Pitfalls to avoid when investing in sector ETFs

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the sector.

Advertisement

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the sector.

Despite a large and growing body of evidence showing that most investors are best served by low-cost, broadly diversified index funds, some still prefer to take a more hands-on approach with their portfolios. That can range from picking individual stocks to making tactical bets on certain countries, such as maintaining a home bias toward Canadian equities or overweighting U.S. markets.

Sitting somewhere in between is sector investing. While there is no strict definition, it can be thought of as deliberately over- or underweighting specific parts of the market. Instead of owning the entire market, you are making targeted bets on areas like financials, energy, or technology based on your outlook.

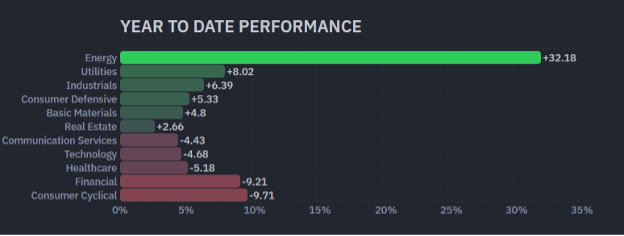

This is top-of-mind right now due to the sector rotation we have experienced over the past six months. According to Finviz data as of March 19, the U.S. energy sector is up 32.18% year to date, while some of the mega-cap-heavy areas tied to the Magnificent Seven have lagged. Communication services is down 4.43%, technology is down 9.21%, and consumer cyclical is down 9.71%.

Source: Finviz

Part of this comes down to macro forces. Rising geopolitical tensions, including the U.S.–Israel–Iran conflict, have sharply pushed energy prices higher, benefiting oil and gas producers. At the same time, some of the enthusiasm around artificial intelligence has cooled, with investors reassessing valuations and near-term earnings expectations for large-cap tech.

The challenge is that, while sector investing itself as a strategy has evolved, the Canadian sector ETF landscape has not kept pace in terms of fees.

In the U.S., investors have access to a wide range of low-cost options, most notably the Select Sector SPDR lineup from State Street, with management expense ratios (MERs) around 0.08%. These U.S. equity sector ETFs are also available in Canadian-dollar (including currency hedged) variants thanks to a partnership with BMO Global Asset Management at a 0.21% expense ratio.

In Canada, comparable domestic-focused offerings tend to be more expensive. A clear example is the iShares suite of Canadian sector equity ETFs, which track different industrial segments of the S&P/TSX but come with MERs closer to 0.6%.

More importantly, the way these Canadian equity sector ETFs are constructed can introduce unintended concentration risk. The limitations often come from the underlying index methodology of S&P Global rather than the ETF itself. Understanding this structural quirk is important before using any sector funds to express a sector view. Here is what to watch out for, along with some more thoughtfully constructed alternatives to consider.

By definition, sector investing already means overweighting one slice of the economy beyond its natural market-cap weight. That is expected.

The problem is that you can end up taking on a second layer of concentration without realizing it. Instead of your returns being driven by the broader forces affecting a sector, they can end up being dictated by just a handful of dominant companies within it, with their attendant risks.

In Canada, this issue largely comes down to how sector indices are constructed. Many Canadian sector ETFs, particularly those in the iShares lineup, track S&P/TSX capped sector indices. These indices apply a 25% cap on any single holding at each rebalance.

Caps are not unusual. They exist to prevent extreme cases, such as when Nortel Networks once exceeded 30% of the TSE 300, the leading Canadian benchmark of the 1990s. That is why its successor, the S&P/TSX Capped Composite Index, has a much tighter 10% limit. At the sector level, however, a 25% cap is so high that it often fails to meaningfully reduce concentration.

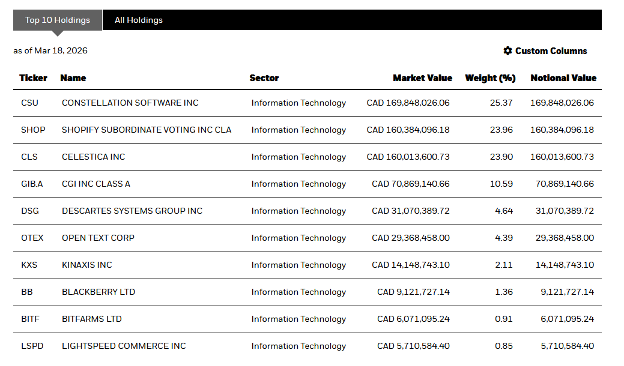

Take the Canadian technology sector as an example. The iShares S&P/TSX Capped Information Technology Index ETF (XIT) tracks just over 20 companies. In practice, roughly three-quarters of the portfolio ends up concentrated in just three names: Constellation Software, Shopify, and Celestica.

Source: iShares Canada

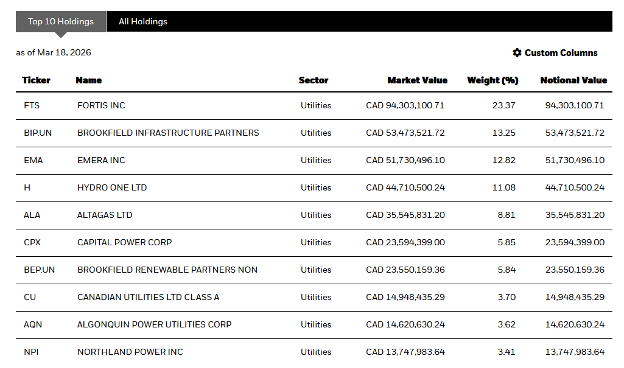

Similarly, the iShares S&P/TSX Capped Utilities Index ETF (XUT) is concentrated in Fortis, Brookfield Infrastructure Partners, Emera, and Hydro One. Together, these four companies account for roughly 60% of the portfolio. Again, a majority of the ETF’s risk and return is tied to a small group of stocks.

Source: iShares Canada

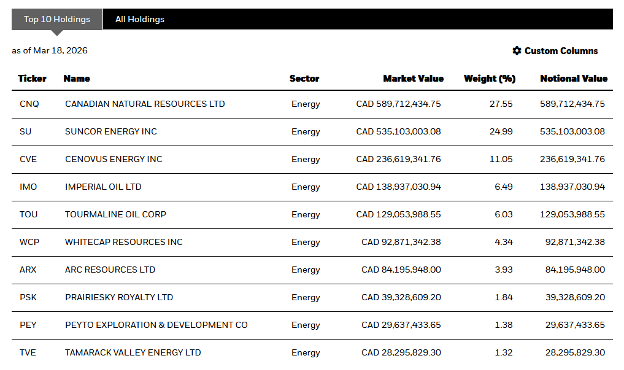

Even in one of Canada’s largest sectors—energy—the issue persists. The iShares S&P/TSX Capped Energy Index ETF (XEG) currently has Canadian Natural Resources between rebalances at 27.55%, with Suncor Energy at the 25% limit. Combined, those two holdings make up more than half of the portfolio.

Source: iShares Canada

You do not need to be an indexing expert to see the problem. If three companies are driving most of the performance, you are no longer making a diversified sector bet. You are effectively making a concentrated bet on those companies, while still paying an ETF fee to do so.

If two or three companies are determining most of the ETF’s outcome, are you really still expressing a sector-wide thesis? I think this is one of those cases where the usual benefits of ETFs, diversification, and low fees start to break down.

At some point, you have to ask whether the iShares’ lineup of Canadian sector ETFs is actually worth using. Many of these funds are legacy products.

Take XEG as an example. It dates back to March 2001 and has grown to about $2.1 billion in assets under management, largely on the back of brand recognition and inertia. But in today’s market, it is difficult to justify paying 0.6% annually for a portfolio where half the exposure is concentrated in two companies.

That leads to the first option, which in this specific case is more reasonable than it usually is with broad indexing. Investors can simply buy the top holdings directly. If a sector ETF is effectively just a handful of dominant names, you can replicate that exposure yourself. With zero-commission brokerage options now widely available, building a basket of the top 10 holdings and weighting them according to your own preferences is entirely feasible.

You could choose to equal-weight them or tilt toward higher-conviction names. The trade-off is that you introduce tracking error and make the process more active. Not every investor wants that level of involvement and responsibility.

The second option is to be more selective with the ETFs you choose. One useful tool is the Cboe Canada ETF screener, which allows you to filter by asset class, geography, and sector, and then sort the results in ascending order by key metrics like expense ratio.

Source: Cboe Canada

Doing this quickly reveals that there are more cost-effective and better-constructed alternatives available. In energy, for example, you can find lower-fee equal-weighted options such as the Global X Equal Weight Canadian Oil & Gas Index ETF (NRGY).

Source: Global X Canada

The same approach applies across other sectors. In utilities, switching the screener to that category brings up alternatives like the Global X Equal Weight Canadian Utilities Index ETF (UTIL), which also comes with a lower fee profile and a more balanced allocation across holdings.

Source: Global X Canada

In short, sector investing in Canada requires scrutiny. It is not enough to have a view on a sector. You also need to understand how exposure is constructed. Otherwise, you may think you are taking a big-picture sector bet, when in reality you are paying a premium to hold a small number of stocks.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Strategy sold millions in Bitcoin. Learn why, how institutions are tackling quantum computing risks, and whether Coinbase is...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

From home office costs to travel expenses, discover the tax deductions employees may qualify for and how to claim...

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.

After learning Canada's financial system from the ground up, Chexy co-founder Liza Akhvledziani shares the money habits that helped...

The analog economy is booming, but Gen Z isn't chasing nostalgia. Here's why younger consumers are paying more for...

Cell phone related expenses may be deductible for some taxpayers, even if they were missed in the past.

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...