Being hooked on debt has long-term consequences

There's a cost that goes beyond low interest rates you see posted online

Advertisement

There's a cost that goes beyond low interest rates you see posted online

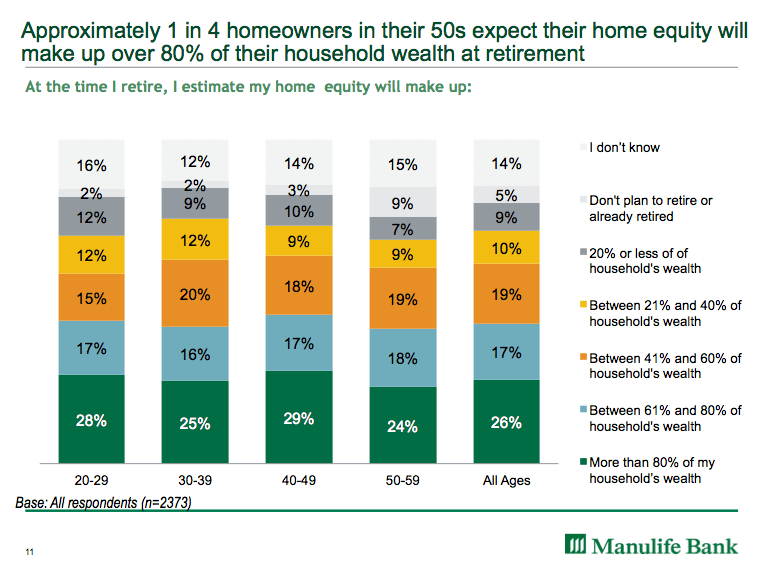

“Our research has consistently found that becoming debt-free is among the top financial priorities for Canadian homeowners, says Lunny. But with stretched budgets and rising housing costs, these homeowners must find a balance between debt repayment and saving for retirement. “So they don’t end up house-rich and asset poor,” says Lunny.

Why? Because increased debt means some potentially difficult decisions, says Lunny. Those with significant equity in their home and insufficient retirement funds could opt to: retire later than originally planned, accept a lower standard of living in retirement, downsize to a less expensive home, or borrow against their home equity to pay bills and fund their retirement.

“Our research has consistently found that becoming debt-free is among the top financial priorities for Canadian homeowners, says Lunny. But with stretched budgets and rising housing costs, these homeowners must find a balance between debt repayment and saving for retirement. “So they don’t end up house-rich and asset poor,” says Lunny.

Why? Because increased debt means some potentially difficult decisions, says Lunny. Those with significant equity in their home and insufficient retirement funds could opt to: retire later than originally planned, accept a lower standard of living in retirement, downsize to a less expensive home, or borrow against their home equity to pay bills and fund their retirement.

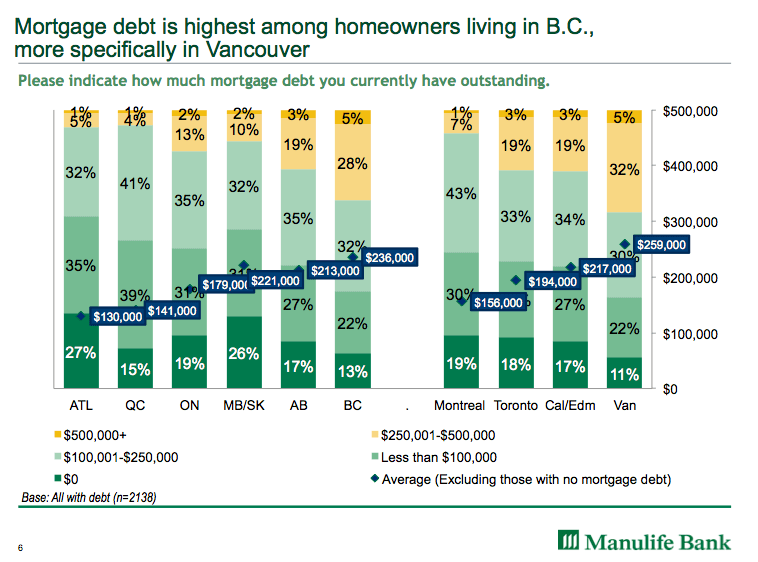

“When you look at why people struggle to make a mortgage payment it almost always comes down to income. It could be a loss of a job, a pregnancy leave, a temporary disability or illness, but whatever the reason, people need to develop a budget and a spending plan that enables them to plan for periods with a reduced income,” says Lunny.

“The best option is to work with an advisor to get a plan in place well before retirement to balance debt repayment, retirement savings and day-to-day spending,” says Lunny.

Why you should cash out your emergency fund »

Why you may not need an emergency fund »

How much will you need to retire? »

Read more from Romana King at Home Owner on Facebook »

“When you look at why people struggle to make a mortgage payment it almost always comes down to income. It could be a loss of a job, a pregnancy leave, a temporary disability or illness, but whatever the reason, people need to develop a budget and a spending plan that enables them to plan for periods with a reduced income,” says Lunny.

“The best option is to work with an advisor to get a plan in place well before retirement to balance debt repayment, retirement savings and day-to-day spending,” says Lunny.

Why you should cash out your emergency fund »

Why you may not need an emergency fund »

How much will you need to retire? »

Read more from Romana King at Home Owner on Facebook »

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Tax season can push Canadians deeper into debt as many rely on refunds. Here’s why it’s happening, and how...

The first quarter finally broke the pattern of steadily rising markets, but energy stocks soared.

Robert has been taking RRIF withdrawals beyond the minimum required amount to gift to his kids and to reinvest...

Geopolitics, rising oil prices and ETF inflows are shaping Bitcoin’s outlook. Is now the right time for Canadian investors...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

A University of Calgary study found that over one-third of senior homeowners worry about affording basic home maintenance, suggesting...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Whether you want the highest interest rate or no service fees, these savings accounts will meet your needs.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...