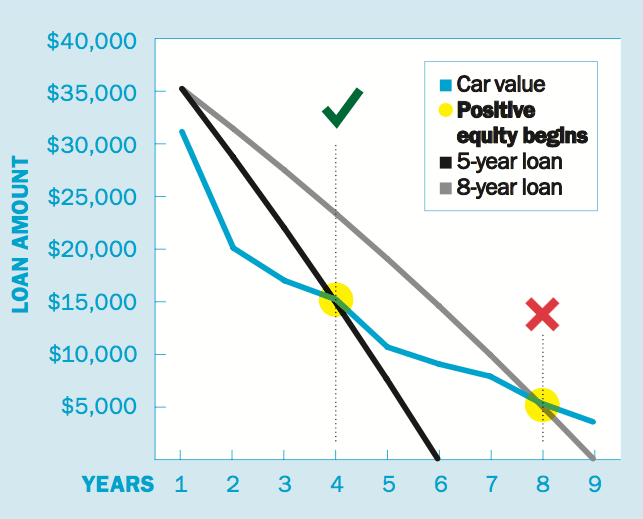

Warning: steer clear of extended auto loans

Don't fall victim to "negative equity"

Advertisement

Don't fall victim to "negative equity"

Read more:

Should I get a long-term loan? »

How to get out of a bad car loan »

Buying your first car »

Read more:

Should I get a long-term loan? »

How to get out of a bad car loan »

Buying your first car »

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Travel scams are rising with AI, from fake booking sites and rentals to phishing emails and stolen loyalty points....

Thinking of ditching your car? Experts break down the real costs, savings, and trade-offs of life without a vehicle...

Airlines are raising fares, adding fees and cutting flights as fuel costs surge. Expect fewer deals and higher prices...

Ticket prices can swing wildly with dynamic pricing. Here’s when to buy early, when to wait, and how to...

Rising fuel prices and geopolitical tensions are pushing Canadians to rethink when and how they book travel, with many...

Summer travel doesn’t have to break the bank. Here’s how to save with strategic timing, flexibility, and smarter booking.

Home exchanges are changing how we travel, making it more affordable, flexible, and personal. Here’s how platforms like HomeExchange...

Global airlines, including Air Canada and WestJet, are raising fares and fuel surcharges as jet fuel prices soar following...

Used car prices remain high in 2026, pushing buyers to put down less and finance more. Here’s how insurance...

A pricing error could work in your favour. Discover how Canada’s Scanner Price Accuracy Code compensates shoppers—and its important...