Downsizing: Go small, think big

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

Downsizing in retirement can add a sizeable chunk of income to your nest egg, paving the way for more security and enjoyment in your golden years

It was a little over a year ago that Bob and Helene Murray sat in the family room of their suburban Toronto home, discussing when and how they could finally start realizing their retirement dream of moving back to their native Montreal. Job opportunities had spurred the 50-something couple to leave decades ago, but in their advancing years they now felt the tug of wanting to be closer to family and the city where they both grew up. While health issues had recently forced Bob to pack in his career, Helene wasn’t sure if she could join him quite just yet—financially, they didn’t know if their nest egg was big enough. (We’ve changed names to protect their privacy.)

That’s when the Murrays wondered whether downsizing and tapping some of the equity in their paid-for home might help make up the difference and allow them to kick-start their plans sooner. “Basically the question was, could we swing it? Would we have enough money if we budgeted properly,” asks Bob. “Because if we couldn’t swing it, Helene would stay at work. But she really wanted to retire—that added fuel to the fire.”

Leaving the family home is one of the most complicated issues couples will face in retirement. The best downsizing plans must satisfy a range of needs: finances, lifestyle, being close (or not so close) to family and friends, not to mention the practical realities of aging. Some people feel no tie to the family home and want to downsize and relocate as soon as they retire, while others are determined to stay put until they’re carried out feet first. In the end, the right decision for you will be highly individual based on your particular needs and circumstances—but there are a number of common factors you should consider. Read on to see how you can make downsizing work to your advantage.

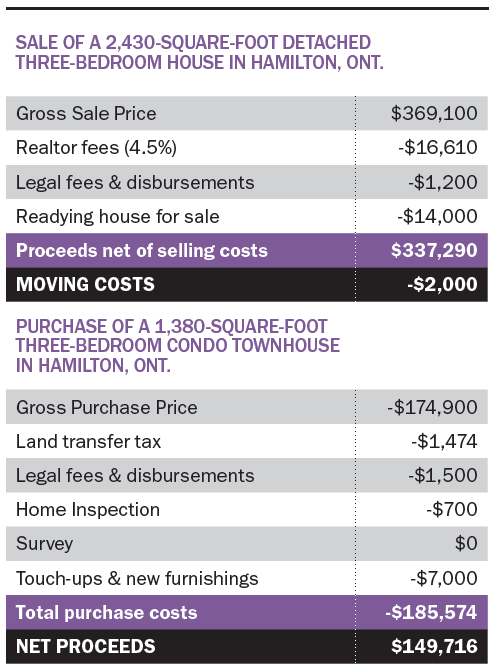

Notes: Prepared with the assistance of Melanie Reuter, Elizabeth Campbell and Don Campbell of the Real Estate Investment Network. Gross sale price, gross purchase price and land transfer tax are taken from actual recent real estate transactions in Hamilton, Ont. (In this case, the seller of the house and buyer of the townhouse are not the same.) The other figures are estimates. Realtor fees can vary from 2.5% to 6%. Money spent on readying house for sale as well as touch-ups and new furnishings will vary widely. Buyer is often required to commission a survey by the mortgage lender if the seller can’t produce one done fairly recently. In this case we’ve assumed no new survey is required. Land transfer taxes vary widely across Canada but most provinces have them. Purchase of a newly constructed home would be subject to additional costs, particularly GST. In this case, both properties are resales and not subject to GST.

There are two natural times to consider downsizing—near the start of retirement or much later on. But shortly into your post-working years, you’ll probably find you don’t require as large a home anymore. “You no longer need to be near work and schools,” points out Steven Sass, associate director of the Boston College Center for Retirement Research. And the key advantages to downsizing immediately are many: it may help you reinvent your lifestyle, live in a locale where you please, and maybe make use of some—but ideally not all—of the equity in your home to help afford a better retirement lifestyle. If you are looking to bolster your finances by downsizing to a less expensive property, be mindful that it’s generally smart to retain some home equity in case it’s needed later on.

Of course, if you don’t own an expensive home in Toronto or Vancouver, you probably won’t net an enormous payoff, especially after considering transaction costs. But often a smaller payoff can still be well worth it. In many communities, you should be able to sell a typical three-bedroom family home, buy a smaller townhouse or condo apartment in the same general area, and net at least $100,000 to $200,000. Above—in “How much can you net from downsizing your home?”—I provide an example of a strategy that yielded $150,000. As a rule of thumb, adding that amount to your nest egg would allow you to withdraw a further $6,000 a year plus inflation adjustments starting at age 65 (based on a 4% initial withdrawal rate). While that’s far short of being enough to retire on by itself, it can make a big difference topping up finances to afford a few more retirement comforts.

If you’re downsizing later in retirement, the decision will probably be more strongly influenced by growing frailties. There are a lot of things you can do to help you stay in the family home—see “Aging in place” on pg. 21 for tips on how to enjoy your home longer—but keep in mind there often comes a point where it no longer makes sense. As the effects of aging become pronounced, it typically becomes difficult to get everything you need cost-effectively in a family home setting. “If you’re stuck in there, and you’re not eating well and you’re forgetting to take your medication, a retirement residence that provides structure, socialization, activities, and nursing attention can for many enhance their well-being,” says Audrey Miller, a geriatric care manager who is managing director of Elder Caring Inc.

If you’ve retained a sizeable chunk of your home equity, you might be able to use the proceeds of selling the family home to help afford the often substantial costs of a retirement home (for seniors who need a little help with activities of daily living) or a nursing home (called “residential care” in B.C. and “long-term care” in Ontario, for seniors who need a lot of help). Unlike retirement homes, most nursing homes are heavily subsidized by the government—but you still have to pay part of the costs yourself, and in some cases having more money can help you afford extras like a private room.

The financial benefits of downsizing often go beyond what you net on the transaction. “What is often overlooked is downsizing can cut your expenses,” says Sass. That’s because some of your major ongoing cost items tend to vary according to the size or value of your property, including property taxes, maintenance and certain utilities like heating. Of course, you may not think you will see savings when you’re facing a sizeable condo or strata fee every month in your new place. But in doing the comparison, experts say you should allow at least 1% of the house value and sometimes more per year for not-so-obvious maintenance costs in your old home. Of course these expenses will vary quite a bit, so in some situations there won’t be savings at all. But if you’re moving from a large, older house with sizeable maintenance needs and moving to a newer condo without too many expensive amenities and reasonable condo/strata fees, then the yearly savings will often be several thousand dollars a year.

If you’re trying to maximize your up-front real estate payoff from downsizing, it helps if you can target communities with relatively low real estate prices within the regions you’re looking at, says Don Campbell, senior analyst and co-founder of the Real Estate Investment Network. So if you want to stay close to a relatively expensive area but save on real estate purchase prices, look just beyond easy commuting distance, he says. For example, consider Barrie if you’re hoping to be near Toronto, or Chilliwack if you want to be close to Vancouver. Also look for attractive communities with a little less real estate cachet compared to better-known communities in the same region, he says. Thus consider Vernon instead of Kelowna in the Okanagan Valley, or Comox Valley instead of Victoria on Vancouver Island.

But if you are considering moving provinces, you also need to consider varying governmental senior tax and benefit policies. For example, by my calculations, a single senior with $70,000 a year in taxable income and standard tax credits will pay more than $5,000 in higher combined federal and provincial taxes in high-tax Quebec compared with lower-tax B.C. Consider also that B.C. has a generous property tax deferral program for homeowners over 55 living there at least a year who have substantial equity in their homes: you can defer all property taxes until you pass on or sell the house at a cost which cumulates at an exceptionally low interest rate, currently 1% a year. (Alberta has a similar program for seniors 65 and over which currently costs 2.85% a year.) Some provinces have great government prescription drug programs (sometimes just for seniors, in other cases for all residents), while other provinces only help with drug costs if your income is exceptionally low.

If you are looking to relocate, it helps to find a community with good medical services that are reasonably close to friends and family—or at least has good airport access if it’s more distant. Also be sure to pick a locale that helps you enjoy an active lifestyle with plenty of social connections. If you have broad interests and an open mind, you might find your needs satisfied in a community that has plenty of common amenities like bike trails, card clubs, hobby groups, libraries, swimming pools and fitness centres. “Those kinds of things can be really good for getting people out of the house, getting them moving, getting them meeting more people,” says aging expert Lee Anne Davies, who blogs at agenomics.ca.

Also make sure you think about how your capabilities are likely to change as you age. Consider how decreasing mobility might cause problems contending with things like stairs and a large yard (unless you love gardening, in which case it might be worth it). This should extend to your choice of community as well. For example, many people are attracted to a quiet life in small towns and rural areas, but that can lead to isolation later in life when you may no longer be driving, says Davies. “A mistake that people make is they’re not thinking long term enough.”

Keep in mind too that moving is disruptive, expensive and just becomes harder to do as you age, so you don’t want to do it too often. Don’t buy a new place unless you’re pretty sure you want to live there for a while. “I would certainly suggest renting for a year first if people are moving to an area which isn’t familiar,” says Al Feth, a fee-for-service financial planner in Waterloo, Ont., who has helped a number of retirees with downsizing plans.

Whatever stage you consider downsizing, make sure it meets as many of your needs as possible. That’s what Bob and Helene Murray were hoping for when they decided to downsize and relocate. They netted a little over $1 million after costs from selling their five-bedroom 4,000-square-foot house in the Toronto suburbs. Now settled in downtown Montreal, they’re currently renting a 1,100-square-foot two-bedroom condo while they decide what kind of home they want to live in and in which neighborhood.

Meanwhile, they’ve found plenty of things to do, visiting regularly with relatives and enjoying lots of hobbies and activities. They play bridge, like water activities in the summer, skiing in the winter, and love street life in Montreal. “It’s so lively and so creative, and so much is going on,” enthuses Bob.

The Murrays have a year to make up their mind about where and what to buy, but they’re leaning toward a downtown condo in their beloved Montreal. Bob figures if they do that, they’ll have roughly $400,000 to $600,000 left from the proceeds of selling their Toronto home to add to their retirement nest egg. While the extra money isn’t the main reason for downsizing and relocating, it does give them more wherewithal to help enjoy what they hope will be a long and comfortable retirement.

Most of us want to stay in our homes as long as we can. Fortunately, there are plenty of things you can do to renovate or get assistance to help cope as you get older.

The typical two-storey home isn’t well-designed for advancing frailties. Expect the following renovation cost estimates if you live in a large city like Toronto, says David Wallace, vice-president of the Adapt-Able Design Group. Where renovating is feasible, homeowners can often recover costs when it comes time to sell. “Because of our aging population, we have more people with mobility issues who are looking for these features,” Wallace says. Renovations may also generate tax deductions or tax credits under a number of federal and provincial programs.

■ Bathroom renovations, including a raised toilet, grab bars in key locations, and the installation of a step-in shower or bath: $8,000 to $18,000

■ Exterior front steps replaced or supplemented by a ramp or vertical platform lift: $3,000 to $12,000

■ To get between floors, a stair-glide: $3,000 (for a straight-run) to $12,000 (with bends); a through-the-floor lift (a small elevator the size of a telephone booth): $40,000 to $60,000; a full-scale residential elevator: $80,000 to $100,000

Many seniors who need a bit of help can get by with a personal care aide coming in for a few hours a day. What governments are willing to pay for varies across Canada, but it’s limited in time and scope. If that isn’t an option, the cost of paying an aide for short visits is usually affordable for middle class retirees. Geriatric care manager Audrey Miller says the cost for bringing in a personal care worker through an agency for three hours a day is roughly $28,000 a year in Ontario, B.C. and Alberta. However, more extensive help can quickly escalate. Bringing in a live-in caregiver working through an agency, roughly 10 to 12 hours a day, is about $75,000 a year plus food and accommodation, says Miller. Attentive round-the-clock care can run to over $200,000 a year, she says.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Learn how the federal government’s 2024 budget can affect you and your money.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...