Plan for the unexpected

Stress-test your financial plan for any major curve-balls life may throw your way.

Advertisement

Stress-test your financial plan for any major curve-balls life may throw your way.

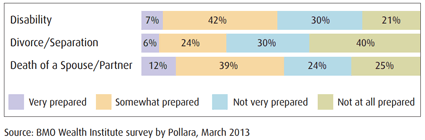

On both sides of the border today are items on the perils of unexpected events setting back long-term financial plans. CNN Money is reporting here that retirement savers are losing US$117,000 to unexpected events. Meanwhile, the BMO Wealth Institute has released a 10-page report entitled The biggest life events that can derail your financial plan.

None of this should come as a surprise to investors or anyone making long-term financial plans. As the late John Lennon sang on his final album, Double Fantasy, “Life is what happens to you while you’re busy making other plans.” (By the way, he may not have been the first to say this. See here for details.)

CNN reported on an Ameriprise Financial survey of Americans aged 50 to 70 with at least US$100,000. Nine in 10 of them had already experienced at least one economic or life event that hurt their retirement savings, while almost 40% had been hit by at least five unanticipated events that caused their average loss to hit US$144,000. The takeway, Ameriprise said, was to “expect the unexpected.”

Despite all the fancy retirement calculators available to modern investors, these tools provide at best rough guesses of what may or may not happen in the future. Who 20 years ago could have anticipated the minuscule interest rates that now afflict fixed-income investors? Stock market declines come around with unwelcome frequency and as we saw in the 2008 financial crisis, home prices are equally subject to price volatility. Putting aside money for children’s education or taking care of ailing elderly parents can also take a toll on savings.

On both sides of the border today are items on the perils of unexpected events setting back long-term financial plans. CNN Money is reporting here that retirement savers are losing US$117,000 to unexpected events. Meanwhile, the BMO Wealth Institute has released a 10-page report entitled The biggest life events that can derail your financial plan.

None of this should come as a surprise to investors or anyone making long-term financial plans. As the late John Lennon sang on his final album, Double Fantasy, “Life is what happens to you while you’re busy making other plans.” (By the way, he may not have been the first to say this. See here for details.)

CNN reported on an Ameriprise Financial survey of Americans aged 50 to 70 with at least US$100,000. Nine in 10 of them had already experienced at least one economic or life event that hurt their retirement savings, while almost 40% had been hit by at least five unanticipated events that caused their average loss to hit US$144,000. The takeway, Ameriprise said, was to “expect the unexpected.”

Despite all the fancy retirement calculators available to modern investors, these tools provide at best rough guesses of what may or may not happen in the future. Who 20 years ago could have anticipated the minuscule interest rates that now afflict fixed-income investors? Stock market declines come around with unwelcome frequency and as we saw in the 2008 financial crisis, home prices are equally subject to price volatility. Putting aside money for children’s education or taking care of ailing elderly parents can also take a toll on savings.

Far from Lennon’s double fantasy, such disruptions can inflict what BMO terms a “double shock” of both loss of income as well as unplanned extra demands on spending. Little wonder BMO finds Canadians’ biggest fear is the stress of not having enough money to retire.

If you’ve read this blog before, you’ll know what’s coming next. By all means, save and invest wisely, live below your means and do all you can to establish financial independence. This is not the same as retirement. If you can establish a modicum of findependence by your 30s or 40s (paying off all debts plus building a nest egg), you should do so: the sooner employment income is an income supplement rather than the sole means of financial support, the better.

Far from Lennon’s double fantasy, such disruptions can inflict what BMO terms a “double shock” of both loss of income as well as unplanned extra demands on spending. Little wonder BMO finds Canadians’ biggest fear is the stress of not having enough money to retire.

If you’ve read this blog before, you’ll know what’s coming next. By all means, save and invest wisely, live below your means and do all you can to establish financial independence. This is not the same as retirement. If you can establish a modicum of findependence by your 30s or 40s (paying off all debts plus building a nest egg), you should do so: the sooner employment income is an income supplement rather than the sole means of financial support, the better.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

It’s almost impossible to do, but the mindset around spending all your savings can help you make the best of the...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Filing your 2025 taxes in 2026? Here are the key changes, cancelled credits, and CRA updates Canadians need...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Global conflicts affect Canadians’ finances in real time. Learn how rising costs, volatility, and uncertainty can impact your budget...

If you leave Canada and own a rental property, or you are a non-resident and you buy a rental...

Gen Z faces an “experience gap” as AI and employer expectations rise. Co-ops, apprenticeships, and hands-on learning are now...

Rental property investors need to report their annual income and expenses on their tax return. You must also track...

The Canada Caregiver Amount can help families supporting loved ones with infirmities. Learn who qualifies and how much you...

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...