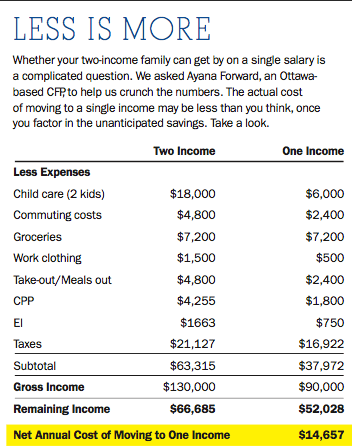

A guide to thriving as a single-income family

It takes two incomes to raise a family these days. Or does it?

Advertisement

It takes two incomes to raise a family these days. Or does it?

Talking about finances can be challenging for couples. “Often, we only deal with money when it’s a problem, but money itself is neutral.” Explains Collacutt. “We layer on all the junk—the blame, shame, anger and frustration. When we approach money from this place that’s when problems arise.” Ongoing dialogue is integral to making a single-income household work, says Trevor Van Nest, a Niagara, Ont.-based CFP and money coach.“Two brains are always better than one when it comes to personal finances.” Even when only one person earns the money, both people need to be responsible about how that money is spent.

Talking about finances can be challenging for couples. “Often, we only deal with money when it’s a problem, but money itself is neutral.” Explains Collacutt. “We layer on all the junk—the blame, shame, anger and frustration. When we approach money from this place that’s when problems arise.” Ongoing dialogue is integral to making a single-income household work, says Trevor Van Nest, a Niagara, Ont.-based CFP and money coach.“Two brains are always better than one when it comes to personal finances.” Even when only one person earns the money, both people need to be responsible about how that money is spent.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Why two people at the same life stage can be years apart financially, and how timing, housing, immigration and...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...

The biggest financial barrier for newcomers isn't always knowledge, but understanding how familiar words take on new meanings...

Financial principles can be timeless, but the tactics behind them often aren't. Here's why some money advice deserves a...

Building wealth as a couple takes more than smart investing. Here's why open communication about money is essential...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...

Putting an inheritance into a joint account may seem simple, but tax and attribution rules can affect who reports...

Financial milestones are changing for young Canadians. Here’s why experts say budgeting, saving, and consistency matter more than following...

Found this really interesting, my girlfriend who I will be moving in with next year will be studying for her masters and not working or atleast a year. This means I will be the only income provider for atleast a year and hence managing expenses and our finances will be crucial. But even more, on how we communicate our expectations and setup guidelines to keep us accountable.

This is very helpful.

As a single mom of 3 with no child support. It’s been a long struggle to finally feel just financially comfortable enough.

Unlike others who received supports and payouts after their divorce and separation.

I wasn’t the lucky one. I walked out of a domestic marriage, started a new life with 3 kids and little in my bank to survive….

Every now and then I am in searched for other supports out there.

Although there are helps but I always know there’s more, if I can just find it. I worried what if my I don’t have enough? what if my health goes down? what if there’s emergency? There’s always what if…

Hoping one day government can do more for us especially the ones with low income and no child support. FRO isn’t do enough to help us get the support we need so I think our government should do more to enforce.