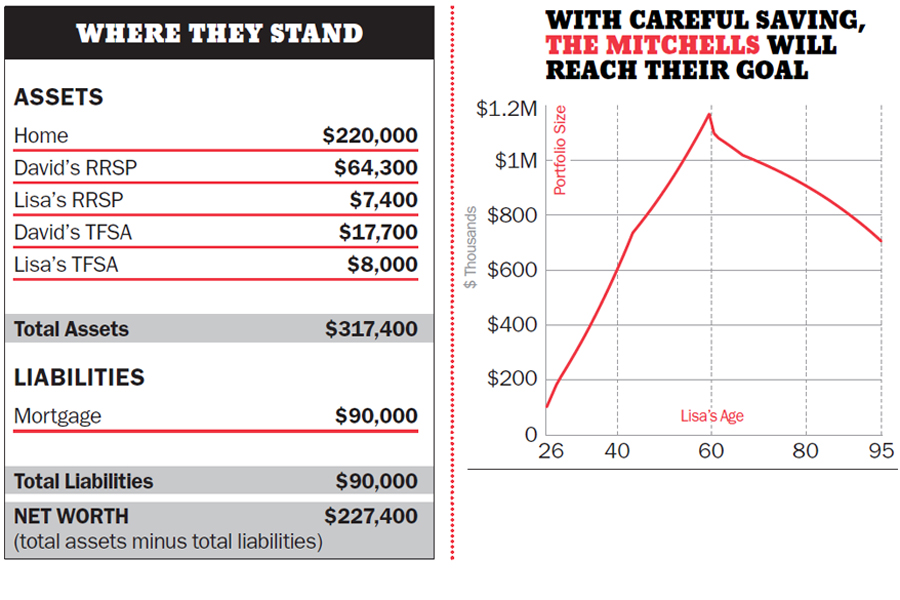

Millionaires by age 50

This couple is on track to reach financial independence earlier than most.

Advertisement

This couple is on track to reach financial independence earlier than most.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Shopify and energy companies delivered strong quarterly results, while Telus posted a steep loss. Catch up on this week's...

Strategy sold millions in Bitcoin. Learn why, how institutions are tackling quantum computing risks, and whether Coinbase is...

Crypto is going mainstream in Canada. A new OSC survey finds ownership has more than doubled, while advisor recommendations...

The CRA is cracking down on TFSA overcontributions. Learn how penalties work, how to correct mistakes, and when...

Why two people at the same life stage can be years apart financially, and how timing, housing, immigration and...

Struggling to stick to a budget? Learn how a simple cash flow system can help you save, spend confidently,...

Copper production lifted First Quantum, while Intact faced higher catastrophe claims. Catch up on the latest quarterly results from...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...