Am I on track to buy a home in five years?

If Rob and Lisa can make their home ownership dreams come true, but it will mean they'll have to start aggressively paying down their debt.

If Rob and Lisa can make their home ownership dreams come true, but it will mean they'll have to start aggressively paying down their debt.

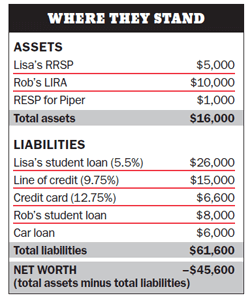

Rob Hamilton, 37, and Lisa Aldworth, 33, rent a two-bedroom apartment in Toronto with their one-year-old daughter, Piper. They would like to own a home, but they are $61,600 in debt. “We think saving for a down payment and buying our house in five years is a more realistic strategy,” says Lisa. They would love to stay in the city, but are also considering Guelph, Ont., since it is more affordable and closer to Lisa’s parents.

Each year this couple spends $9,600 on debt repayment, $5,000 for transportation, $18,000 for Piper’s daycare, and $11,820 for rent—a steal in Toronto. With incidentals their expenses hit $53,920. Rob makes $35,000 working for an arts organization while Lisa earns $74,000 as a social worker, giving them a combined after tax income of just $82,328. That leaves them with $28,408 annually to pay down debt and save for their house. “Should we contribute to RRSPs or stick to Tax-Free Savings Accounts?” asks Lisa. “My parents want to give us a $20,000 gift when we’re ready to buy. That will help. Are we on track?”

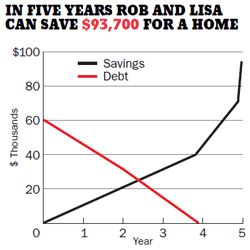

If Rob and Lisa start aggressively paying down their debt, they can buy a house in five years. “The focus has to be on both paying down the debt and saving,” says Barb Garbens, a fee-only financial planner in Toronto. “They have to do both to make the plan work.” With $28,400 a year in disposable income this couple can afford to nearly double their current debt repayment rate to $1,500 a month—or $18,000 a year. That would wipe out their debt in four years. “They should start by paying off the highest-rate debt first and work their way down to the student loan debt,” says Garbens.

With the remaining $10,000 in disposable income they should contribute $5,000 a year each to Tax-Free Savings Accounts to save for their down payment. “I wouldn’t do an RRSP,” says Garbens. “TFSAs give them more flexibility if they have an emergency. Plus, they can use that RRSP room more profitably later in their careers when they’re earning more.” Once their debt is paid off, they can put the $18,000 they were spending on debt towards their down payment, giving them a total of $73,000, with a 2% annual return compounded monthly. “Coupled with the $20,000 gift from Lisa’s parents, they’ll have about $93,000 to put towards their home in either Guelph or Toronto, whichever suits them best.”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Sponsored By

National Bank of Canada

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

This prepaid travel card eliminates foreign exchange charges on your purchases abroad, though the loading fees could irk some...

Food and beverage company expects organic growth of 4% in 2024.

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.