How much you really need to retire

Here's the cost of a typical middle-class retirement

Here's the cost of a typical middle-class retirement

Many advisers say you need retirement cash flow equal to 70% to 80% of your peak pre-retirement income. While that would be nice, most Canadians retire comfortably on far less.

“I get so upset when I hear advisers telling clients they need 70% to 80%,” says Annie Kvick, a certified financial planner and associate with Money Coaches Canada in North Vancouver. “I’ve had clients come to me at 67 and they’re still working because their adviser told them they didn’t have enough. When I looked at how much they really needed, I found they could have retired five years ago.”

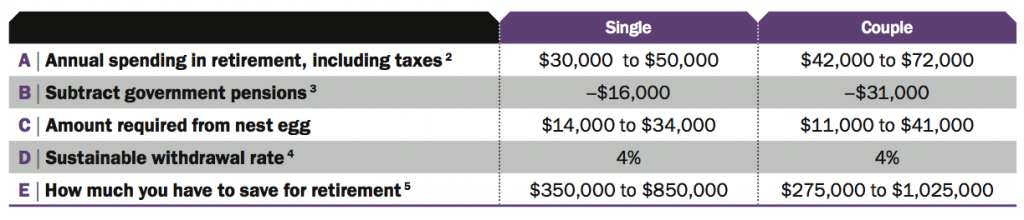

In my view, a better rule of thumb is to aim for a replacement ratio of 50% to 60% for couples, and 60% to 70% for singles, assuming you have a paid-for home and your kids are financially independent. Better yet, use actual dollar figures. Typical middle-class Canadian couples can live comfortably on $42,000 to $72,000 a year ($30,000 to $50,000 for singles), again assuming no mortgage or child costs.

If you wonder how you can make those figures work, consider the middle years of your working life when you probably carried a hefty mortgage, supported children, paid for work-related transportation and wardrobe costs, saved for retirement and paid a lot of income tax. In retirement, you get to strip out most of those costs, so you can have a similar lifestyle on much less income.

Adjusting to such a reduction in income is not always easy, so be careful not to ratchet up your standard of living too much while you’re working. That can happen if, after paying off your mortgage and getting the kids launched, you get used to spending the extra on luxuries.

“People need to ask, ‘Is this the standard of living that I can maintain throughout retirement?’ It may be time to step back and say, ‘We’ve been living high off the hog, but we can’t sustain this’,” says Lee Anne Davies, a retirement educator with Agenomics. “I don’t hear enough people being honest about their lifestyle and that’s the conversation you need to have with yourself.”

Even in that situation, the good news is you likely proved you could live modestly in your middle years. In many cases you should be able to do it again in retirement without great sacrifice if you have to.

How much do you need to save, anyway? Here’s the cost of a typical middle-class retirement starting at age 65(1)

Notes: (1) All amounts are in 2014 dollars, reflecting current purchasing power. Spending projections for subsequent years are adjusted for inflation, so real purchasing power would be unchanged. (See “What’s Your Magic Number” in the Summer 2013 issue for more.) (2) Typical middle-class income before tax. Assumes a paid-for home. (3) Typical annual amount for Canada Pension Plan and Old Age Security based on retiring at age 65, assuming a fairly long career at average salaries or better. (CPP and OAS are adjusted to pay more if deferred, and CPP is adjusted to pay less if started earlier.) We’ve assumed no employer pension, but this should be included here if you have one. (4) Approximate amount that can be withdrawn from initial nest egg if retiring at age 65, with only a small risk of outliving the money, based on a rough consensus of experts. (5) Required at start of retirement at age 65 (C/D). You’ll need more if you retire earlier, or less if you retire later.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Learn how the federal government’s 2024 budget can affect you and your money.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...