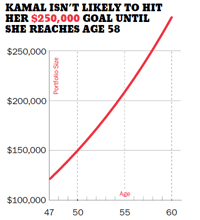

Am I on track to have $250,000 by age 55?

Kamal wants to retire early in order to travel and do volunteer work but isn't sure she'll be able to meet her savings goal.

Kamal wants to retire early in order to travel and do volunteer work but isn't sure she'll be able to meet her savings goal.

Kamal Mangat, 47, lives in Stoney Creek, Ont., where she works for Canada Post. Her husband Jagmohan, 53, works in shipping and handling and will retire in 12 years at age 65. “He’s a workaholic, but not me,” says Kamal, who describes herself as a spiritual person. Her goal? To travel and do volunteer work. “With three teenage kids and an active family, it doesn’t leave much time now for my passion—volunteering,” says Kamal. “But my husband and I have made a pact. If I can build my personal investments to $250,000 by age 55, then I can retire and not jeopardize any of our other family goals, such as paying off our mortgage and helping our kids pay for their university educations.”

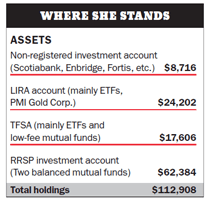

Kamal picks her own investments. Her portfolio of $112,908 includes dividend-paying stocks, exchange-traded funds and mutual funds. “I ?nd the 2% management expense ratios of the mutual funds in my RRSP fairly high, so I know this account needs some changes,” says Kamal. Her plan is to add $250 a month to the RRSP account until age 55. With average returns of 5% annually, she’s hoping that will be enough to meet her $250,000 goal.

Unfortunately, Kamal is not on track to have $250,000 by age 55, says Marilyn Trentos, investment adviser and portfolio manager with RBC Dominion Securities. By adding $250 a month to her RRSP, reinvesting dividends and factoring in a 5% average annual rate of return, Kamal will have only about $209,128 in her portfolio at age 55. To reach her goal of $250,000 in eight years, Kamal needs to increase her monthly RRSP contribution to a hefty $575 a month—an increase of $325 monthly. Otherwise, she will need to work three more years and retire at 58. “As an investment strategy, I’d suggest selling the high-fee mutual funds in her RRSP and instead hold blue-chip dividend-paying stocks in that account, with all dividends reinvested, much like her non-registered investment account,” says Trentos. “All of her other holdings are ?ne.” One ?nal piece of advice? “When she’s picking her dividend-paying stocks she should try to ensure good diversification over various economic sectors, including gold, health care and technology. That will set her on the right track.”

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Presented By

Embark Student Corp.

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...