The elusive middle class

They can hardly define it but that won't stop politicians from promising to help the middle class

They can hardly define it but that won't stop politicians from promising to help the middle class

In July, Matthew and Larissa Powell got an unexpected bonus from the Government of Canada. Their usual $100-a-month Universal Child Care Benefit (UCCB) was boosted to $160. And because the increase was retroactive, the Burlington, Ont., couple discovered a $520 deposit in their bank account. It was advertised as a small gift to hardworking Canadian families, courtesy of Stephen Harper.

With the election looming in October, the Powells—traditionally Liberal voters—saw the cash as a naked vote grab by the Conservatives. “The timing is a little suspicious,” Larissa says, “coming just before the election and in time to pay for all the back-to-school stuff.”

That UCCB cheque represented the first political football of the 2015 election. Liberal leader Justin Trudeau, who has three children, lobbed it back, donating his family’s annual entitlement of $3,400 to charity. “When it comes to child benefits, fair doesn’t mean giving everyone the same thing, it means giving people what they really need,” he said at the time. As for the Powells, they kept the cash, rolling it into education savings for their three-year-old son Owen. “We can use it,” says Larissa. “Money is money.”

Enhancement to the federal child tax benefit—which will cost the government almost $3 billion this year—is just one of an array of financial goodies Canada’s three major political parties are rolling out to woo coveted middle-class voters. There’s a problem, though: the middle class isn’t an easy-to-peg interest group in the same way as, say, small business owners or the local 420 Cannabis Community. As a result, it’s a bit of a mug’s game when it comes to establishing how much—or little—the middle class is struggling and what kind of policy changes would at least win votes, if not actually have a positive impact.

What is clear is those middle-class issues will play an influential role in how Canadians vote on October 19. The main reason, argues Philip Cross, Calgary economist and former chief economic analyst for StatsCan, is that most of us self-identify as middle class. “That’s why every politician says, ‘I’m going to help the middle class.’ It resonates with people—they think, ‘Oh, he’s going to help me!’”

Which political party is better for your portfolio? »

Pity Canada’s voters trying to get a handle on the state of the middle class when Canada’s political parties can’t even agree on a definition of what it is. The Conservatives peg the middle class as those earning up to $120,000 in household income. Middle-class families, they say, are better off than ever; their income is up and the Harper government’s record of tax reductions has helped “every single Canadian family in this country.”

The Liberals, however, say middle-class families are struggling. Trudeau has focused laser-like on a single tax bracket: families earning between $44,701 and $89,401, claiming that “for 10 years, Harper has been ignoring the people who do most of the heavy lifting in our economy, who work longer and longer hours for an ever-shrinking piece of the pie.”

And the NDP? They define middle class as the middle 60% of income earners whom Thomas Mulcair says “are working harder but falling further and further behind.”

All of this political posturing ignores the fact that the middle-class experience doesn’t just hang on how much money you make. As those struggling to own a home or find affordable daycare in one of Canada’s major cities can attest, even $120,000 doesn’t always cut it.

“Class is about mind-set and attitudes and values,” says Cross. What it’s really about, he reasons, is how much money is left over after the bills are paid, and whether you can afford to lead a comfortable life with a home of your own, maybe a car in the garage and a chance to take a vacation to Disney World. It hinges on things like whether you’ve been able to get an education and whether you can afford to help your kids do the same. And it’s about whether you have hope for the future. Those things are “impossible to measure,” explains Cross. “So we end up looking at income.”

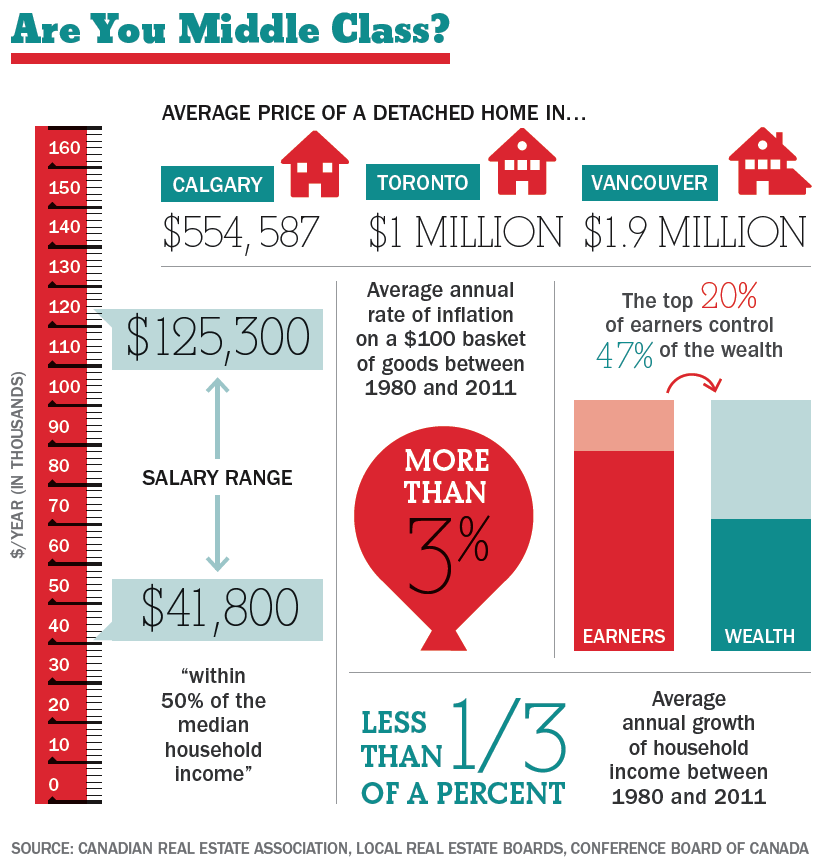

While various interest groups may quibble over exactly how to slice and dice the numbers, Queens University economist Charles Beach says defining the middle class as those whose earnings fall within 50% of the median household income “is as good a definition as any.”

By that measure, the middle-class family in Canada earns between $41,800 and $125,300. That’s a broad swath of the population. And yet, the question of just how well the middle class is doing remains a valid one.

What are the overall trends? Are middle-class families struggling to keep their heads above water, living paycheque to paycheque and piling on debt? Or are they thriving, saving for even sunnier days in retirement? The answer depends on where you live, what segment of the economy you’re employed in, whether you’ve managed to squirrel away a nest egg, and even your age or your stage in life.

Harper vs. Trudeau: Who has the better tax plan for you? »

Calgary high school teacher Laura Schwartz feels as if she’s pedalling just to stay in place. The 55-year-old’s salary has been frozen for the last three years at about $88,000. Out of that, she says one-third goes to payroll deductions for taxes and pension payments, and Schwartz—who is single—pays her mortgage, property tax, utilities and home insurance for her three-bedroom Calgary duplex and owns a car. She’s left with about $1,300 a month to live on.

But even though Schwartz’s salary isn’t rising, the cost of living is—at an average of 1.51% annually over the last three years, according to the Bank of Canada. “Every time I go to the grocery store it costs me $90,” she says. “And that’s just for a few basics.” She’s not wrong. Food prices are up more than 3% this year over last year. Had Schwartz been receiving cost-of-living increases to her salary, she’d earn $92,000 this year—so one could argue her spending power is already down. “Technically I’m making good money and I’m fully employed,” she says. “But I feel more like the working poor.”

It is. And it isn’t. By almost any measure, real income has been rising in recent years, after adjusting for inflation. In 2013 (the latest year for which stats are available) the median total household income in Canada rose to $76,550, up 12% from $68,410 in 2009. But look at those figures over the past 30 years and the direction is down. In fact, from 1980 to 2011, total household income in Canada grew by less than one-third of a percent per year (averaged out)—considerably less than inflation. “Middle-class incomes have risen over the long run, but really quite slowly,” says Beach. “And much of this is due to the growth of two-earner households, so that families have to work longer hours in total to keep their real incomes up.”

The economists we spoke with contend that most of the damage was done during the 1990s recession and we’ve yet to fully recover. What’s more, middle-class incomes haven’t been rising as fast as incomes at the top end of the distribution. “The middle-class share of total family income peaked in the late ’70s at about 56%, and they’re now at about 51%,” says Beach. Meanwhile, the top 20% of earners have seen their share of total family income grow to about 47% from about 42% during this same time period. “So liberal types have focused on the fact the income share of the middle class has been declining. The big winners are on the top end.”

Political leaders have approached the issue of putting more money in the hands of citizens from different angles. Last year, Stephen Harper introduced income splitting for families with kids under 18, to a maximum of $2,000 in savings for taxpayers with incomes up to $230,000—a measure that helps families with two parents in different income brackets, but not Schwartz. The same goes for Harper’s enriched (but taxable) child tax benefit.

If elected, the NDP would introduce a national childcare program at $15 per day to help families struggling with daycare costs. That’s won’t help Schwarz either, but Trudeau’s plan might. The Liberals have pledged to raise taxes for Canada’s richest earners and give to the middle class by lowering the current federal tax rate on incomes between $44,701 and $89,401 from 22% to 20.5%. For Schwartz it would mean an extra $1,320 in her pocket annually.

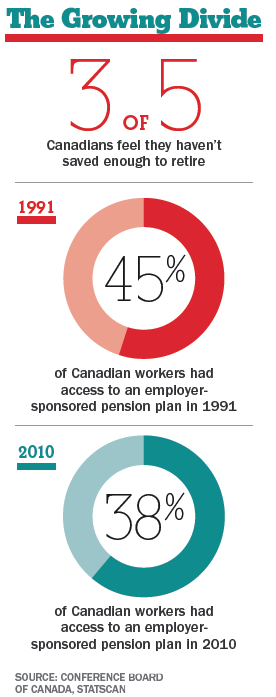

Whether income growth is, in fact, stalling or even falling behind inflation, it has become popular wisdom that middle-class Canadians are now in a squeeze that leaves them unable to save adequately for retirement. Then again, the very notion of a retirement savings crisis is unfounded, assures pension expert Malcolm Hamilton. In the recent C.D. Howe Institute report, “Do Canadians Save Too Little?,” Hamilton says the undersaving crisis is exaggerated, in large part due to too much reliance on the accuracy of the current StatsCan household saving rate and the misconception that we should target retirement income that is 70% of what we made while working.

“Canadians are reasonably well prepared for retirement,” he writes. “Most save more than the 5% household saving rate. Most can retire comfortably on less than the traditional 70% replacement target. The greatest challenges come early in their adult lives when the burdens of acquiring a home and supporting young children strain the family budget. After that, things get easier.”

Priced out

Priced outAlthough how much you earn has a direct impact on where you see yourself in the economic spectrum, one thing most economists agree on is that if you own a home, you’ve become part of the middle class, or higher.

But thirtysomething Toronto couple Bridget Light-Craig and Jonathan Craig know that essential trapping of a middle-class lifestyle has become increasingly elusive in some parts of the country. The burden of acquiring a home is particularly heavy in some of Canada’s biggest cities, where home prices have shot through the roof.

Despite a small inheritance and some help from their parents, the couple have been searching for a home they can afford for over a year now. Bridget, a digital manager for a magazine, and Jonathan, a self-employed special effects makeup artist, started off with a wish list that included a detached home in their desired neighbourhood—trendy Parkdale, just west of Toronto’s downtown core. Their target price: $500,000 to $600,000.

“So many things have not worked out,” laments Bridget. “Either people get there ahead of you, because the market is crazy. Or something turns out to be wrong with the house—like knob and tube wiring throughout. We’re willing to take on some renovations, but that’s scary.” Although the couple scaled back expectations, they still haven’t found a property that fits the bill. “We’re a bit burnt out.”

Their struggle will ring a bell for would-be home buyers across the country, but nowhere more so than in Vancouver, where home prices have risen from an average $701,000 for a detached home in 2005 to $1.9 million last year. Even having a solid job and a good education doesn’t guarantee you can afford to live in B.C.’s largest city.

Eveline Xia grew up in Vancouver and has a Master’s in environmental science, but the 29-year-old can’t hope to buy a home there now. This past spring, after reading a letter to the editor in the local paper about a doctor who planned to move from the city because he couldn’t afford housing, Xia asked people to share their frustrations under the hashtag #donthaveamillion.

The Twitter campaign struck a chord in the city, where the average family spends 70% of its income on housing, instead of the widely recommended 30%. Xia was inundated with interview requests and organized an affordable housing movement that she hoped would encourage Vancouver’s powers-that-be to look at the issue and perhaps (like uber-capitalist Hong Kong) offer subsidized housing for those priced out of their own city. The response: “There’s nothing we can do.” Xia is now considering a move to Vancouver Island, where housing costs are at least within reach.

The overheating in housing may be most acute in Vancouver but data from the most recent National Household Survey (2011) show the challenge is much wider. A quarter of Canadian households were spending more than 30% of their income on housing, the threshold set by the Canadian Mortgage and Housing Corporation (CMHC) in 1986. Unfortunately, for houseless or house-poor Canadians like Bridget and Jonathan in Toronto, there are no easy solutions. Part of the problem: our housing market operates on two speeds. Housing in Toronto and Vancouver has soared in cost, but elsewhere, such as some markets in Alberta and Saskatchewan, prices have actually dropped. From a policy perspective, and assuming they even could, how would political policy-makers cool some specific markets without cooling them all? (To see Romana King’s Home Owner column for two ways to cool the housing market, download the September/October issue of MoneySense magazine)

The Conservative government has tried tightening mortgage rules, to limit its own exposure to the housing market through the CMHC. But uninsured mortgages are filling the gap for wannabe home owners who can’t muster a 20% down payment. Meanwhile, both the Liberals and the NDP have floated the idea of tax breaks to encourage construction of rental housing, which might take some pressure off house prices.

Ottawa’s Olga and Yuri Sesiakin read in the financial pages about couples with $2 million in assets saved for retirement and they just laugh. The Sesiakins, who immigrated from Moldova in 1993 to escape civil war, came here to raise their kids “in a peaceful country,” says Olga. “I knew nothing about Canada. There was only one picture in the library and it was of the tundra. I thought, ‘Jesus, where am I going?’”

After studying English intensively, Olga launched a business as an esthetician and Yuri got his Master’s degree in engineering. Now, at 45 and 51, respectively, the couple earn an after-tax income of about $108,000 per year and own a $560,000 house in Ottawa, as well as two cars, and a time-share in the Dominican Republic. They also help support Yuri’s father in Moldova and have two kids (Daniel, 22, and Tanya, 18) who are both getting an education.

But, while all looks hunky dory on the surface, the Sesiakins owe $164,000 on their home and $110,000 on a line of credit. Meanwhile, they’ve managed to save just $146,000 (most of it in RRSPs). “There’s nothing left at the end of the month,” complains Olga. The Sesiakins’ main concern seems to be their lack of a pension and savings going toward a comfortable retirement. Olga is self-employed and although Yuri’s employer once had a robust pension plan for employees, “they stopped it just before he started with them.” What’s more, Olga worries that if the economy collapses, even the little they’ve managed to save could drop “to $40,000 or even nothing.” With many years of prime earning ahead of them, however, as well as the fact the kids are already off to university, this could be another example of the prevalent overworrying Malcolm Hamilton cites in his study.

For people like the Sesiakins, who seek some kind of assurance that they won’t have to work as Walmart greeters in retirement, the country’s two opposition parties could appear to offer the most comfort. Both would make an expanded Canadian Pension Plan (CPP) compulsory and would reverse Harper’s decision to have Canadians wait until age 67 to collect Old Age Security (OAS). The key difference: Mulcair would make his CPP changes effective immediately, while Trudeau favours a gradual approach. Of course, one could also argue that the only reason either of the opposition leaders can even mull such policy options is because of the continuing strength of the Canadian economy under the current government.

Indeed, Harper has made it easier for all Canadians to build their retirement nest egg, if they so choose: he nearly doubled the Tax-Free Savings Account (TFSA) limit from $5,500 to $10,000. (To get your bigger TFSA working for you now, download the September/October issue of MoneySense magazine) He has been generally hostile to the idea of a mandatory enhancement to the CPP, but with an election looming Harper said in May he’d explore the idea of allowing Canadians to voluntarily make additional CPP contributions in return for higher payouts.

The shrinking middle

The shrinking middleIt used to be that a good union job offered security and enough money to pay the bills, buy a house and car and secure a pension. That was then. This is now, says Greg Shepley, an auto-worker in his early 50s.

For 12 years, Shepley worked as a mechanic at the Ford plant in Talbotville, Ont., where he earned $40 per hour—enough to live a solidly middle-class life. His wife stayed at home with the kids, who both went to university. But in 2011, the plant closed. For a year, Shepley got by on unemployment with a top-up from Ford. But when a job opened up at the company’s plant in Oakville, Ont., he jumped at the chance—even though it meant buying a new home within commuting distance and taking a demotion, a $5 an hour pay cut and a pension reduction.

Shepley counts himself lucky. He knows others who took a buyout from Ford, figuring they’d pick up another job and bank the cash. The problem: “Times have changed,” says Shepley. “Those jobs that were out there when we graduated high school are gone and some of those guys are on welfare now.” Indeed, says Cross, “the workers who’ve lost the most ground are those with lower skills and education.” And the largest source of that downward pressure can be traced to the decline of Canada’s manufacturing industry.

When it comes to nurturing the country’s industrial heartland, both opposition parties accuse Harper’s Conservatives of focusing myopically on the oil and gas sector, allowing as many as 330,000 good manufacturing jobs to evaporate. If voted in, the NDP believe they’ll reverse the trend by offering tax relief and tax credits to small businesses and manufacturers so they can remain competitive. Trudeau claims he’d work to ensure “middle-class Canadians can skill and re-skill for the jobs of today—and the jobs of tomorrow.” He suggests we need a “national manufacturing strategy” to encourage global investment and boost job prospects in places like southwestern Ontario. (At the time of this story, he has yet to elaborate on that plan.)

Meanwhile, with the election looming, Harper recently handed out a $59-million loan to Toyota Canada aimed at maintaining 8,000 jobs. He says the Conservatives have “taken decisive action to create the type of environment in which Canadian businesses prosper, reducing taxes and red tape… and making Canada an attractive destination for foreign direct investment.”

While factory workers are clinging by their fingernails to a middle-class lifestyle, there’s another group that is having a heck of a lot of trouble getting there in the first place. Andrew Crozier has been living with his parents in Etobicoke, Ont., since finishing an economics and finance co-op program at the University of Guelph in 2013, followed by a college certificate in advertising copy-writing. Since then, he’s been working at unpaid internships. “I’ve done five or six of them, but never a full-time job,” he says. At one point, Crozier worked at No Frills to earn some cash. “I was a university graduate with a finance degree and I was stocking shelves all day,” he says. “Someone would say, ‘Can you find me some Dunkaroos?’ and all I could think was, ‘What am I doing?’”

In spite of Crozier’s experience, education levels have been rising in Canada. According to StatsCan, the proportion of adults with a college diploma or a university degree rose to 50% from 39% between 1999 and 2009. And student debt levels are rising in concert, ranging from an average of $13,000 per student in Quebec to $28,000 in Ontario and the Maritimes. Young people are “having trouble landing that first good job,” says Cross. In fact, fully a third of 25- to 29-year-old post-secondary grads are working low-skilled jobs in Canada—the highest number of any member nation of the Organization for Economic Development and Cooperation. “It could be that employers are saying that despite all this education, young people don’t possess the skills that they want,” says Cross. In other words, they’re not getting the degrees that match the employment opportunities available.

All three parties are focused on making it easier for students to graduate with a manageable amount of debt, but offer slightly different ways of making that happen. Potential initiatives range from expanding the Canada Student Grants program (Conservatives and NDP), to making student loans repayable according to income earned (mused by Trudeau as far back as 2013). Mulcair has also said he’d implement a $15 per hour federal minimum wage (which might help young people fund their schooling). But none of these measures are likely to vault folks like Crozier directly into prosperity. Or even get them out of the basement.

Ultimately, says Cross, political parties lump everyone together in the same pot, stir it up and then treat the “middle class” as a homogeneous group—and that isn’t likely to result in policies that benefit those who really need them.

Cross contends that across-the-board measures like tax cuts are rarely the best answer if governments are really striving to help those struggling to achieve or maintain middle-class status. “If you introduce measures that are going to help 60% or 80% of the population, you’re going to end up helping a lot of people who don’t need help.” The best policies “concentrate our limited resources on those small groups of people that could benefit a great deal.”

But targeting small groups of the public is less appealing to our politicians who are far more interested in targeting large amounts of voters. So expect to hear phrases such as “fairness for the middle class” multiply before we hit the polls on October 19. When Canadians decide to weigh middle-class issues in this election, whether tied to income inequality, debt, job growth or retirement security, they will be voting in different ways.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Sponsored By

National Bank of Canada

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Managing lifestyle creep is challenging financially and psychologically, especially with inflation. Expert strategies keep day-to-day spending in check.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...