Investors see value, but why won’t they act on it?

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

Advertisement

Investors continue to favour higher-fee active investments when lower-fee passive strategies are clearly better for them

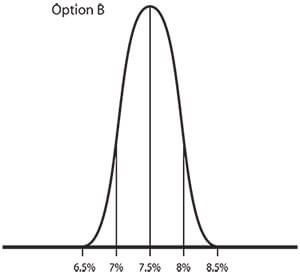

Option B (Beta-replicating) is predicated on mimicking a market.

Option B (Beta-replicating) is predicated on mimicking a market.

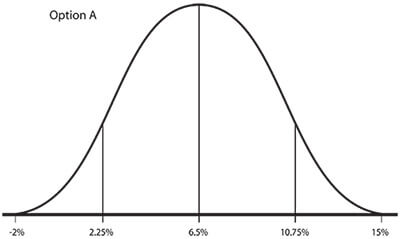

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

In my examples I’ll use a market return of 8% and then deduct the average cost of the products to determine the expected market return. Let’s assume that traditional active products (for example, F Class mutual funds) cost 1.5% and traditional passive products (for example, market-tracking ETFs) cost 0.5%. Those costs are likely a bit high, but the important thing to note here is that the difference in cost is about 1 percentage point.

![]()

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Robinhood’s WonderFi acquisition closes as Shopify adds US$3 billion to its buyback plan and Apotex targets a $1-billion IPO.

Leaving a TFSA to a U.S. spouse can trigger complex IRS reporting and costly tax issues. Here’s why some...

Wealth building starts with small, consistent habits. Here’s how young Canadians can save, invest and grow their net worth...

Canadian bank earnings season delivered higher profits, lower credit-loss provisions and dividend increases across much of the sector.

Gig workers and freelancers face uneven cash flow, but experts say consistent investing is still possible with the right...

Canadian depository receipts may offer convenience and accessibility, but they come with numerous trade-offs investors should be mindful of.