The true price of financial advice

Transparency shines a light on the value of paying for help when investing

Advertisement

Transparency shines a light on the value of paying for help when investing

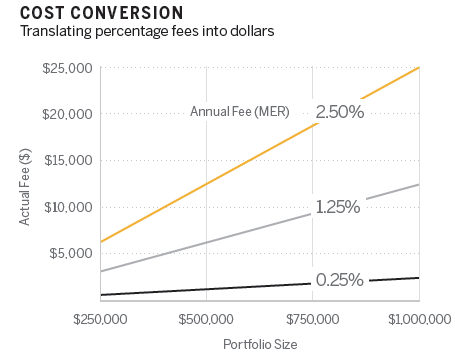

To put that in perspective, the minimum wage in Ontario will climb to $11.40 per hour this year. Sturdy retirees who are willing to work 40 hours a week for 52 weeks a year for minimum wage will make $23,713 before taxes. Alternatively, if they can slash their investment-related expenses, they might be able to save more than they’d earn, after tax.

The good news is there are several ways to cut fees, some without cutting out an advisor. Broadly speaking there are three ways to do it. You can keep the individualized advice but move to a portfolio of low-fee funds. Or you can opt to do your own planning and choose a low-fee portfolio of professionally managed funds. Finally, those with sufficient knowledge and experience can do it on their own and cut costs to the bone.

To put that in perspective, the minimum wage in Ontario will climb to $11.40 per hour this year. Sturdy retirees who are willing to work 40 hours a week for 52 weeks a year for minimum wage will make $23,713 before taxes. Alternatively, if they can slash their investment-related expenses, they might be able to save more than they’d earn, after tax.

The good news is there are several ways to cut fees, some without cutting out an advisor. Broadly speaking there are three ways to do it. You can keep the individualized advice but move to a portfolio of low-fee funds. Or you can opt to do your own planning and choose a low-fee portfolio of professionally managed funds. Finally, those with sufficient knowledge and experience can do it on their own and cut costs to the bone.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.

Cogeco reports a steep quarterly loss tied to its U.S. business, while Electrovaya jumps on an Amazon agreement and...

Why and how ETF closures happen, which warning signs to watch for, and what it means if a fund...

Nobody moves to Canada excited about price matching. When my family immigrated in 2019, I expected to spend countless...