Frugal living not required

The Fraser family can still save enough for retirement even with setbacks and debt.

The Fraser family can still save enough for retirement even with setbacks and debt.

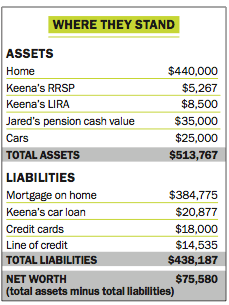

Jared and Keena Fraser are hard-working people who have fallen on hard times. Despite pulling in a combined income of $99,000—Jared works as a nurse, Keena runs a home daycare—the Saskatchewan couple’s resources have been stretched to the limit due to health problems that put them deep into debt, and even have them contemplating selling their home. The distressing truth is the Frasers, parents to two boys, are entering their fifties with a net worth of only $75,580—and debts totalling a whopping $438,187. The notion of ever being able to enjoy their golden years seems like an impossible dream.

“We’ve had several setbacks in the last few years,” says Keena, 48. “We built a custom home for ourselves in 2009 to house my growing daycare business and it cost more than we planned. Then I had to have surgery and all the money we had saved and more was needed to pay the bills while I was recuperating. We are worried that with so little in savings we won’t have anything for retirement. Time is not on our side.”

The Frasers (whose names we’ve changed to protect privacy) have spent hours pouring over their bank and credit card statements, trying to come up with a plan that will allow them to pay off their debt quickly and save enough for retirement. It hasn’t been easy. In fact, the new home they enjoyed building five years ago now feels like a noose around their necks. “We got in way over our heads,” admits Jared, 51. “More space meant more furniture and a landscaped yard for Keena’s daycare business. We didn’t realize all the extra expenses there would be.”

It wasn’t long before the Frasers started using their line of credit and credit cards to keep up with the unforeseen expenses. Still, neither Jared or Keena actually regret upsizing their home to grow the daycare, because it enabled them to help their oldest son. Kevin, then in junior high school, was having behavioural problems and several times a month the school principal would call Keena at work to tell her they were sending him home. “My office jobs weren’t flexible so I had to find a way to be with my son when he needed me and at the same time, earn an income,” she says. “I felt the direction he was going in would land him in jail.”

To her surprise, it was just months after starting her daycare business that she observed a big change in Kevin. “He started to enjoy school for the first time in a long time. I saw the difference in his attitude right away.” Today, Kevin’s 19 and attending the local university, with plans to eventually enroll in medical school. “He was our best investment,” says Jared. “We’re proud of him and happy to see his progress.”

Just two years ago the Frasers thought they were on the right track and making real progress on paying down their debt. The bank had allowed them to re-mortgage their home and consolidate some of their accounts, reducing their annual payments. But then adversity struck again: Keena was told she needed stomach surgery and the recovery was longer than expected. “There were complications and I wasn’t able to return to work as quickly as I’d planned,” she says. “This meant less income for a while and the credit charges rose a little more.”

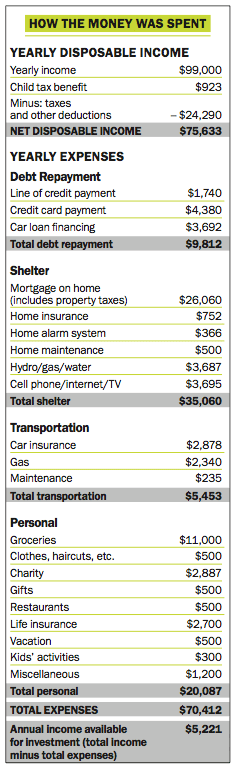

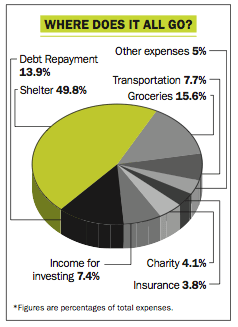

Thankfully, Keena is healthy again and back running her home daycare, but she and Jared’s financial problems are now more imposing then ever. Today, they have $32,535 in consumer debt, a $20,877 car loan and $384,775 left on the mortgage of their $440,000 home. While the couple would like to get started on a retirement savings plan, they’re not even sure that’s possible. Right now, the Frasers are paying $9,812 annually toward their consumer debt (including car payments), with the goal of eliminating it within five years. After all of their other expenses are taken care of (including mortgage payments), that leaves them with $5,221 a year in disposable income—an amount they’re at loggerheads over what to do with.

For his part, Jared believes they should be solely focused on debt repayment. But Keena isn’t so sure that’s best in the long run. She’d like to use the $5,221 to start a savings and investing plan. She’s taken some workshops in do-it-yourself investing and is interested in putting her new knowledge to work.

Keena’s main concern is that apart from the equity in their home, they don’t have much else in the way of savings: just $5,267 of mutual funds in Keena’s RRSP and another $8,500 in her LIRA, as well as the $35,000 cash value of Jared’s defined benefit pension plan that he’s contributed to for 10 years through his workplace. He’ll receive $2,000 a month if he retires at 65, but retiring any earlier would mean his pension would be only about $1,500 a month—much less than the couple feels they need to live comfortably.

One solution the couple does agree on is that they need to cut costs. Unfortunately, in most areas, their annual expenses are quite modest. While their $11,000 annual grocery bill is higher then they’d like, that’s an expense that can’t be cut because Keena needs to eat a restrictive diet to remain healthy. Another expense they’re reevaluating is the $2,887 they donate annually to their church. “We’d consider giving only half of that for a couple of years if it would help get us out of debt quicker,” says Jared. “But donating to our church is important to us.” Finally, the Frasers have two term life insurance policies totalling about $700,000 that they are paying $2,700 annually for. “Should we just sell them?” wonders Keena.

A far more radical scenario the couple is contemplating involves selling their house, downsizing to a $300,000 condo and paying off all of their consumer debt immediately. “If I close my daycare, the condo would be a viable option,” says Keena, adding that a return to office work—albeit at a lower salary—would make her life a bit less stressful. “I have four little boys in my daycare that are between one and two years old. I love being with them but it’s challenging,” she says. Still, all of this would be an absolute last resort for the couple. “If there’s a way to keep our house and save for retirement, we’d definitely love to hear it,” says Keena.

One thing working in the Frasers’ favour is their frugality and commitment to sacrifice in order to make growing their retirement nest egg a reality. “We’re not big spenders,” says Keena, noting that she and Jared enjoy simple pleasures. They love murder mysteries and participating in their local church, although one day they’d love to indulge a bit and take their family on a vacation to a warmer climate—something many of their friends rave about. “This is something that happens when you’ve lived in cold Saskatoon for a while,” laughs Jared. “We’re really looking forward to budgeting for some sunshine.” Mainly, though, the Frasers would like to get their financial house in order to make sure the sun hasn’t already set on their golden years.

Jared and Keena Fraser have transformed their lives after being thrown several curve-balls. “They took care of their son and family and created a financial solution—Keena’s daycare business—to manage it, which was very creative,” says Vancouver money coach Annie Kvick. Tatiana Terekhova, a certified financial analyst with Fairsplit in Oakville, Ont., is in agreement: “The Frasers work at jobs they love and built their dream home to accommodate their family and income needs. Of course, it comes with a price-tag, but with a focused plan they can meet their goals.”

It’s never too late to catch up and Jared and Keena are in much better shape than they think. Here’s what the Frasers should do to get their finances back on track.

Prioritize debt. Both experts agree that the couple’s No. 1 priority is to pay down their consumer debt—not saving to invest. They have two options, the first of which should be to talk to their bank about consolidating their debt at an even lower interest rate. If they can get a $32,535 consolidation loan at 8%, which Terekhova says is doable, they should be able to pay $12,784 annually toward the debt. That payment will be made up of: the $6,120 they’re paying now to service their consumer debt (minus the car loan), $1,443 from halving their charitable donation, and their entire $5,221 annual cash surplus. If they do this, all of their consumer and car debt will be paid off in three years. They can then go back to making their full charitable donation.

If they can’t consolidate their debt in this manner, they still have another viable option: prioritizing debt. They should first tackle their 19.9% credit card debt, then the 11.99% credit card debt, followed by the line of credit at 8% and finally the car loan at 4%. “If they make payments using the same schedule as the first scenario, they can be debt-free—including the car loan—in three years and 10 months,” says Kvick. “If they don’t reduce 50% of their donation money, it will take them four years and two months to be debt-free.”

Keep the house. The Frasers have a huge $384,775 mortgage on their home but selling it now makes no financial sense, says Terekhova. “If they move, much of their $75,580 net worth will evaporate after legal fees, commissions, land transfer taxes and moving costs. And moving to a condo will restrict their living and work options. They should stay put.”

Once the couple has paid off their consumer debt, about $15,000 annually will be available to invest ($9,812 from an end-to-debt repayment and $5,221 from annual income available for investment). For the first year after the debt is paid off—late 2018—they should put that $15,000 towards an emergency fund—perhaps in their TFSAs. The following year—2019—they should divvy up the money as follows: 50% towards the principal of their home, 25% to their TFSAs and the final 25% for some travel. “They don’t have to wait until retirement to go south or take a nice vacation,” says Kvick. “They can do that in three years.”

Diversify the daycare business. Returning to office work likely won’t pay enough to make it feasible for the Frasers to give up the daycare, says Terekhova. “Keena gets a lot of deductions for that business and these won’t be available with a full-time office job. She should only consider office work if she gets a gold-plated benefits plan that includes disability insurance, additional medical coverage and a pension.” In the meantime, Keena should expand her business and consider adding tutoring. “Parents pay $20 an hour to have tutors help their kids do their homework,” says Terekhova. “This is a great way to diversify out of the more stressful daycare work.”

Count on the company pension. The couple is fortunate that Jared has a good defined-benefit pension plan through his workplace. This will be their main savings vehicle. “Just because you don’t see a monthly statement doesn’t mean the pension money is not growing,” says Terekhova. And with Jared’s pension paying them $2,000 per month starting at age 65, plus Jared’s and Keena’s CPP and OAS payments each adding another $1,000 of monthly income, the couple will be able to live very comfortably in retirement.

At age 65, they can then decide whether or not to downsize to a retirement community. “They should only do that because they feel they want to, not because they have to,” says Kvick. With life insurance payments gone at 65, a much-reduced home mortgage and more than $100,000 in savings in their TFSAs, RRSPs and LIRAs, the Frasers, despite the ordeal they’ve endured, should be just fine.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Sponsored By

National Bank of Canada

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

This prepaid travel card eliminates foreign exchange charges on your purchases abroad, though the loading fees could irk some...

Food and beverage company expects organic growth of 4% in 2024.

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.