What are covered call ETFs, and are they good investments?

Covered call ETFs aren’t for everyone. Here are some common misconceptions about this investment type, and who it’s best suited for.

Advertisement

Covered call ETFs aren’t for everyone. Here are some common misconceptions about this investment type, and who it’s best suited for.

Covered call exchange-traded funds (ETFs) have seen an influx of attention recently from Canadians seeking a high-yielding investment, according to Travis Koivula, investment advisor at Aviso Wealth in Victoria. As retail investors take the reins on managing their own investment accounts, many are looking for high-yielding securities like covered call ETFs, due to the income distributions they offer, he says. But Canadian investors should know about the downsides of investing in covered call ETFs.

A call option is an agreement that gives a buyer the right to buy a stock at a predetermined price in the future. The seller is compensated for giving the call option buyer the right (or the option) to buy the investment they own. The option is “covered” if the seller owns the underlying stock. Canadian investors can “write” (sell) a covered call option when they want to reduce the risk of owning an investment.

In 1999, Mark Cuban (the minority owner of the Dallas Mavericks but better known as a panellist on Shark Tank) sold Broadcast.com to Yahoo!, and in return received 14.6 million shares of the company. Cuban was forced to hold Yahoo’s shares (likely due to a lock-in period) and implemented a version of covered calls to protect his position, explains Koivula.

In the example above, Mark Cuban can give another investor the right to purchase one share of Yahoo—let’s say at $100 per share—at a future date. For simplicity’s sake, we’ll assume Cuban’s Yahoo shares are worth $95 each, so he was able to sell the option for, say, $4. Here are two hypothetical outcomes:

You can see that the covered call acts as a kind of dampener on the investor’s overall return, while giving them immediate income ($4 in the example above).

Most Canadian investors don’t implement options trades. But they can own covered call ETFs. Covered call ETF providers step in to implement this trade on investors’ behalf, with a larger pool of funds. Global X’s S&P 500 Covered Call ETF (XYLD) is a well-known example of a covered call ETF. In Canada, examples include RBC’s Canadian Dividend Covered Call ETF (RCDC) and CI’s Gold+ Giants Covered Call ETF (CGXF). Use a Canadian ETF screener to find more.

Many Canadian retail investors are seeking the highest dividend or yield that they can find in an ETF. In many cases, covered call ETFs come up near the top of that search, says Koivula.

Some of his own clients see covered call ETFs offering eye-popping yields, and they decide to further investigate the opportunity. Indeed, as of Feb 14, 2024, XYLD paid a 10.6% 12-month trailing yield, which, on face value, is a very strong income yield.

ETFs like this can work well in the short-run. Koivula points out that clients like that they’re “getting paid to wait” if they think markets will be flat or down.

It’s true that covered call ETFs pay a high income yield. But there’s a number of reasons why they may not be the ideal investment outside of a few situations.

The first thing to know is that distribution yield does not equal investment return.

By their nature, covered calls cannot deliver better returns in a market that continues to increase. Over the long run, stocks go up, even though they may go down or sideways for periods of time. Covered call strategies involve selling the upside gain on an underlying security. Thus, if the security keeps going up—you’re losing out on gains.

Even if you receive a high-income yield, you will end up forgoing capital gains to keep the strategy going.

In the Cuban example, if Yahoo’s shares went up to $150, he would miss out on a $55 gain while only receiving a $4 premium. This $4 premium looks like a 4.2% yield ($4 income divided by the initial $95 stock price). However if Cuban wanted to keep this strategy going he would have to repurchase the stock again at $150, thus realizing $51 of lost appreciation. Here’s what the calculation looks like:

$95 initial share + $4 income – $150 to reset the position = -$51

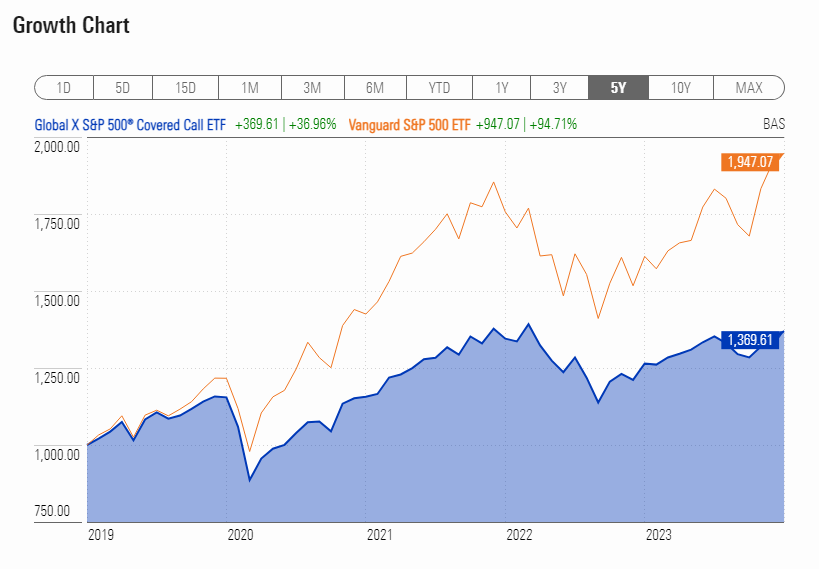

The underperformance is shown in the example below. XLYD, which performs a covered call strategy on the S&P 500, starkly underperforms Vanguard’s S&P 500 ETF (VOO) by more than 50% in the past five years. This gap gets wider as you look on a longer time horizon.

XYLD vs. VOO five-year performance (as of Feb 15, 2024). Source: Morningstar

Most ETFs you can find that track a vanilla index are passively managed, such as the iShares Core S&P 500 ETF. This means that the ETF will do its best to match the securities of a given index, and will not veer outside the lines paved by the index.

Covered call ETFs, on the other hand, are generally actively managed. To implement the strategy takes careful planning and meticulous trade execution beyond a simple buy-and-hold strategy. Thus, covered call ETFs charge more for the service of implementing the strategy.

VOO charges a measly 0.03% expense ratio; meanwhile, XYLD charges a 0.60% expense ratio (20 times more). These expenses add up over time and eat into investment returns, especially in the long-run.

A common misconception amongst Canadians investors is that covered call ETFs provide dividend income, says Koivula.

When you buy an ETF and hold it, the appreciation is tax deferred until you sell it. But the cash distributions of covered call ETFs generally include a mix of dividends, capital gains and tax-free return of capital. The option premium income is taxable as a capital gain as it is earned.

With covered call ETFs, there may also be more turnover of the underlying holdings as call options are exercised and stocks within the ETF are sold. Ultimately, this may be less tax efficient than a buy-and-hold approach, as capital gains are continuously triggered.

At a minimum, Canadian investors should understand the investing strategy they are using, including the risk/reward profile of their investments, says Koivula.

Covered call ETFs are best used over short periods by active and sophisticated investors wanting to get paid to wait in a flat market. Although they are commonly held in non-registered accounts, their tax structure means it may be better to keep them in tax-advantaged accounts, such as a registered retirement savings plan (RRSP), tax-free savings account (TFSA) or first-home savings account (FHSA).

“Covered calls are a great way to earn income in a flat market or down market,” says Koivula. “But for a long term investor, I believe owning the underlying index is a more profitable strategy.”

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Copper production lifted First Quantum, while Intact faced higher catastrophe claims. Catch up on the latest quarterly results from...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Whether a U.S.-listed ETF is worth buying depends on foreign exchange costs, taxes, MERs, and your investment account.

Artificial intelligence is transforming markets, but retirees should approach the AI investing theme with caution and a well-diversified portfolio.

Cogeco reports a steep quarterly loss tied to its U.S. business, while Electrovaya jumps on an Amazon agreement and...