New active U.S. ETFs for Canadian investors—are these funds worth your money?

Notable U.S. ETF providers are expanding into Canada with new actively managed funds. Here’s what Canadian investors should know before clicking buy.

Advertisement

Notable U.S. ETF providers are expanding into Canada with new actively managed funds. Here’s what Canadian investors should know before clicking buy.

Despite U.S. President Donald Trump’s trade wars and tariffs on key partners, including Canada, the U.S. asset management industry continues to view Canadian investors as an attractive market for actively managed exchange-traded funds (ETFs).

In October 2024, Capital Group, best known for managing the American Funds lineup in the U.S., launched four actively managed ETFs in Canada, covering global equities and fixed income. That same month, JPMorgan Asset Management entered the Canadian market with two ETFs modelled after its U.S.-based equity income strategies.

JPMorgan followed up in March 2025 with another two listings on the TSX. The JPMorgan US Value Active ETF (JAVA) and the JPMorgan US Growth Active ETF (JGRO) are both variants of existing U.S. ETFs and aim to offer Canuck investors familiar strategies through Canadian listings.

As with all active funds, these ETFs face an uphill battle. The latest S&P Indices Versus Active (SPIVA) scorecard from S&P Global, which tracks how active funds perform relative to their benchmarks, shows that over the past 15 years, 89.5% of U.S. large-cap blend funds underperformed the S&P 500.

The numbers are even worse in specific equity styles. Over the same period, 95.08% of large-cap value and 95.91% of large-cap growth funds underperformed their respective S&P 500 style benchmarks.

Still, the JPMorgan brand name carries weight, and a 0.44% management fee for both JGRO and JAVA may look attractive to Canadian advisors and Canadian retail investors trying to beat the index. Here’s my take.

Both JAVA and JGRO are built on old-school active management. There’s little in the way of an algorithm or rules-based screen here. Security selection and portfolio construction are driven by the discretionary decisions of a seasoned team of portfolio managers.

According to JPMorgan, both ETFs follow what it describes as a “fundamental, bottom-up approach.” That means investment ideas are generated through deep research, conference participation and one-on-one meetings with company management teams. Rather than starting with a macroeconomic view (technical, top-down approach), these fund manager teams look at individual companies first and evaluate them on their own merit.

The selection criteria of stocks included differ depending on the ETF. For JAVA, the focus is on quality and valuation. Specifically, the managers assess the business model, financial health and management quality of the companies, alongside metrics like free cash flow and earnings.

JGRO, in contrast, is all about growth. Its managers look at the duration and magnitude of a company’s growth potential, assess its competitive dynamics and leadership, and project fundamental performance relative to market expectations.

Portfolio construction also varies. JAVA tends to be more concentrated than the average broad market ETF, generally holding between 130 and 200 stocks, split evenly between quality and value-oriented positions.

Compared to JAVA, JGRO holds a wider range of between 100 and 400 stocks, with weightings based on the managers’ conviction in each, a key feature of discretionary active management.

However, specific details about portfolio design and selection methodology are limited by design. JPMorgan doesn’t disclose every input, in part to protect its proprietary process.

The Canadian-listed versions of JAVA and JGRO are managed by the same teams as their U.S. counterparts. JAVA is overseen by a veteran team that includes Scott Blasdell, who has 31 years of industry experience (26 with JPMorgan) and has managed this fund for three years. He is joined by Andrew Brandon, with 27 years in the industry (25 at JPMorgan), David Silberman, with 36 years of experience (all at JPMorgan), and John Piccard, with 33 years in the industry and 11 at JPMorgan, who joined the fund management team less than a year ago.

JGRO, on the other hand, is managed by a duo. Giri Devulapally brings 33 years of experience, including 22 at JPMorgan, while Felise Agranoff has 21 years of industry experience, all with JPMorgan. Both portfolio managers joined the fund in the past year.

In the U.S., both funds are already well established. JGRO is the larger of the two, with just under USD$4.9 billion in assets under management. JAVA is smaller but still sizeable, with USD$3.09 billion in AUM.

It’s too early to judge the performance of the newly launched Canadian versions of JAVA and JGRO. However, their U.S.-listed counterparts have been around since October 2021, which provides a meaningful track record to draw insights from.

On the surface, JAVA and JGRO look promising. Both ETFs carry Morningstar Medalist Ratings of “Silver,” a designation awarded to funds that Morningstar analysts have “high conviction will outperform the relevant index, or most peers, over a market cycle on a risk-adjusted basis.” That’s not a bad endorsement if you trust the judgement behind it. (Gold ratings are for the top 15%, where as silver ratings are for the next 35%.)

JPMorgan also promotes the relative historical outperformance of both funds. JAVA, for instance, highlights its results versus the Morningstar large value category average and the Russell 1000 Value Index. JGRO similarly claims outperformance versus its Morningstar peer category average.

Benchmark comparisons can be carefully selected. Morningstar analyst ratings, while helpful, are still subject to authority bias. This means people may place too much trust in expert opinions even when those experts may be biased or wrong.

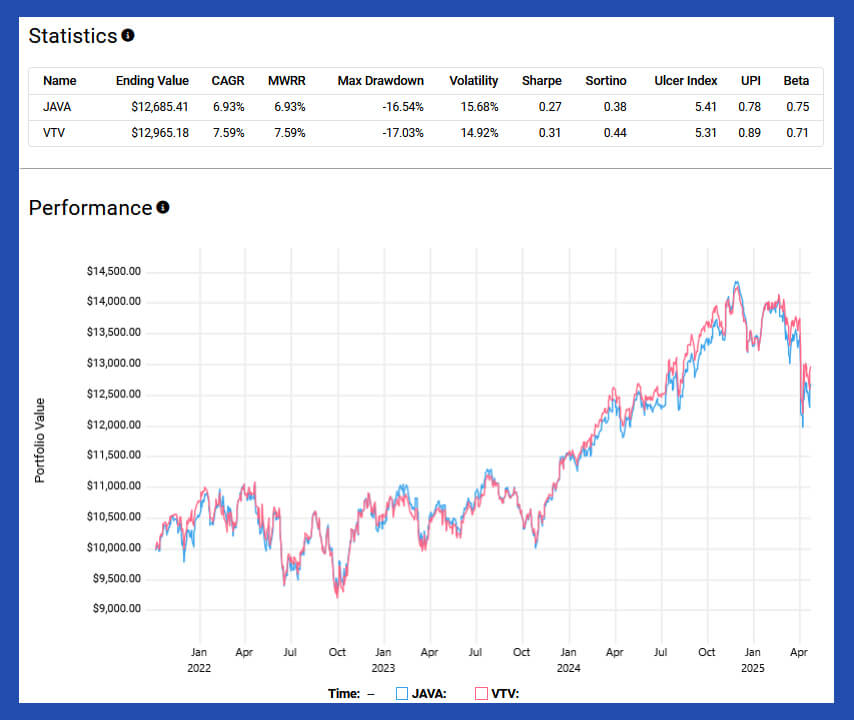

Looking at historical returns compared directly to widely available, low-cost U.S. benchmarks paints a more mixed picture. From October 5, 2021, through April 23, 2025, JAVA underperformed the popular Vanguard Value ETF (VTV), returning a 6.93% CAGR compared to VTV’s 7.59%.

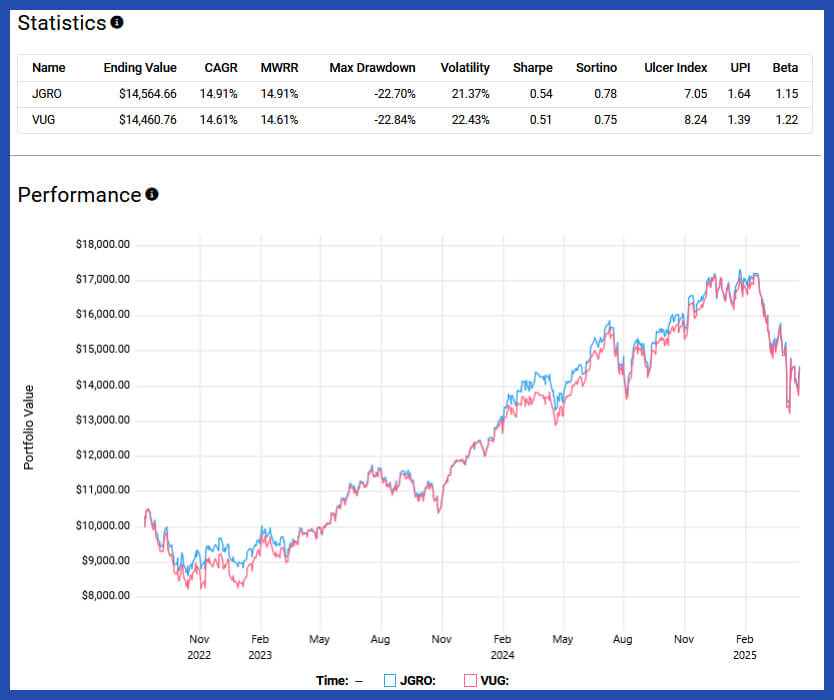

JGRO, on the other hand, only slightly outperformed the Vanguard Growth ETF (VUG) over its available window, returning 14.91% CAGR from August 9, 2022, through April 23, 2025, versus VUG’s 14.61%.

That begs the question: why pay 0.44% for JAVA or JGRO when VTV and VUG offer similar performing large-cap value and growth exposure at just 0.04%? The cost gap is significant, and it becomes even harder to justify when you examine portfolio overlap.

As of April 24, there were 99 overlapping holdings between JAVA and VTV. That represents 61.5% of JAVA’s 165 holdings, and 30.4% of VTV’s 335 holdings. This level of overlap suggests a meaningful degree of similarity between the two portfolios, at least in terms of core holdings.

For JGRO, the overlap is slightly lower but still notable. It shares 58 holdings with VUG, which amounts to 51.8% of JGRO’s 114 stocks and 35.8% of VUG’s 170. Again, this suggests that despite the active mandate, there’s significant common ground between JGRO and its index-tracking counterpart.

In my view, Canadian investors already have access to plenty of value and growth–focused index ETFs that hold many of the same stocks as JAVA and JGRO, albeit at a much lower cost. And over time, that lower fee becomes less of a headwind to performance and more of a structural advantage.

In effect, JAVA and JGRO have to overcome a 0.44% management fee year after year, while index alternatives like VTV and VUG continue compounding with a minimal 0.04% drag. That 40-basis point difference may not seem huge in the short run, but over decades, it can add up.

While the success of JAVA and JGRO’s active management teams is ultimately unpredictable, one thing we can say with near certainty is that a 0.44% annualized cost is harder to outrun than 0.04%. That’s just basic math.

Active ETFs could be a fit for Canadian advisors and retail investors aiming to outperform a benchmark. They would likely be comfortable paying higher fees in exchange for the potential of alpha. They also need to be okay with the real possibility of lagging the index—sometimes for extended periods.

Alpha refers to an investment return greater than the aggregate return of the market in which the investment trades. Actively managed funds aim to beat the market, adding alpha with the help of skillful investment decisions. In contrast, passive index funds are designed to deliver the market return only, with no alpha.

Read more in the MoneySense Glossary: What is alpha?

Above all, buying an active ETF like JAVA and JGRO means buying into the issuer. You’re not just choosing a strategy; you’re trusting a team of analysts and portfolio managers to make the right calls. It’s as much about picking the right people as it is about picking the right ETF.

That said, 0.44% is actually quite reasonable for actively managed ETFs, especially in Canada. If you’re dead set on allocating to active strategies, JAVA and JGRO just may be among the most cost-effective options available right now. Hopefully, the entrance of big names like JPMorgan will also pressure local ETF issuers to revisit their pricing models.

At the end of the day, competition is usually good, whether the ETF is homegrown or imported. Just make sure you’re looking under the hood before buying in, and don’t assume the marketing pitch tells the whole story.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Lululemon profits dip, Couche-Tard surges, and Power Corp declines. Here’s what investors need to know about Q4 results...

U.S.-Iran tensions have shaken markets, but experts urge investors to stay disciplined, avoid emotional moves, and use volatility to...

Canadian companies face a turbulent quarter, with Algoma Steel losing big and Transat posting gains amid major corporate moves.

Canadians moving to the U.S. may be able to unlock a locked-in RRSP after 24 months of non-residency—but tax...

Q4 shows mixed results across sectors: Canadian Natural and Pet Valu post gains, while George Weston and Canada Packers...

Bitcoin extends losses, down 47% since October 2025. When will the crypto bear market reverse, and what does the...