Where to invest $500,000

More money gets you more options, and some come at a lower cost

More money gets you more options, and some come at a lower cost

Once your nest egg reaches $500,000, you have a lot riding on investing it wisely. Fortunately, more money gets you more options, and some come at a lower cost.

If what you’ve been doing so far is working, you don’t have to change, but I’ll present you with three choices you can access at $500,000 that aren’t usually practical for those with smaller portfolios. Two of them involve specific types of investment professionals: full-service brokers and investment counsel firms. For the third option, we consider investing outside the traditional stock and bond portfolio in an income property.

If you want to turn over day-to-day management of your money to seasoned professionals, your best option if you have at least $500,000 may be an investment counsel firm (also known as a “portfolio management firm” or “private investment counsel”). These money managers make the day-to-day investment decisions subject to your overall direction, which is known as “discretionary” portfolio management.

If you want to turn over day-to-day management of your money to seasoned professionals, your best option if you have at least $500,000 may be an investment counsel firm (also known as a “portfolio management firm” or “private investment counsel”). These money managers make the day-to-day investment decisions subject to your overall direction, which is known as “discretionary” portfolio management.

While their specific investment philosophies vary, they generally emphasize prudence. “The culture is this is a stay-rich portfolio, not a get-rich portfolio,” says Kelly Rodgers, president of Rodgers Investment Consulting. The main downside? You need a lot of money to access this option. Only some firms will take you as a client if you have $500,000 to invest—many require that you have $1 million or more.

Investment counsel firms are known for rigorous investment processes provided by a team of exceptionally well-qualified professionals. Typically you meet with an account representative holding the well-regarded chartered financial analyst (CFA) designation. Compared to most financial professionals “they have far more in-depth training in portfolio analysis and portfolio construction,” says Rodgers. That person thoroughly examines your financial situation, needs and risk tolerance, and then helps set your asset allocation, all of which is documented in an Investment Policy Statement (IPS). The money is then turned over to investment professionals working in the background who invest the money according to the direction in the IPS.

Fees are typically 1% to 1.5%, roughly comparable to rates charged by full-service brokers for stock and bond portfolios of a similar size, but cheaper than what you will pay for mutual funds through an adviser.

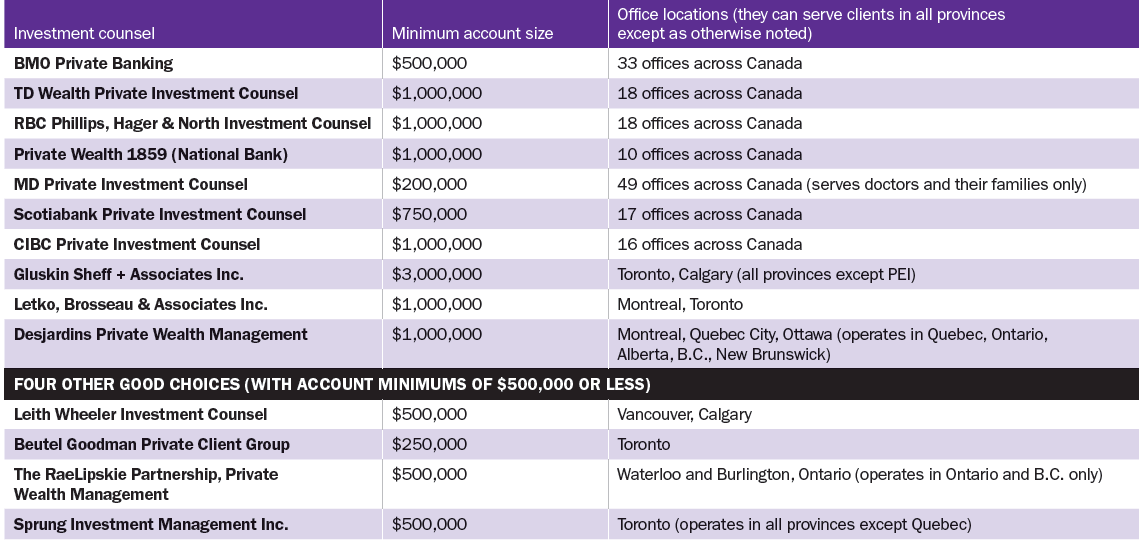

Despite their investment prowess, these low-key firms aren’t well-known. While many of the largest firms are divisions of banks, their services are rarely described in ads. For a list of leading investment counsel firms, see the tables below. You can also find a more extensive listing of firms at the Portfolio Management Association of Canada website, portfoliomanagement.org.

Brokers can be a good option if you invest mainly in stocks, bonds and ETFs, and you’re looking for advice. Few brokers are interested in your business if you only have $100,000 to invest, but most are keen to serve you when you have $500,000 or more. While at one time brokers were known for touting hot stock tips, these days they’re usually called “investment advisers” and are likely to take a broader view to managing your overall wealth. Often they can draw on financial planners and other experts from their firms to provide specialized advice.

Compared to mutual fund advisers, brokers are licensed to sell more products and can often do it for lower fees. A broker with a basic license can sell stocks, bonds, ETFs, and mutual funds, whereas mutual fund advisers with a basic license can only sell mutual funds. At $500,000, you can expect to pay somewhere around 1.5% or a bit less. You may need to invest $1 million or more to bring fees down to 1%. Many brokers also provide the traditional option of being paid through a commission on each trade. In contrast, you’ll generally pay about 2% per year for a balanced stock and bond mutual fund portfolio purchased through a mutual fund adviser.

Brokers have a lot of independence to operate their own practice within the overall brokerage firm. Minimum license requirements ensure only basic knowledge of investments, so knowledge levels vary widely. If you’re looking for a broker, it’s important to find one with a strong combination of qualifications and experience who follows an approach that fits your needs.

Consider the approach used by Craig Allain, an investment adviser with RBC Wealth Management in Waterloo, Ont. He has been a broker for more than 20 years and has a $500,000 account minimum. His designations include Certified Financial Planner (CFP) and Chartered Investment Manager (CIM) and he has an additional license to sell insurance. He manages some accounts on a “non-discretionary” basis (he advises, you make the decisions). But he also has an additional license to manage accounts on a “discretionary” basis when authorized by clients to do so (in that case, he makes the day-to-day decisions subject to your overall direction).

Before Allain invests any money for a new client, he typically has an RBC financial planner prepare a complete financial plan to help him thoroughly understand the client’s situation, needs and objectives. He also asks probing questions about risk tolerance. He looks at the overall picture and often provides advice about things such as life insurance and wills. “We definitely follow the wealth management approach,” says Allain. “Money management is part of it, but there’s so much more to it than that.”

An effective broker typically adopts a specific investment approach that draws heavily on the firm’s expert research and then sticks with it. In Allain’s case, when it comes to equities, he specializes in recommending blue-chip dividend stocks drawn from the research department’s “focus lists.” This approach tends to result in similar holdings across his 206 household accounts, which allows him to effectively monitor and then quickly adjust each account according to new developments.

Another option that makes sense for those with $500,000 or more is income properties. While they’re not for everyone and they can come with significant risks, you may be able to find higher yields than you can get with stocks and bonds.

Another option that makes sense for those with $500,000 or more is income properties. While they’re not for everyone and they can come with significant risks, you may be able to find higher yields than you can get with stocks and bonds.

The key is selectivity. You won’t get decent yields buying condos in Vancouver and Toronto, says Don Campbell, senior analyst and co-founder of the Real Estate Investment Network (REIN). Instead look for townhomes, semis, and multiplexes in small or medium-sized cities with strong income and population growth in centres like Barrie or Hamilton in Ontario; Maple Ridge or Abbotsford in B.C; Saskatoon, Saskatchewan; and Airdrie or Fort Saskatchewan in Alberta, he says.

In my view, prudent investors are best off considering an income property only after they’ve paid off the mortgage on their residence, and then should invest only part of their nest egg. Campbell says putting a third of your investable assets into real estate would be reasonable for many people. He adds that you can find good options in real estate if you start with an initial investment of $150,000 or $200,000. That can provide you with a 25% down payment on a property worth $600,000 to $800,000, with the rest covered by a mortgage.

If you search carefully, you should still be able to find a property which generates a “cash-on-cash” return of 7% or 8%, he says. The cash-on-cash return is the net annual cash flow from the property, net of all costs, including maintenance and mortgage payments, as a percentage of the down payment. While that’s significantly less than you could earn a few years ago when real estate was cheaper, it is much better than yields for reasonably conservative stock and bond investments.

Direct real estate investing won’t suit everyone. You need to be savvy and do your homework thoroughly. Campbell says it’s important to make sure that the property will make money for you based on net rental income alone: “Don’t count on capital appreciation.”

Maintenance costs, such as replacing the roof or furnace, tend to be higher than you’d think, and you always run the risk of having your cash flow disrupted by a problem tenant. You can also run into trouble if you take out a big mortgage and interest rates start to rise. For that reason, it’s a good idea to lock in your mortgage for five to seven years and assess what your payments would be if rates rose by a couple of percentage points at renewal. A good conservative strategy is to plan to pay off the rental mortgage entirely by the time you retire.

Full service brokers—who typically go by the title of “investment adviser” these days—are a good choice for investing in stocks, bonds, and ETFs if you need advice and want to approve every investment decision. Brokers have a lot of independence to adopt their own approach within the overall brokerage firm. You should interview two or three before making a decision.

Investment counsel firms (also known as portfolio management firms) are a good choice if you want to leave the day-to-day choices of what to buy and sell up to professionals, subject to your overall direction. Investment counselors typically adopt an integrated and rigorous team approach to manage your money. We start with a list of the largest firms. We supplemented that with a list of several reputable firms with a minimum account size of $500,000 or less. Note that many firms are flexible on minimum account size if they expect you to add more money over time.

Notes: The largest firms are ranked by assets under management, by order of size. One additional firm had sufficient assets to be included in the top 10 but asked not to be identified. Source of largest firms by assets is: Investor Economics, Winter 2015. Minimum account size and office locations were provided by each firm.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Sponsored By

National Bank of Canada

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

This prepaid travel card eliminates foreign exchange charges on your purchases abroad, though the loading fees could irk some...

Food and beverage company expects organic growth of 4% in 2024.

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.