Get the benefit from investing momentum, with less risk

Use moving averages to mitigate downdrafts

Use moving averages to mitigate downdrafts

Last summer I wrote about the potential strength in performance from momentum strategies over the long term. The simple strategy I back-tested performed splendidly, beating the S&P/TSX composite index by 13.3% annually.

However, while it seems that using momentum stocks can produce outstanding returns, they also come with increased volatility. The same strategy I back-tested, produced a much greater downside deviation (a measure of the volatility of negative returns) than the index. This means that the strategy produced more frequent and larger negative returns than the benchmark. The strategy also produced a large drawdown, losing 36.9% during the financial crisis in 2008.

Experiencing this type of portfolio loss in such a short time period is rather painful for most investors. This potential distress alone can prevent investors, or at least detract them, from following a momentum strategy or even general stock investing. However, there are options that attempt to control or at least mitigate these risks. One of those options is following a crossover rule using a simple moving average.

There are different types of crossover rules with moving averages. A simple type is when the price of an asset moves above or below its moving average. When the price moves above the moving average line or “crosses over”, that signals an uptrend. On the other hand, when the price moves below its moving average line, that would signal a downtrend. Crossover rules removes emotion from trading as they are strict in dictating when you buy and sell.

For this exercise, we are going to implement this simple crossover rule using the S&P/TSX composite index price. If the index’s price moves above 1% of its moving average, then you would buy (or stay invested in equities). If the price moves 1% below its moving average, sell your stocks (or stay in cash). Our cushion of 1% prevents increased buying and selling when the index price moves above and below its moving average lines frequently. We will implement this rule on the same strategy used in the momentum article. As a reminder, the strategy focused around short term price increases with a restriction of stocks having at least a market cap of $250 million to exclude the smaller cap stocks. There was also a return on equity factor which added positive performance when combined with price momentum.

These are factors used:

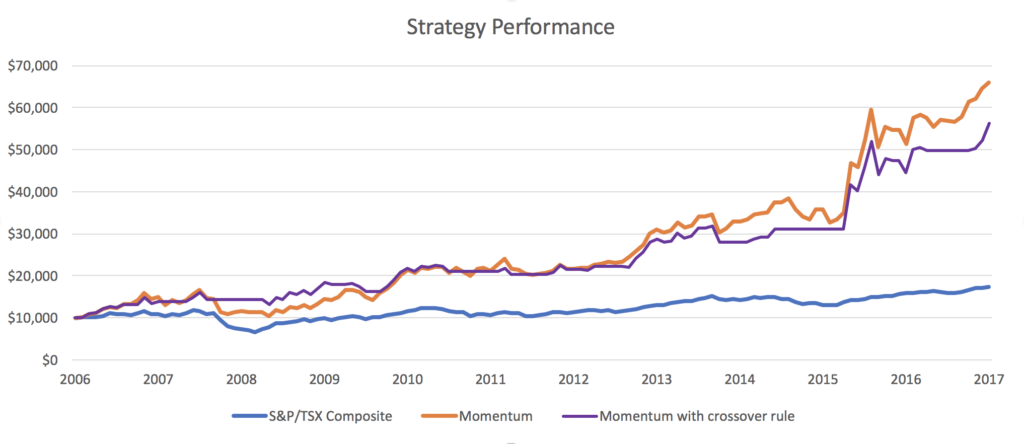

I ran an updated back-test from December 2006 to December 2017, using an initial investment of $50,000. During this process, a maximum of 15 stocks were purchased and equally weighted. Quarterly, the portfolio would be replaced with the best 15 stocks based on the strategy’s criteria. Trading costs were $9.99 per transaction.

The strategy produced an annualized total return of 18.7% over the period while the S&P/TSX composite index advanced 5.1%, resulting in an outperformance of 13.6%. Downside deviation was 13.3% and the maximum drawdown was -36.7%.

Adding the crossover rule lowered the annualized total return to 17%. However, downside deviation was reduced to 9.5%, nearly matching the index’s 9.4% during the same period. Maximum drawdown contracted significantly to -18.6%. In other words, downside risk was substantially reduced at a minimal cost of total return.

| Annualized Return | Downside Deviation | Maximum Drawdown | |

| Momentum Strategy | 18.7% | 13.6% | -36.7% |

| Momentum Strategy + Crossover Rule | 17.0% | 9.5% | -18.6% |

Crossover rules may mitigate some unwanted volatility, but they do not help with the high turnover that comes with momentum strategies. In fact, crossover rules may increase turnover. Also, these rules are meant to be predictive but can (and will) fail at times. Following them may have your portfolio in cash when the market is thriving, and other times may be late signaling a downtrend. Also, crossover rules are meant to be followed in a strict manner. You should buy or sell according to the rules you implement at all times, as opposed to when you feel like it.

Even if they are not perfect, crossover rules can be a powerful tool to mitigate risk of significant portfolio losses. There are many types of crossover rules to choose from. Before implementing one, make sure you do your own research to understand how to use them and their implications.

MORE ABOUT INVESTING:

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Food and beverage company expects organic growth of 4% in 2024

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Managing lifestyle creep is challenging financially and psychologically, especially with inflation. Expert strategies keep day-to-day spending in check.

Bitcoin’s next “halving” is right around the corner. Here’s what you need to know.