Making sense of the markets this week: January 8, 2023

As historically bad a year as it was, 2022 comes to a close, and should you wait for the market bottom? Also, Canadian stocks look solid, while Tesla does not.

Advertisement

As historically bad a year as it was, 2022 comes to a close, and should you wait for the market bottom? Also, Canadian stocks look solid, while Tesla does not.

Kyle Prevost, editor of Million Dollar Journey and founder of the Canadian Financial Summit, shares financial headlines of the week and offers context for Canadian investors.

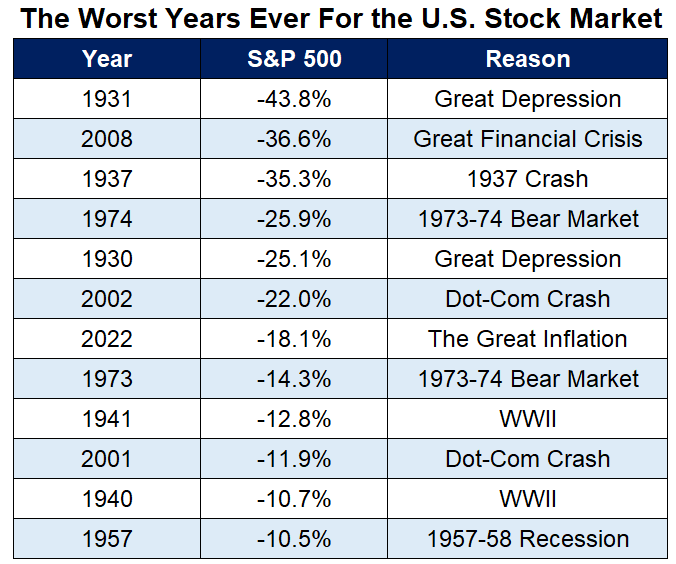

What caught my eye this week? This chart from Ben Carlson:

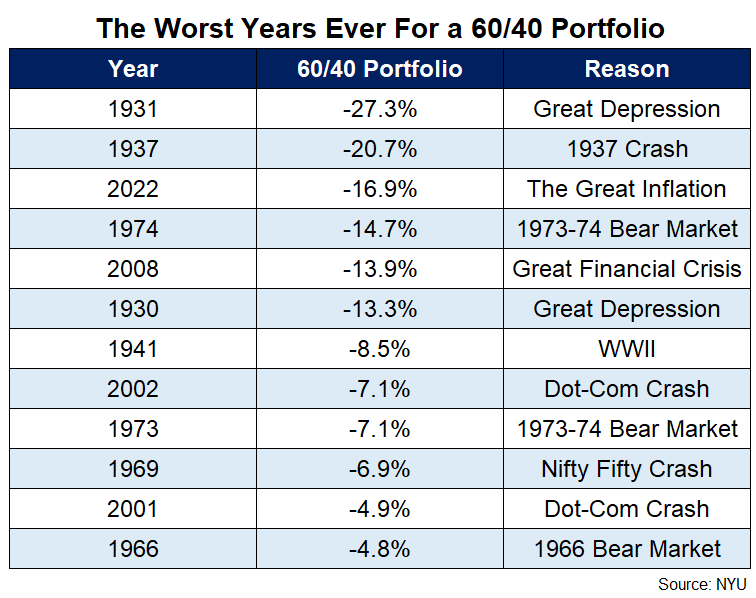

When you combine those U.S. stock market returns with the -13% return on the Bloomberg Aggregate Bond Market Index (by far the worst in 40-plus years), you’re looking at some historically awful returns for the largest capital market in the world. In fact, in the context of the traditional balanced 60/40 portfolio (60% stocks and 40% bonds), 2022 was the third worst year on record for American investors.

Take note of 2022’s line (third from the top):

Canadian investors experienced a gentler year with the S&P/TSX Composite Index posting a loss of 8.5% in 2022. And the Solactive Canadian Select Universe Bond Index shows that Canadian bonds were down about 11%. Consequently, a 60/40 portfolio would be down nearly 10% for 2022. And that’s likely closer to 12%, once fees were considered for those investors who include mutual funds.

Our four major takeaways from this information:

Four months ago, I was at a dinner party. Guests at my end of the table started talking about the recent troubles of the world’s stock markets, how difficult it was to navigate the current economic waters, and so on. I later told my wife, “I swear that I didn’t bring it up!”

I’m usually more fun at dinner parties.

However, one was an accountant, who spoke with extreme confidence about “inside information” from his son who worked in private equity in Toronto. According to him, now was the time to “go to cash and wait for the market’s collapse so that you can buy everything cheaper later.”

I’ve learned over the years that if you embarrass verbose people at dinner parties it usually doesn’t end well for anyone. So, I simply asked how he would know when the market bottoms out and what the signal would be for when to start buying again.

He looked at me quizzically and replied something like: “Oh, you know, once things start going up and the economy is doing better. That’s when it’s safe to get back in. Why would you want to buy stocks now, only for them to lose money right away as they fall?”

I respectfully nodded, which I hope gave the impression I was suitably impressed. Then, because I felt I had a fiduciary responsibility to my more impressionable friends, I waited until our “resident oracle” moved on to explain why “waiting for the bottom” in order to invest was an awful strategy.

Trying to time the market bottom is incredibly difficult. Not only do you need to get fundamental valuation analysis to be absolutely correct, but you also need to be able to gauge the “animal spirits” of market participants in the short term.

Generally speaking, by the time “things start going up,” it’s already too late to buy back in. That delay can be extremely costly.

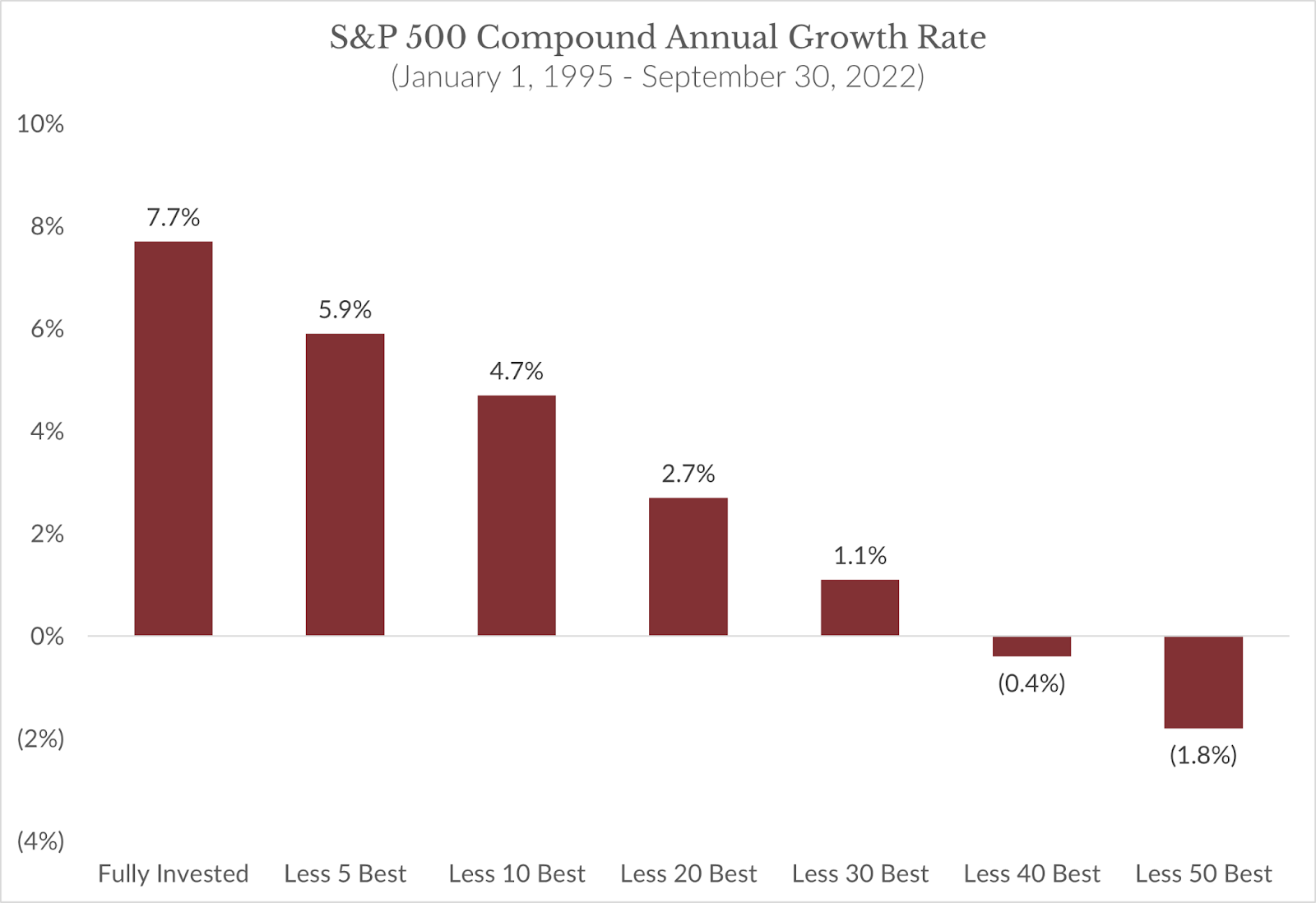

If you stay on the sidelines with a fist full of cash, “waiting for the bottom,” you’re almost assuredly going to miss out on some of the best days in the market. The vast majority of the best days in market history took place immediately following the market bottom (when people were at their most pessimistic).

The above chart shows market returns over 7,000 trading days from January 1, 1995, to September 30, 2022. If you missed the 10 best days in the market, your annual growth rate evaporated from 7.7% to 4.7%.

If you’re wondering what that sort of reduction in annual returns would have done to the raw value of your portfolio, here’s a similar look at the period of 2006 to 2021:

Coincidentally, that late-September dinner party was around the time when the markets began to turn.

Now, who knows, the markets could certainly re-test those lows. But I have wondered over the last few months whether the “start buying” Bat Signal had ever started flashing for my well-connected accounting friend. Given human beings’ behavioural biases, I would think we’re quite unlikely to ever find out.

In any case, I promised my wife that I wouldn’t ask about that at the next get-together.

The silver lining when it comes to having a really bad year in the stock markets is that (all other things being equal) the probability of higher returns going forward rises substantially. Now, if company earnings start to collapse, then all bets are off as all other things would definitely not be equal at that point.

That said, Canadian stocks look poised for very solid returns in the medium term. We can say this with a moderate degree of authority. (Remember that past events are not great indicators of future returns.)

Here are a few metrics that would lead us to a somewhat sunny medium-term prediction.

Our current P/E valuation discount relative to the U.S.’s S&P 500 shows that as a group, Canadian stocks are substantially cheaper than in the past when compared to American stocks.

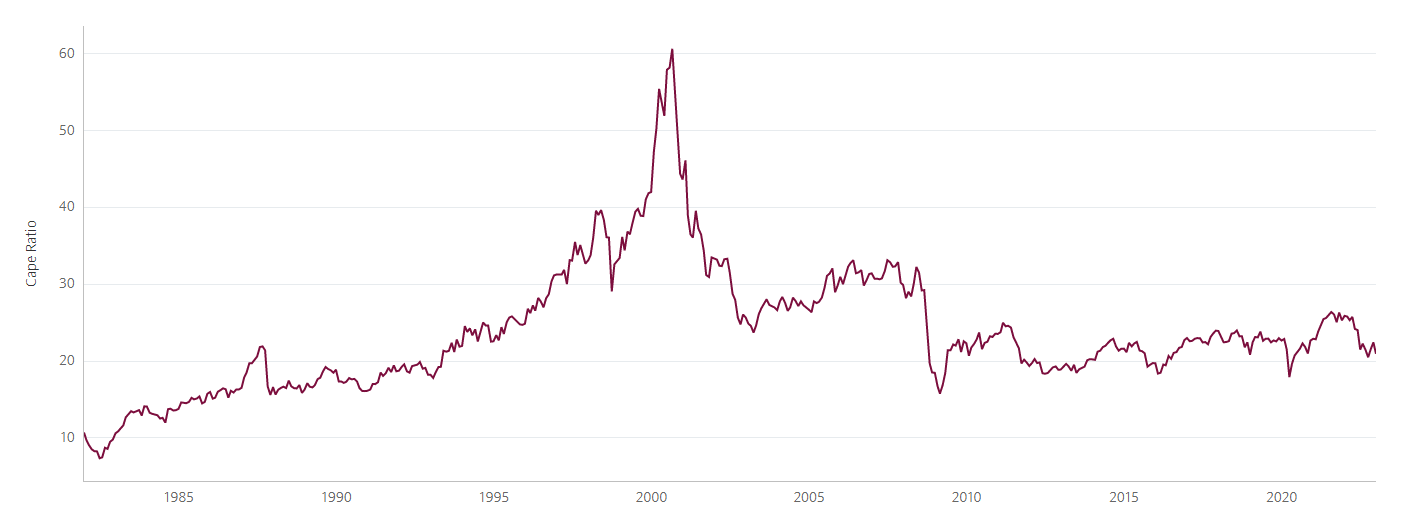

Canada’s CAPE ratio (the earnings per share over the longterm, shown below) is just under 21x, which is roughly average for us, while our forward P/E ratio is about 12.6x right now (below historical averages).

Also, the dividend yield for the S&P/TSX 60 index (shown below by the XIU ETF) is once again up around 3%, signalling that valuations are probably back to more normal levels after the exuberant highs of the past couple of years.

Of course, this isn’t a recommendation of one specific Canadian stock or exchange-traded fund (ETF). It should also be noted that while these big-picture metrics indicate “solid” or “normal” returns going forward, in the short term, there is still a wide range of possibilities to both the upside and downside.

Back in June 2022, I wrote about how shareholders of EV-maker Tesla Inc. (TSLA/Nasdaq) were in a bit of trouble. When the value of your car company equals the value of all other car companies put together, then you have set the expectation bar pretty high.

We can now safely say that perhaps those expectations were a bit too high, as the company saw its shares plunge 14% on Tuesday. Certainly, the steady stream of negative headlines generated by their CEO’s recent USD$44 billion side hustle hasn’t helped much.

Let me get this straight…

Back when Tesla didn’t make any money, it was worth more than USD$1 trillion.

Now that Tesla delivered 40% more cars in 2022 than in 2021 (up to 1.3 million vehicles) somehow it is only worth about USD$350 billion?

It just goes to show how complicated it is to try and value a company at any given time.

Also, someone forgot to tell the average investor that shine was coming off of Tesla’s balance sheet, it was still the most purchased stock by retail investors in December 2022.

That said, the craziest thing about this story is that Tesla is still worth more than most of its competitors put together!

The chart below is a bit out of date—what a difference a couple of weeks can make!—but you can still see that even at its current valuation, Tesla is nearly lapping the field.

It’s not nothing that Tesla continues to dominate electronic vehicle (EV) sales as well.

The issue, as always with investing in Tesla, is that the price of the stock continues to be dominated by retail investors who are buying shares based on brand reputation and absolutely sky-high expectations of long-term EV domination.

So, while the company’s future could be quite bright (no matter what its infamous CEO tweets), if it’s only moderately successful in the competition against every other car maker, the current valuation might still be substantially too high.

For what it’s worth, I’m keeping my eye on Ford and how successfully it is able to transition the F-150 pick-up truck to an electric platform. That vehicle is my personal measuring stick for how successful EV adoption is at any given time. If Ford can steal Tesla’s thunder, by normalizing electric vehicles to the rural world that I grew up in, the financial results will be shocking.

The Investment Industry Regulatory Organization of Canada (IIROC) and the Mutual Fund Dealers Association of Canada (MFDA) merged on January 1, 2023. The marriage is now known as the New Self-Regulatory Organization of Canada and there is a new website. The two former logos are intact (For how long? Who knows?), but you can see it at newselfregulatoryorganizationofcanada.ca.

Kyle Prevost is a financial educator, author and speaker. When he’s not on a basketball court or in a boxing ring trying to recapture his youth, you can find him helping Canadians with their finances over at MillionDollarJourney.com and the Canadian Financial Summit.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Nearly one in four Canadians say they or a family member fell victim to a scam in the past...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

From home office costs to travel expenses, discover the tax deductions employees may qualify for and how to claim...

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Before buying a home in Canada, U.S. citizens should understand the cross-border tax and ownership rules that can have...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...

More Canadians are exploring alternatives to the Big Six. Learn what to compare before switching banks and how to...

Sadly, your comments on the current market has added little as to , invest,or not invest. Gone are the days when a couch potatoe could read a financial column, or the Money Sense top 100 stock list and feel some confidence in its authors.