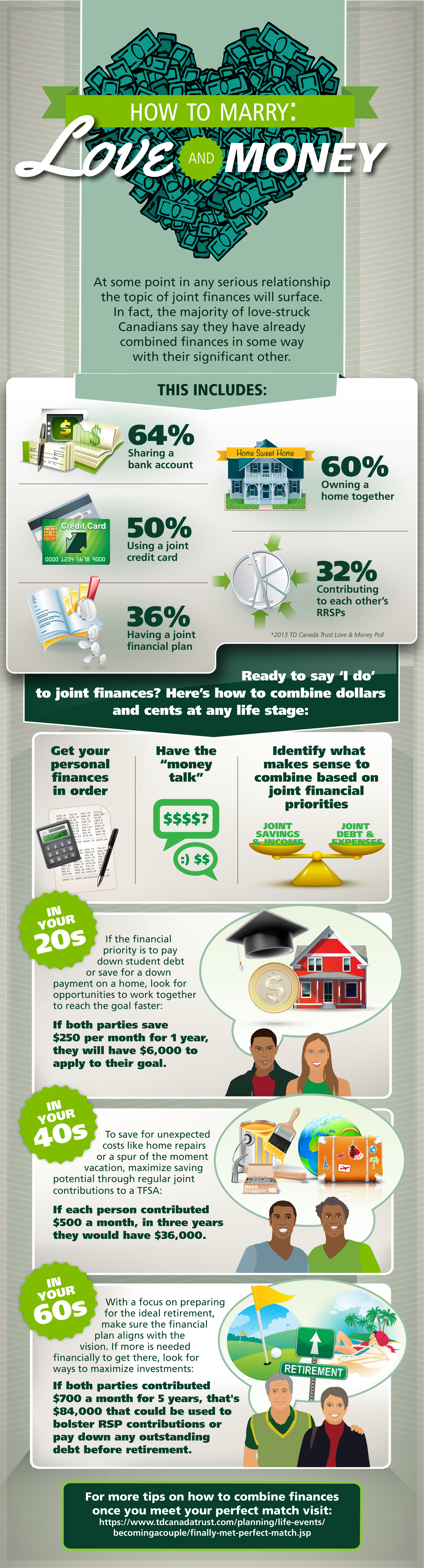

We've chosen not to go the route of 64% of couples.

Advertisement

We've chosen not to go the route of 64% of couples.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Writing a will is easier and more affordable than many people think. Here's how Canadians can protect their assets,...

More Canadians are turning to ChatGPT and other AI tools for money advice. Here's what to know about trust...

Moving to Canada often means rebuilding your credit history from scratch. One newcomer explains the hidden challenges, and the...