Can this couple retire early?

Bao Lam, 43, wants to retire comfortably at age 65. If he sells his business and switches to a less stressful but lower-paying job, can he do it?

Bao Lam, 43, wants to retire comfortably at age 65. If he sells his business and switches to a less stressful but lower-paying job, can he do it?

Bao Lam, a 43-year-old certified financial planner in Waterloo, Ont., believes in second opinions. He asked MoneySense for our thoughts on whether he’s on track to leave his high-paying—but stressful—job at age 47. That’s when he hopes to sell his business for $900,000 and invest that money until his retirement at 65. Bao’s 39-year-old wife Jeannette, who is currently his assistant, would stop working. “Doctors need a second opinion about their own health,” says Lam. “It’s no different with financial advisers.”

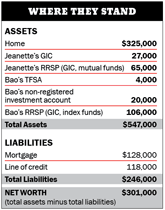

The Lams, who have a teenage son, have assets including a $325,000 home and $222,000 in registered and non-registered investments. They will be cashing in Jeannette’s $27,000 GIC and putting it towards their $118,000 line of credit later this year. The couple, who gross $180,000 per year, hope to have all their debts (including a $128,000 mortgage), paid off before retiring.

The Lams, who have a teenage son, have assets including a $325,000 home and $222,000 in registered and non-registered investments. They will be cashing in Jeannette’s $27,000 GIC and putting it towards their $118,000 line of credit later this year. The couple, who gross $180,000 per year, hope to have all their debts (including a $128,000 mortgage), paid off before retiring.

When they sell their business, the Lams will receive $90,000 gross per year for 10 years, with payments made monthly. “If I invest that money and don’t touch it until age 65, will that be enough to guarantee us a comfortable retirement?” asks Bao. “I plan to work at a salary job making $60,000 gross or so from age 47 until age 65—just enough to live on comfortably without saving a penny more. I’m not counting on CPP or OAS so the funds will have to come completely from my portfolio.”

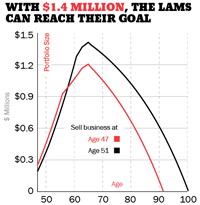

According to Heather Franklin, a fee-only adviser in Toronto, the Lams won’t be able to meet their targets. Selling Bao’s business sounds appealing, but the entire $900,000 won’t be available for investment until Bao is 57. At an annualized growth rate of 5%, the Lams should have $1.2 million at age 65. That sounds like a lot, but since the Lams aren’t counting on CPP and OAS—a pessimistic viewpoint, given that CPP is well funded—it’s not enough. Franklin says Bao should stay at his current job until 51 so he can save another $200,000 before he sells his business. “This will let him bulk up his savings and cushion him against any setbacks in his investments,” she says. “With all of us living longer and longer, he needs a minimum $1.4 million at 65 to ensure the portfolio takes him and his wife to age 95.”

According to Heather Franklin, a fee-only adviser in Toronto, the Lams won’t be able to meet their targets. Selling Bao’s business sounds appealing, but the entire $900,000 won’t be available for investment until Bao is 57. At an annualized growth rate of 5%, the Lams should have $1.2 million at age 65. That sounds like a lot, but since the Lams aren’t counting on CPP and OAS—a pessimistic viewpoint, given that CPP is well funded—it’s not enough. Franklin says Bao should stay at his current job until 51 so he can save another $200,000 before he sells his business. “This will let him bulk up his savings and cushion him against any setbacks in his investments,” she says. “With all of us living longer and longer, he needs a minimum $1.4 million at 65 to ensure the portfolio takes him and his wife to age 95.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Presented By

Embark Student Corp.

Breaking your mortgage to get a better interest rate could save you thousands of dollars. Here’s what you should...

Has your home insurance premium gone up? We get to the bottom of why rates are on the rise...

You've poured lots of money into your RRSP. How do you get it out without paying a fortune in...

Thinking about a career change or worried you won’t escape the next round of layoffs? Follow our tips to...

You can do more than survive in Canada—choose where to put your wisely and over the long term you'll...