Retire like it’s 1999

Your portfolio’s fortunes can change dramatically based on your chosen retirement date

Your portfolio’s fortunes can change dramatically based on your chosen retirement date

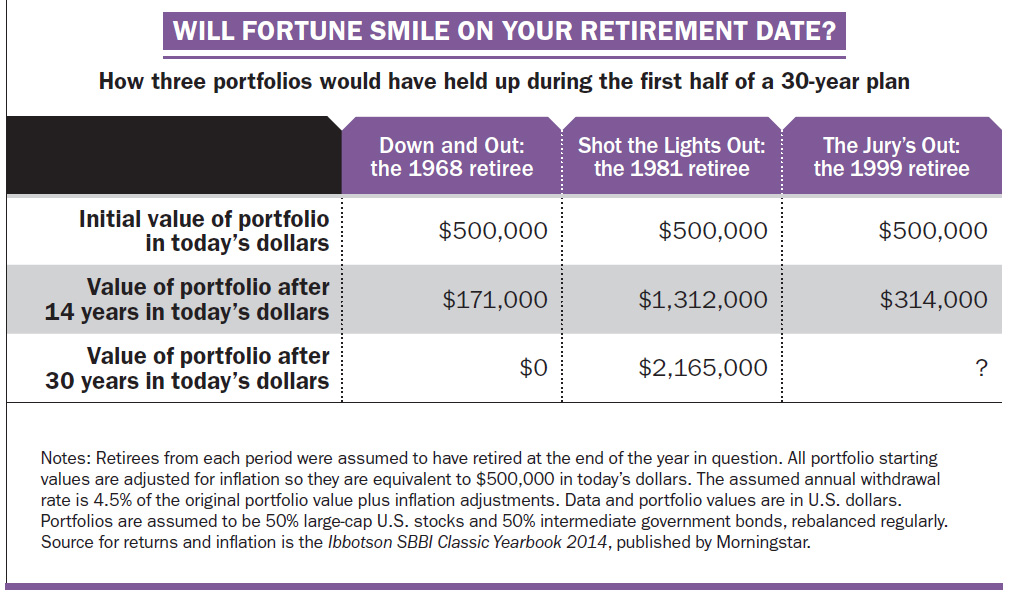

We’ve seen how your portfolio’s fortunes can change dramatically based on your chosen retirement date. That begs the question of how the current generation of retirees is faring. Since many financial plans assume a retirement portfolio needs to last 30 years, we looked at the situation for someone who is almost halfway there.

The last decade and a half has been challenging for stocks, although bonds have done better. The year 1999 was a particularly unfavourable date to retire: many stocks were trading at extremely high levels during the dot-com bubble, and the bear market that followed was a prime example of an unlucky sequence of returns. It’s too soon to answer conclusively whether a retiree’s nest egg will be sustainable over a full 30-year period, but it’s looking iffy based on a 4.5% withdrawal rate. If you had retired in 1999 with the equivalent of $500,000 in today’s money, you would still have a portfolio worth about $314,000 at the end of 2013. That’s significantly ahead of where the unfortunate 1968 retiree was after 14 years (see below), but not enough to be confident the money will last the full 30 years.

To be fair, however, it’s important to acknowledge that many people who retired in 1999 were in their peak earning years during the longest bull market in history (from 1987 to 2000) and probably benefitted from the massive gains in stocks during those years. That would have enabled them to build a retirement portfolio substantially bigger than it might have been. So the fortunes of the 1999 retiree have probably averaged out to some degree.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Learn how the federal government’s 2024 budget can affect you and your money.

U.S. inflation comes in hot, Delta says revenge travel is alive and well, doubling your CPP benefits, and AI...

History repeats (or rhymes) itself in latest market upswing, FHSA celebrates its first birthday, investors getting rich from stocks,...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...