How to pay for your kids’ education

Achille and Heidi Correggia of Brantford, Ont. want to pay tuition for all their three kids. Are they saving enough?

Achille and Heidi Correggia of Brantford, Ont. want to pay tuition for all their three kids. Are they saving enough?

Achille and Heidi Correggia of Brantford, Ont., have three children—Kyle, 6, and three-year old twins Sophia and Noah. The couple has been contributing $2,500 annually per child into a family plan RESP starting the year each was born. ($2,500 is the maximum annual RESP contribution per child that is eligible for a 20% government grant.) “We want to be able to pay the full cost for all of their university educations, no matter where they choose to go,” says 38-year-old marketing specialist Achille. His wife shares that goal. “Both our parents paid for much of our educations,” says Heidi, a 37-year-old physiotherapist. “We want to do the same.”

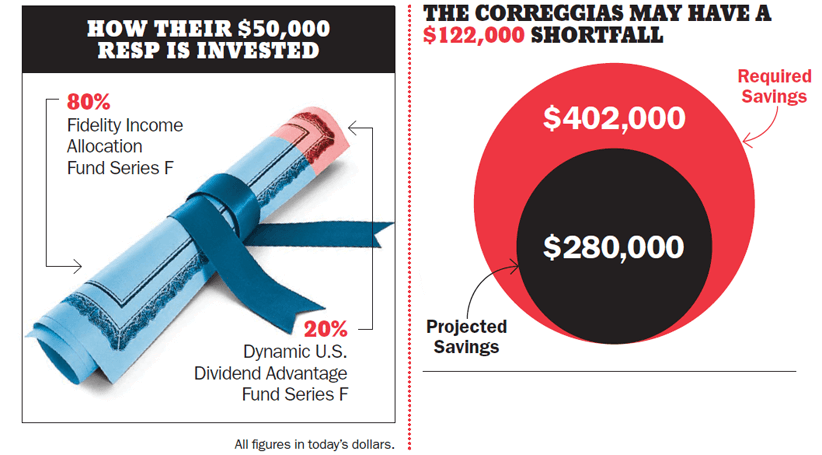

However, the couple worries rising tuition rates may thwart their efforts. “If we keep saving $2,500 per child until each turns 17, will we have enough to fully fund their educations?” asks Achille. Their RESP now totals $50,000, invested 20% in the Dynamic U.S. Dividend Advantage Series F equity fund and 80% in the bond-oriented Fidelity Income Allocation Fund Series F. The couple assumes a 3% annual increase in post-secondary education fees.

According to Annie Kvick of Money Coaches Canada, the Correggias may not fully meet their goal without some tweaks. A four-year university degree costs $62,000 today. Last year, the cost of undergraduate programs soared 5%. “So the Correggias should save more,” says Kvick. Assuming a 3% annual increase in post- secondary costs (and a 4.5% return) they’ll need $300,000 in RESPs to fully finance their goal. The shortfall would be only $20,000.

But if university costs rise 5% a year—more likely—they’ll need $402,000 to fully pay for their kids’ education. So they should save an extra $6,200 a year until the twins are 17. Much of this can be met with RESPs ($50,000 is the maximum room per child), with the rest saved in the parents’ TFSAs or non-registered accounts in-trust for the kids. “The asset mix of 58% fixed income and 42% equity is appropriate for their time horizon and adequate to meet their goals with the higher contributions suggested here,” says Kvick.

Of course, they could be more aggressive with their investments, and the kids could chip in by winning scholarships or taking part-time jobs.

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

It’s challenging to balance education savings with the high cost of living. Here are six ways to invest in an...

We have everything you need to know about tax credits, changes and deadlines, and more. Get the info you...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

Here’s how to get your free ticket to attend the MoneyShow Canada Virtual Expo.

Trump sells unprofitable company for billions, the U.S. is an oil king, GameStop struggles continue, and tech rules the...

Inflation falls, Fedex jumps 13%, earnings soften for Power Corp and Couche-Tard, and S&P 500 gets two new members.

Oracle shares up 13%, Reddit’s unique IPO, Canadians are gloomier than most on world economic prospects, and Japan’s stock...