When interest rates and inflation rise simultaneously

It's happened before and it wasn't pretty

Advertisement

It's happened before and it wasn't pretty

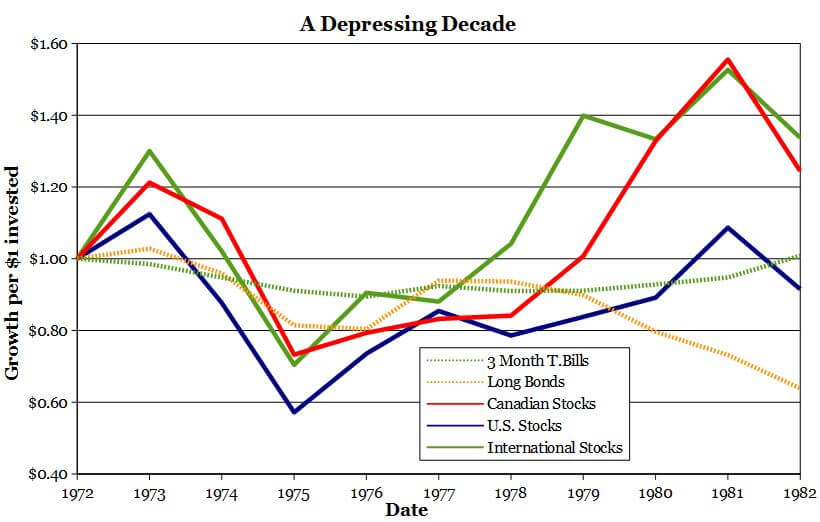

Long Canadian bonds were the hardest hit. They suffered a cumulative loss of 36% over the course of the decade. But that shouldn’t come as a big surprise because bonds with long maturities tend to be very sensitive to changes in interest rates. A small rate decline will boost their prices mightily while a tiny rate increase will causes their prices to plummet.

On a more positive note, fixed-income investors who stuck with 3-month Canadian treasury bills eked out a total gain of 1% from 1972 to 1982.

Stock investors had a particularly rough time during the market crash of 1973-1974. By the end of the 10 year span, U.S. stocks (S&P 500) lost 9% while Canadian Stocks (TSX 300) gained 24% and international stocks (EAFE) climbed 34%.

A 40% bond and 60% stock portfolio with an equal amount of money invested in each asset class—rebalanced annually—would have gained a total of 14% in inflation-adjusted terms or about 1.3% annually from 1972 to 1982, before taxes and fund fees.

It was a hard period for retirees. Given the frothy state of the markets, I fear we’re heading into a similar low-return era. You might want to prepare by saving more and spending less.

Long Canadian bonds were the hardest hit. They suffered a cumulative loss of 36% over the course of the decade. But that shouldn’t come as a big surprise because bonds with long maturities tend to be very sensitive to changes in interest rates. A small rate decline will boost their prices mightily while a tiny rate increase will causes their prices to plummet.

On a more positive note, fixed-income investors who stuck with 3-month Canadian treasury bills eked out a total gain of 1% from 1972 to 1982.

Stock investors had a particularly rough time during the market crash of 1973-1974. By the end of the 10 year span, U.S. stocks (S&P 500) lost 9% while Canadian Stocks (TSX 300) gained 24% and international stocks (EAFE) climbed 34%.

A 40% bond and 60% stock portfolio with an equal amount of money invested in each asset class—rebalanced annually—would have gained a total of 14% in inflation-adjusted terms or about 1.3% annually from 1972 to 1982, before taxes and fund fees.

It was a hard period for retirees. Given the frothy state of the markets, I fear we’re heading into a similar low-return era. You might want to prepare by saving more and spending less.

| Name | Price | P/B | P/E | Earnings Yield | Dividend Yield |

|---|---|---|---|---|---|

| CIBC (CM) | $101.35 | 1.94 | 11.09 | 9.02% | 4.78% |

| National Bank (NA) | $46.77 | 1.69 | 13.56 | 7.38% | 4.70% |

| Shaw (SJR.B) | $26.39 | 2.14 | 9.56 | 10.46% | 4.49% |

| BCE (BCE) | $61.97 | 4.33 | 19.61 | 5.10% | 4.41% |

| Emera (EMA) | $47.81 | 2.01 | 14.74 | 6.78% | 4.37% |

| Bank of Nova Scotia (BNS) | $67.35 | 1.65 | 12.03 | 8.31% | 4.28% |

| TELUS (T) | $43.28 | 3.17 | 18.11 | 5.52% | 4.25% |

| Bank of Montreal (BMO) | $86.35 | 1.49 | 12.79 | 7.82% | 3.98% |

| Royal Bank (RY) | $82.23 | 1.95 | 11.95 | 8.37% | 3.94% |

| Sun Life Financial (SLF) | $41.64 | 1.37 | 12.5 | 8.00% | 3.89% |

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Bonds are considered safer than stocks, but higher interest rates can still lead to losses. Here's what investors need...

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

Canada’s original asset-allocation ETF is still a good all-in-one investment, but it can have its flaws. Here are add-ons...

Created By

Ratehub.ca

An RESP’s investment mix should evolve over time. Here’s how to focus on growing and then preserving your savings...

Created By

Ratehub.ca

Young investors have many ways to build the fixed-income portion of their portfolios. Experts say to keep these two...