78 and deep in debt

Retired businessman Louis Zanini knows it's time to sell his home and pay off his $113,000 debt. But as he approaches his 80s, will he be better off financially if he buys a condo, or moves into a rental apartment?

Advertisement

Retired businessman Louis Zanini knows it's time to sell his home and pay off his $113,000 debt. But as he approaches his 80s, will he be better off financially if he buys a condo, or moves into a rental apartment?

Louis Zanini, a 78-year-old retiree from Ridgetown, Ont., loves to talk about the good old days when he was busy raising his four kids and working as a printer across the border in the United States. Louis and his wife, Rina, who passed away from cancer four years ago, also ran their own marketing and promotions business for several years from the basement of their family home. “I’ve always loved hard work and don’t like to be idle,” says Louis, who sold the business in 2008. “I wish I had kept my business because it kept me busy. I was always researching new ideas and going out to meet new customers. Things are different now without Rina or the business in the picture.”

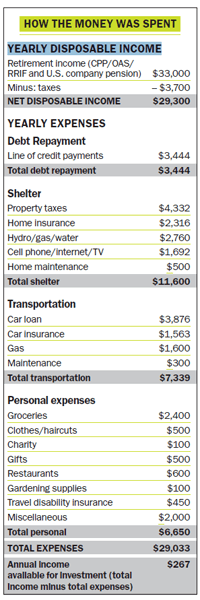

These days Louis, whose name we’ve changed to protect his privacy, is living on a fixed income of $29,000 a year but he’s worried. That’s because he still has debt on his balance sheet—$113,000 to be exact, made up of a $13,000 car loan and $100,000 on his line of credit. He expects his car loan to be paid off in three years but the $100,000 line of credit is a trickier matter. He took on the debt when he sold his business—unfortunately the amount he netted wasn’t enough to clear the company’s debts. “I’m only paying the interest on it—$3,444 a year,” says Louis. “In the past I’ve never been in debt, except for the mortgage on my home, which is paid off now. My concern is that if interest rates go up, I’ll be squeezed for money. I’m not getting any younger and I’ve been diagnosed with diabetes and prostate cancer. I think it may be the right time for me to sell the house and use any extra income to make my 80s comfortable.”

Louis Zanini, a 78-year-old retiree from Ridgetown, Ont., loves to talk about the good old days when he was busy raising his four kids and working as a printer across the border in the United States. Louis and his wife, Rina, who passed away from cancer four years ago, also ran their own marketing and promotions business for several years from the basement of their family home. “I’ve always loved hard work and don’t like to be idle,” says Louis, who sold the business in 2008. “I wish I had kept my business because it kept me busy. I was always researching new ideas and going out to meet new customers. Things are different now without Rina or the business in the picture.”

These days Louis, whose name we’ve changed to protect his privacy, is living on a fixed income of $29,000 a year but he’s worried. That’s because he still has debt on his balance sheet—$113,000 to be exact, made up of a $13,000 car loan and $100,000 on his line of credit. He expects his car loan to be paid off in three years but the $100,000 line of credit is a trickier matter. He took on the debt when he sold his business—unfortunately the amount he netted wasn’t enough to clear the company’s debts. “I’m only paying the interest on it—$3,444 a year,” says Louis. “In the past I’ve never been in debt, except for the mortgage on my home, which is paid off now. My concern is that if interest rates go up, I’ll be squeezed for money. I’m not getting any younger and I’ve been diagnosed with diabetes and prostate cancer. I think it may be the right time for me to sell the house and use any extra income to make my 80s comfortable.” Right now, Louis’s income just meets his expenses. But going forward, he’d like to do two things to get his financial house in order. First, he’d love to boost his income by about $5,000 to $10,000 a year. He feels that will be what’s needed to make his life more comfortable and worry-free as he ages. His second goal is to pay off his debt. “As I get older, there may be a time when I have to move into a retirement home, or have some form of paid home care,” he says. “I want to be ready for that financially.”

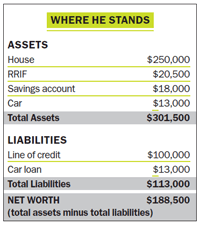

And while Louis has some savings—$20,500 sitting in a RRIF and $18,000 in a savings account—his only other significant asset is his house, which is worth about $250,000. “Selling my house and paying off all my debt and associated home-selling fees would leave me with about $120,000 in the bank,” says Louis. “That would give me some investment options.”

In fact, selling his house would leave Louis with two choices. In the first scenario, Louis could rent a nice two-bedroom apartment for $1,100 a month and put the entire $120,000 remaining from the sale of his home in his investment account. Then he would invest the money so it produced an annual income of about $5,000 to $10,000 a year, something Louis says he could probably do by investing in good dividend-paying stocks or a well-balanced portfolio of index mutual funds.

His second option is to use the $120,000 net from the sale of the house (after debt repayment) to buy a small condo for $100,000 or so. He could pay for it in cash. That would leave him about $20,000 in his investment account to buy dividend-paying stocks but he figures the savings from eliminating debt payments could go instead towards beefing up his annual income. “It’s hard to know the right choice,” says Louis. “The truth is that nice apartments are hard to find but at the same time, downsizing to a condo may have fees that I’m underestimating. It’s difficult to know what to do.”

Another fear Louis has is that there will be another drop in the stock market. “In 2008 I got caught in the stock market crash and lost $60,000 of my savings. I don’t mind some risk—I was self-employed for a while after all—but I know that going forward my options for generating more income will be limited. The years creep up on you and I’m well aware that the financial decisions I make now will have huge repercussions for my future.”

Right now, Louis’s income just meets his expenses. But going forward, he’d like to do two things to get his financial house in order. First, he’d love to boost his income by about $5,000 to $10,000 a year. He feels that will be what’s needed to make his life more comfortable and worry-free as he ages. His second goal is to pay off his debt. “As I get older, there may be a time when I have to move into a retirement home, or have some form of paid home care,” he says. “I want to be ready for that financially.”

And while Louis has some savings—$20,500 sitting in a RRIF and $18,000 in a savings account—his only other significant asset is his house, which is worth about $250,000. “Selling my house and paying off all my debt and associated home-selling fees would leave me with about $120,000 in the bank,” says Louis. “That would give me some investment options.”

In fact, selling his house would leave Louis with two choices. In the first scenario, Louis could rent a nice two-bedroom apartment for $1,100 a month and put the entire $120,000 remaining from the sale of his home in his investment account. Then he would invest the money so it produced an annual income of about $5,000 to $10,000 a year, something Louis says he could probably do by investing in good dividend-paying stocks or a well-balanced portfolio of index mutual funds.

His second option is to use the $120,000 net from the sale of the house (after debt repayment) to buy a small condo for $100,000 or so. He could pay for it in cash. That would leave him about $20,000 in his investment account to buy dividend-paying stocks but he figures the savings from eliminating debt payments could go instead towards beefing up his annual income. “It’s hard to know the right choice,” says Louis. “The truth is that nice apartments are hard to find but at the same time, downsizing to a condo may have fees that I’m underestimating. It’s difficult to know what to do.”

Another fear Louis has is that there will be another drop in the stock market. “In 2008 I got caught in the stock market crash and lost $60,000 of my savings. I don’t mind some risk—I was self-employed for a while after all—but I know that going forward my options for generating more income will be limited. The years creep up on you and I’m well aware that the financial decisions I make now will have huge repercussions for my future.” Louis comes from a large family that never had a ton of money. He was the youngest of six children and his dad was a janitor while mom stayed home to raise the kids. “My dad never owned a home,” remembers Louis. “We never had much money but we were all hugely industrious. And it helped a lot that my mom was a fabulous cook and had lots of friends in the neighbourhood. There was no fast food when I was a kid. All the food was slow.”

As a child, Louis had a job as a delivery boy for the local grocery store and drug store. He graduated from high school in 1952 and three years later landed a salaried job as a printer across the border in the United States. That’s when he met his wife Rina. “It took me three years but I finally got her to accept my marriage proposal,” he laughs.

In the late 1950s and early ’60s, the couple had four children in quick succession and Louis found himself working two jobs just to make ends meet. “Rina managed all the money,” says Louis. “She deposited my weekly cheque and paid all the bills. Those early years were tight but we slowly prospered.”

In 1965, the couple bought their first home and over the years, bought and sold three more houses, always buying a slightly bigger house to accommodate a growing family and their promotional products business. “Our plan was to always pay down the mortgage, which we did,” says Louis. “If there was any money left over, we used it for the kids’ educations, invested it back into our business or added a bit to our savings. My wife did the books for our little home marketing business and I worked on sales evenings and weekends when I got off from my printer job. It was busy.”

By 1995, the kids had moved away and started raising families of their own. That’s when the Zaninis downsized to the 1,300-sq-ft townhouse Louis lives in today. Even though he and Rina both worked part time at their promotional business well into retirement, the couple still found time to drive down to Florida two or three times a year to visit friends. “We both loved road trips and that was a joyous time,” says Louis.

Then, in 2007, Rina got breast cancer. She died the following year. Louis sold what remained of the business in late 2008, paying off the small business loans with his line of credit.

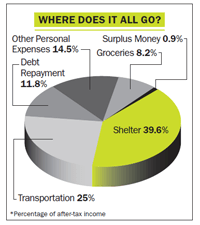

These days, Louis feels constrained by his income of about $29,000 after taxes. That would normally be plenty for him to live on comfortably but with debt payments of $3,444 annually on his $100,000 line of credit (just the interest portion) coupled with an annual payment of $3,876 on his car loan until 2015, he doesn’t see much wiggle room in his budget. With his recent diagnosis of diabetes, Louis is starting to get nervous. “Managing diabetes is a real challenge for me,” he says. “The doctors tell me I’ll need a knee replacement in a couple of years. I live alone and all four of my kids have families and jobs in other provinces. I don’t want to bother them with this. But what that tells me is my expenses could easily go way up and I have to be financially ready for that.”

As he approaches his 80s, Louis would love to be debt-free. He’d like to build a conservative investment portfolio and lately finds himself spending much of his spare time reading investment newsletters and the business section of the newspapers. Most of his money is in high-fee mutual funds but he wants to change that.

Louis also wants to focus on his health and learn to eat right. “I have to work on putting together a daily exercise routine,” he says. “I have bad knees so maybe I’ll buy a stationary bike and get going on that. The doctor ordered 30 minutes of light exercise at least five times a week. As you age, maintaining good health gets incredibly challenging.” Louis knows he’ll need both good physical health and good financial health to have a comfortable life in his 80s and he’s determined to make it all work.

Louis comes from a large family that never had a ton of money. He was the youngest of six children and his dad was a janitor while mom stayed home to raise the kids. “My dad never owned a home,” remembers Louis. “We never had much money but we were all hugely industrious. And it helped a lot that my mom was a fabulous cook and had lots of friends in the neighbourhood. There was no fast food when I was a kid. All the food was slow.”

As a child, Louis had a job as a delivery boy for the local grocery store and drug store. He graduated from high school in 1952 and three years later landed a salaried job as a printer across the border in the United States. That’s when he met his wife Rina. “It took me three years but I finally got her to accept my marriage proposal,” he laughs.

In the late 1950s and early ’60s, the couple had four children in quick succession and Louis found himself working two jobs just to make ends meet. “Rina managed all the money,” says Louis. “She deposited my weekly cheque and paid all the bills. Those early years were tight but we slowly prospered.”

In 1965, the couple bought their first home and over the years, bought and sold three more houses, always buying a slightly bigger house to accommodate a growing family and their promotional products business. “Our plan was to always pay down the mortgage, which we did,” says Louis. “If there was any money left over, we used it for the kids’ educations, invested it back into our business or added a bit to our savings. My wife did the books for our little home marketing business and I worked on sales evenings and weekends when I got off from my printer job. It was busy.”

By 1995, the kids had moved away and started raising families of their own. That’s when the Zaninis downsized to the 1,300-sq-ft townhouse Louis lives in today. Even though he and Rina both worked part time at their promotional business well into retirement, the couple still found time to drive down to Florida two or three times a year to visit friends. “We both loved road trips and that was a joyous time,” says Louis.

Then, in 2007, Rina got breast cancer. She died the following year. Louis sold what remained of the business in late 2008, paying off the small business loans with his line of credit.

These days, Louis feels constrained by his income of about $29,000 after taxes. That would normally be plenty for him to live on comfortably but with debt payments of $3,444 annually on his $100,000 line of credit (just the interest portion) coupled with an annual payment of $3,876 on his car loan until 2015, he doesn’t see much wiggle room in his budget. With his recent diagnosis of diabetes, Louis is starting to get nervous. “Managing diabetes is a real challenge for me,” he says. “The doctors tell me I’ll need a knee replacement in a couple of years. I live alone and all four of my kids have families and jobs in other provinces. I don’t want to bother them with this. But what that tells me is my expenses could easily go way up and I have to be financially ready for that.”

As he approaches his 80s, Louis would love to be debt-free. He’d like to build a conservative investment portfolio and lately finds himself spending much of his spare time reading investment newsletters and the business section of the newspapers. Most of his money is in high-fee mutual funds but he wants to change that.

Louis also wants to focus on his health and learn to eat right. “I have to work on putting together a daily exercise routine,” he says. “I have bad knees so maybe I’ll buy a stationary bike and get going on that. The doctor ordered 30 minutes of light exercise at least five times a week. As you age, maintaining good health gets incredibly challenging.” Louis knows he’ll need both good physical health and good financial health to have a comfortable life in his 80s and he’s determined to make it all work.

Heather Franklin, a fee-only adviser in Toronto, agrees. “Anyone over 60 should not have debt,” she says. “In the near future he’ll have to look at downsizing anyway so why not do it now?” Here’s what Louis should do.

Sell the house. Debt payments and house expenses are a real drag on Louis’s lifestyle. His best option is to sell the house. “I know it’s very hard for some people to sell their home because they have been a homeowner all their lives, but in Louis’s case it makes all the sense in the world,” says Lamontagne. Selling the home and paying off all the debts (including the car loan) will save him just over $7,000 a year in debt payments.

Opt for renting. Neither Franklin nor Lamontagne like the idea of Louis buying a condo. “For starters, every time you buy and sell property there are transaction costs such as realtor commissions, land transfer taxes, lawyers’ fees, and maintenance costs associated with getting a house ready for sale,” says Lamontagne. Both experts feel renting is the better option. “He should rent in a community he likes,” says Franklin, adding that Louis may need the flexibility as he ages, especially if he has to give up his car. “He should look for a nice two-bedroom apartment close to shopping, banking and activities he enjoys. Renting will allow him the flexibility he needs in case his health deteriorates and he has to go into a nursing home or retirement home.” If he sells the house, pays off his debt and rents, he’ll have an extra $20,000 a year to pay for rent and supplement his income in case he needs home care and other personal help in the future.

Invest the money wisely. When Louis sells his home, pays his realtor fees and clears off all his debt, he should have $120,000 left. Franklin would like to see Louis invest this money in dividend-paying stocks in a non-registered investment account. She suggests he steer clear of mutual funds and instead use $100,000 to buy blue-chip, dividend-paying stocks such as BCE, the five big banks, Enbridge and TransCanada Pipelines, while the remaining $20,000 is put into a bond exchange-traded fund like the iShares 1-5 Year Government Bond Index Fund (CLF). “He can have his dividends paid right into his savings account so that will help with his cash flow,” says Franklin. “Dividends are given preferential tax treatment so that will help his bottom line as well. Once the stocks are bought, he can leave them alone for years and the dividends will keep on coming. It’s a very cost-effective, hands-off approach to investing at his age.”

Lamontagne has another option. Seeing that Louis wants predictable income, he’d like him to take $100,000 from the sale of the home and buy an annuity. He can use the remaining $20,000 to buy blue-chip, dividend-paying stocks. That’s because Lamontagne believes an annuity will give Louis true peace of mind. He should see an insurance broker who can shop the market for him. “A life annuity will pay him an income for the rest of his life, no matter how long he lives,” says Lamontagne. “Best of all, most of the monthly payment will be tax-free.” For instance, if Louis bought a $100,000 non-registered prescribed annuity today, it would pay about $9,000 a year for the rest of his life. “That is the equivalent of earning a guaranteed 9% annual return tax-free,” says Lamontagne. “That’s pretty compelling, even when comparing it to dividend-paying stocks.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected]. If we use your story, your name will be changed to protect your privacy.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Heather Franklin, a fee-only adviser in Toronto, agrees. “Anyone over 60 should not have debt,” she says. “In the near future he’ll have to look at downsizing anyway so why not do it now?” Here’s what Louis should do.

Sell the house. Debt payments and house expenses are a real drag on Louis’s lifestyle. His best option is to sell the house. “I know it’s very hard for some people to sell their home because they have been a homeowner all their lives, but in Louis’s case it makes all the sense in the world,” says Lamontagne. Selling the home and paying off all the debts (including the car loan) will save him just over $7,000 a year in debt payments.

Opt for renting. Neither Franklin nor Lamontagne like the idea of Louis buying a condo. “For starters, every time you buy and sell property there are transaction costs such as realtor commissions, land transfer taxes, lawyers’ fees, and maintenance costs associated with getting a house ready for sale,” says Lamontagne. Both experts feel renting is the better option. “He should rent in a community he likes,” says Franklin, adding that Louis may need the flexibility as he ages, especially if he has to give up his car. “He should look for a nice two-bedroom apartment close to shopping, banking and activities he enjoys. Renting will allow him the flexibility he needs in case his health deteriorates and he has to go into a nursing home or retirement home.” If he sells the house, pays off his debt and rents, he’ll have an extra $20,000 a year to pay for rent and supplement his income in case he needs home care and other personal help in the future.

Invest the money wisely. When Louis sells his home, pays his realtor fees and clears off all his debt, he should have $120,000 left. Franklin would like to see Louis invest this money in dividend-paying stocks in a non-registered investment account. She suggests he steer clear of mutual funds and instead use $100,000 to buy blue-chip, dividend-paying stocks such as BCE, the five big banks, Enbridge and TransCanada Pipelines, while the remaining $20,000 is put into a bond exchange-traded fund like the iShares 1-5 Year Government Bond Index Fund (CLF). “He can have his dividends paid right into his savings account so that will help with his cash flow,” says Franklin. “Dividends are given preferential tax treatment so that will help his bottom line as well. Once the stocks are bought, he can leave them alone for years and the dividends will keep on coming. It’s a very cost-effective, hands-off approach to investing at his age.”

Lamontagne has another option. Seeing that Louis wants predictable income, he’d like him to take $100,000 from the sale of the home and buy an annuity. He can use the remaining $20,000 to buy blue-chip, dividend-paying stocks. That’s because Lamontagne believes an annuity will give Louis true peace of mind. He should see an insurance broker who can shop the market for him. “A life annuity will pay him an income for the rest of his life, no matter how long he lives,” says Lamontagne. “Best of all, most of the monthly payment will be tax-free.” For instance, if Louis bought a $100,000 non-registered prescribed annuity today, it would pay about $9,000 a year for the rest of his life. “That is the equivalent of earning a guaranteed 9% annual return tax-free,” says Lamontagne. “That’s pretty compelling, even when comparing it to dividend-paying stocks.”

Would you like MoneySense to consider your financial situation in a future Family Profile? Drop us a line at [email protected]. If we use your story, your name will be changed to protect your privacy.

Julie Cazzin is an award-winning business journalist and personal finance writer based in Toronto.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Experts say the best way to prepare for a single-income household is to test your budget first. Here's how...

Moving to the U.S. doesn’t automatically mean you should convert your Canadian investments. Here’s why tax rules, currency risk...

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Couche-Tard reports higher Q4 profit and revenue, BlackBerry raises full-year outlook after a stronger quarter, and Metro sees earnings...

Navigating student financial aid in Canada? Learn how loans, grants, scholarships, and private options can help pay for post-secondary...

Columnist Vickram Agarwal spent more money than he ever thought he would on two Oasis concerts. The spreadsheet hated...

A U.S.-Iran ceasefire has eased oil prices and inflation fears. Here's what that could mean for bitcoin prices and...