Millionaires by age 50

This couple is on track to reach financial independence earlier than most.

This couple is on track to reach financial independence earlier than most.

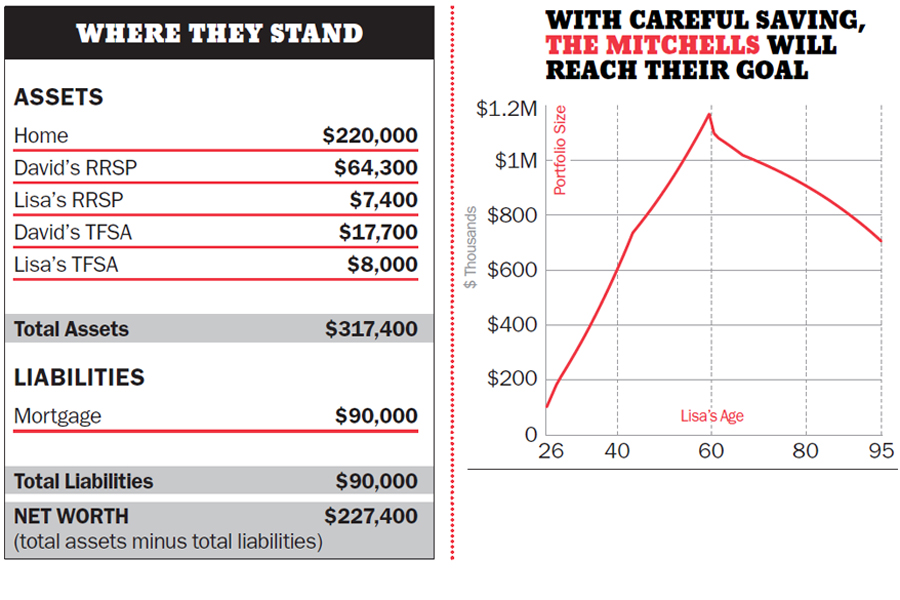

Like many young people saving for their future, David and Lisa Mitchell are working hard to become financially independent. The Winnipeg couple, ages 32 and 26 respectively, would like to have a comfortable retirement with an annual income of $70,000. But they also want the option of working less as they get closer to that goal. By the year 2030, they would like to have $1.2 million in savings. By then, David, who currently makes $69,000 as an engineer, would be 50; Lisa would be 44: she now earns an annual salary of $67,000 as a nurse and is contributing to a defined benefit pension. While the couple expects to continue to work until David is 65 and Lisa is 59, they don’t want to be dependent on their salaries. “We want the freedom to take our feet off the pedal a little earlier than most,” says David. However, they also want to have children within the next couple of years, meaning Lisa would switch to part-time hours and earn about $20,000. The couple have managed their finances well so far and together have almost $100,000 in savings. They also expect to finish paying off their $220,000 mortgage in less than three years.

By saving diligently, the Mitchells will be close to meeting their goal, according to MoneySense retirement columnist David Aston. When David Mitchell turns 50, they should be able to scale back so they only need to earn enough to cover day-to-day expenses for a few years. Putting new money into savings won’t be necessary. From that point, their nest egg can be expected to grow enough by itself to cover an above-average retirement lifestyle in their 60s. Despite a drop in income when Lisa goes part-time, the couple should be able to save 20% of their combined salaries once the mortgage is paid off. That should let them salt away $22,135 a year into their combined nest egg, including $5,000 in annual RESP contributions for two children. If they can save that amount steadily, their nest egg should grow to $740,000 in today’s dollars by the time David is 50 and Lisa is 44. Assuming a 3% real return, that $740,000 would grow to $1.14 million in today’s dollars by about the time David is 65 and Lisa is 59. Before tax, they could expect an estimated $73,000 a year in retirement income: $24,000 in government benefits, $12,000 from Lisa’s pension and $37,000 from their nest egg.

Do you want MoneySense to see if you’re on track to meet your own financial goal? If so, drop us a line at [email protected]

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

This prepaid travel card eliminates foreign exchange charges on your purchases abroad, though the loading fees could irk some...

Food and beverage company expects organic growth of 4% in 2024

General Motors reports strong first-quarter profits as prices help offset small U.S. sales dip.

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Managing lifestyle creep is challenging financially and psychologically, especially with inflation. Expert strategies keep day-to-day spending in check.