How not to sweat rising interest rates

Mutual fund and ETF makers have created floating-rate bond funds that aim to cut the risk of rising interest rates.

Advertisement

Mutual fund and ETF makers have created floating-rate bond funds that aim to cut the risk of rising interest rates.

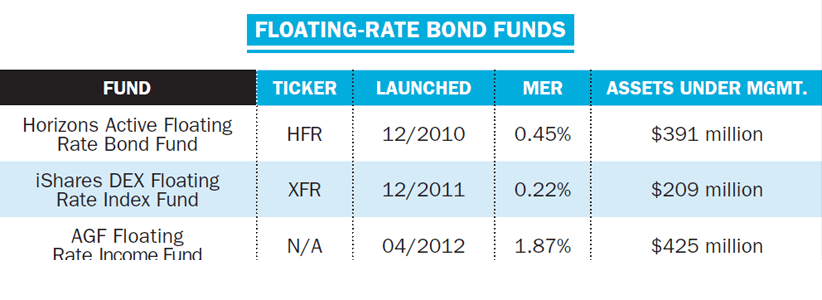

Investors can buy individual floaters through brokers but I prefer mutual funds or exchange-traded funds. Horizons won best Fixed Income ETF at the 2013 Morningstar Canadian Investment Awards. Its Active Floating Rate Bond Fund offers a portfolio of Canadian debt securities, with swap agreements to hedge rate risk. Duration is under two years. It uses active portfolio management by bond giant Fiera Capital.

iShares’ DEX Floating Rate Note Index Fund replicates an associated index three quarters in government bonds. It tracks issues as long as five years but average maturity is half that. A more passive investing style lowers costs and is best suited to investors worried about credit risk.

AGF’s Floating Rate Income Fund offers global diversification in a portfolio of U.S. senior secured bank loans. Subadvisor Eaton Vance Management, a pioneer in floaters, says floating-rate loans behave differently from, and have a low correlation to, traditional bonds. Thanks to variable coupons, yields are less volatile. Loans are reset every 30 to 90 days, so duration is near zero. Last, floating-rate loans are often most senior in corporate capital structures: important because floating-rate loans are often extended to companies with below investment-grade credit ratings. That makes these products competitive with its yields. Adding floaters to portfolios accomplishes several things. It maintains a presence for fixed income in a portfolio—a parking spot—while offering low correlation to traditional fixed-income assets. It defends against rising interest rates and their possible detrimental effect on the fixed-income component of a portfolio. And it provides a competitive income stream that can adjust to rising interest rates.

The lemmings in the crowd may be headed for an interest rate cliff. Smart investors have started beating a path to floating-rate securities. The visionary investors, those guys with their hands still up….can put them down.

Pat Bolland is a veteran financial broadcaster currently with Sun News Network. His Twitter feed is @patbolland.

Investors can buy individual floaters through brokers but I prefer mutual funds or exchange-traded funds. Horizons won best Fixed Income ETF at the 2013 Morningstar Canadian Investment Awards. Its Active Floating Rate Bond Fund offers a portfolio of Canadian debt securities, with swap agreements to hedge rate risk. Duration is under two years. It uses active portfolio management by bond giant Fiera Capital.

iShares’ DEX Floating Rate Note Index Fund replicates an associated index three quarters in government bonds. It tracks issues as long as five years but average maturity is half that. A more passive investing style lowers costs and is best suited to investors worried about credit risk.

AGF’s Floating Rate Income Fund offers global diversification in a portfolio of U.S. senior secured bank loans. Subadvisor Eaton Vance Management, a pioneer in floaters, says floating-rate loans behave differently from, and have a low correlation to, traditional bonds. Thanks to variable coupons, yields are less volatile. Loans are reset every 30 to 90 days, so duration is near zero. Last, floating-rate loans are often most senior in corporate capital structures: important because floating-rate loans are often extended to companies with below investment-grade credit ratings. That makes these products competitive with its yields. Adding floaters to portfolios accomplishes several things. It maintains a presence for fixed income in a portfolio—a parking spot—while offering low correlation to traditional fixed-income assets. It defends against rising interest rates and their possible detrimental effect on the fixed-income component of a portfolio. And it provides a competitive income stream that can adjust to rising interest rates.

The lemmings in the crowd may be headed for an interest rate cliff. Smart investors have started beating a path to floating-rate securities. The visionary investors, those guys with their hands still up….can put them down.

Pat Bolland is a veteran financial broadcaster currently with Sun News Network. His Twitter feed is @patbolland.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

Canada’s original asset-allocation ETF is still a good all-in-one investment, but it can have its flaws. Here are add-ons...

Created By

Ratehub.ca

An RESP’s investment mix should evolve over time. Here’s how to focus on growing and then preserving your savings...

Created By

Ratehub.ca

Young investors have many ways to build the fixed-income portion of their portfolios. Experts say to keep these two...

Shaken by recent stock-market losses? Investing experts weigh in on how Canadians can stick with their retirement plans when...