Unwrap portfolio with index mutual funds

The McEvers want to reduce their portfolio fees in order to save more for retirement.

Advertisement

The McEvers want to reduce their portfolio fees in order to save more for retirement.

Financial planner Tony de Thomasis, of De Thomas Financial Corp., says the couple are moderate-risk investors and should be comfortable with an asset allocation of 75% equities to 25% bonds and cash. As retirement approaches and if markets cooperate, portfolios would be gradually rebalanced to raise the fixed-income weight by 8% every five years or so.

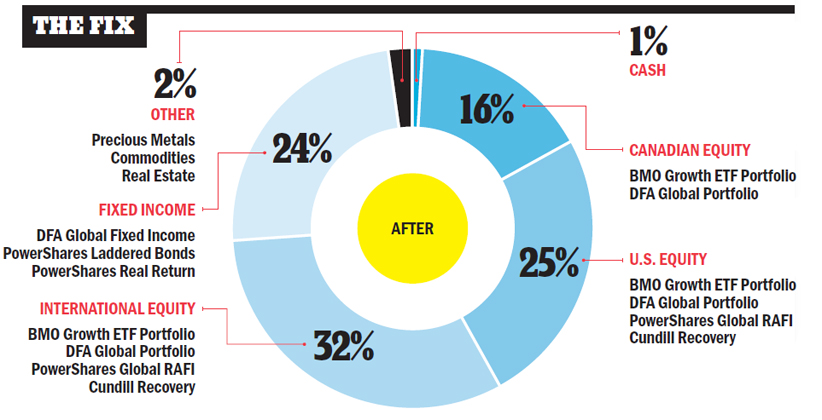

Rather than recommend an all-ETF portfolio, de Thomasis prefers index mutual funds that tilt portfolios toward small-cap and value stocks, such as those available from Dimensional Fund Advisors (DFA) or Invesco PowerShares. Also in the mix are BMO ETFs that provide more traditional large-cap equity exposure to the major North American stock indexes as well as some currency hedging to smooth out fluctuations between the U.S. dollar and Canadian dollar. He uses one actively managed mutual fund, Cundill Recovery, for much of the global stock exposure. For fixed income, he leans to shorter-term bond funds and floating-rate securities in order to lower the risk of spikes in interest rates and thus declining long-term bond prices.

De Thomasis believes the couple can cut their total investment management and financial planning costs to an all-in fee of 1.5%, while being subjected to less stress.

Since markets tend to move in three- to six-year cycles, de Thomasis would strive to rebalance the major asset classes whenever one strays 20% away from the target range, whether up or down.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Financial planner Tony de Thomasis, of De Thomas Financial Corp., says the couple are moderate-risk investors and should be comfortable with an asset allocation of 75% equities to 25% bonds and cash. As retirement approaches and if markets cooperate, portfolios would be gradually rebalanced to raise the fixed-income weight by 8% every five years or so.

Rather than recommend an all-ETF portfolio, de Thomasis prefers index mutual funds that tilt portfolios toward small-cap and value stocks, such as those available from Dimensional Fund Advisors (DFA) or Invesco PowerShares. Also in the mix are BMO ETFs that provide more traditional large-cap equity exposure to the major North American stock indexes as well as some currency hedging to smooth out fluctuations between the U.S. dollar and Canadian dollar. He uses one actively managed mutual fund, Cundill Recovery, for much of the global stock exposure. For fixed income, he leans to shorter-term bond funds and floating-rate securities in order to lower the risk of spikes in interest rates and thus declining long-term bond prices.

De Thomasis believes the couple can cut their total investment management and financial planning costs to an all-in fee of 1.5%, while being subjected to less stress.

Since markets tend to move in three- to six-year cycles, de Thomasis would strive to rebalance the major asset classes whenever one strays 20% away from the target range, whether up or down.

Do you want a portfolio makeover from MoneySense? If so, send an email describing your situation to [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find out which Canadian robo-advisors offer the lowest fees, helpful support, best returns, and most account types with the...

From passive index funds to active managers and DIY portfolios, here’s how to approach Canadian REIT investing in today’s...

This more sophisticated alternative to the 60/40 portfolio promises to avoid down years like 2022. Is it achievable for...

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...

The tax-free savings account is a great wealth-building tool, but it’s sadly misunderstood. Here are seven TFSA features Canadians...

Canada’s original asset-allocation ETF is still a good all-in-one investment, but it can have its flaws. Here are add-ons...

Of the many and diverse funds devoted to the Canadian banking sector, make sure yours has the right allocation...