The true price of financial advice

Transparency shines a light on the value of paying for help when investing

Advertisement

Transparency shines a light on the value of paying for help when investing

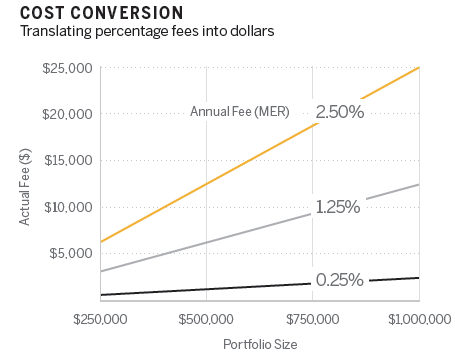

To put that in perspective, the minimum wage in Ontario will climb to $11.40 per hour this year. Sturdy retirees who are willing to work 40 hours a week for 52 weeks a year for minimum wage will make $23,713 before taxes. Alternatively, if they can slash their investment-related expenses, they might be able to save more than they’d earn, after tax.

The good news is there are several ways to cut fees, some without cutting out an advisor. Broadly speaking there are three ways to do it. You can keep the individualized advice but move to a portfolio of low-fee funds. Or you can opt to do your own planning and choose a low-fee portfolio of professionally managed funds. Finally, those with sufficient knowledge and experience can do it on their own and cut costs to the bone.

To put that in perspective, the minimum wage in Ontario will climb to $11.40 per hour this year. Sturdy retirees who are willing to work 40 hours a week for 52 weeks a year for minimum wage will make $23,713 before taxes. Alternatively, if they can slash their investment-related expenses, they might be able to save more than they’d earn, after tax.

The good news is there are several ways to cut fees, some without cutting out an advisor. Broadly speaking there are three ways to do it. You can keep the individualized advice but move to a portfolio of low-fee funds. Or you can opt to do your own planning and choose a low-fee portfolio of professionally managed funds. Finally, those with sufficient knowledge and experience can do it on their own and cut costs to the bone.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Cogeco’s Canadian wireless launch arrives amid downgraded outlook, falling U.S. revenue, and analyst concerns.

A MoneySense reader asks what tax and probate implications she might face if she inherits a rental property held...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

The Index Matrix vividly illustrates how different assets performed in the past. Here’s how Canadians can use it to...

Canadian investors have several options for investing in bitcoin and other cryptocurrencies. Here are the pros and cons of...

Both mutual funds and ETFs have their place, and the right one for you comes down to your financial...

A MoneySense reader wants to give money to his spouse to invest. Can he avoid Canada’s income attribution rules?

These top 10 Canadian momentum stocks all returned more than 40% over the past three months.

A MoneySense reader wants input on the tax implications of her investment withdrawals, but she can’t get a straight...