How to invest in Canadian bank ETFs

Of the many and diverse funds devoted to the Canadian banking sector, make sure yours has the right allocation and strategy.

Advertisement

Of the many and diverse funds devoted to the Canadian banking sector, make sure yours has the right allocation and strategy.

Though they’re well represented in Canadian stock indices, you can see why some investors would want even more exposure to Canadian banks. They have enviable dividend growth histories and ample current yields. They offer relatively stable earnings that are not vulnerable to global tariffs or supply-chain shocks. For decades (and with support from the regulatory regime), they’ve successfully fended off all competitors that have tried to breach their moats. Plus, their payouts typically qualify for the Canadian dividend tax credit when held in taxable accounts, making them highly tax-efficient.

But, banks are a different animal than most TSX stocks. Typical valuation metrics like price-to-earnings ratios don’t always apply cleanly because bank earnings are heavily regulated, cyclical and influenced by capital requirements, interest-rate spreads and credit risk—factors that aren’t captured well by earnings multiples alone.

Instead, Canadian investors need to consider balance sheet and risk management metrics. For example, loan loss provisions, which measure reserves set aside for potential defaults can reveal how conservative a bank is during uncertain times. By contrast, the cost-to-income ratio shows how efficiently a bank operates relative to its net interest revenue, with lower numbers signalling better efficiency.

If all that sounds a little overwhelming to you, you’re not alone. These are complex institutions. That’s why, if I were looking to go long on Canadian banks, I’d delegate the task to an exchange-traded fund (ETF) that holds all six.

Get up to 3.00% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.40%.

Earn 4.50% for 5 months on eligible deposits up to $500k. Offer ends January 31, 2026

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

That shifts your thesis from trying to evaluate which single bank will outperform to betting that, over time, the Canadian banking sector as a whole will grow its customer base, expand into new lending verticals like digital banking, wealth management or business financing, and continue to benefit from secular tailwinds like population growth and housing demand.

This ETF segment is one of the most competitive in Canada, with a wide range of options pursuing different strategies. Here’s a quick guide to the types you’ll encounter, the trade-offs between risk and reward, and what type of investor each one might be suitable for.

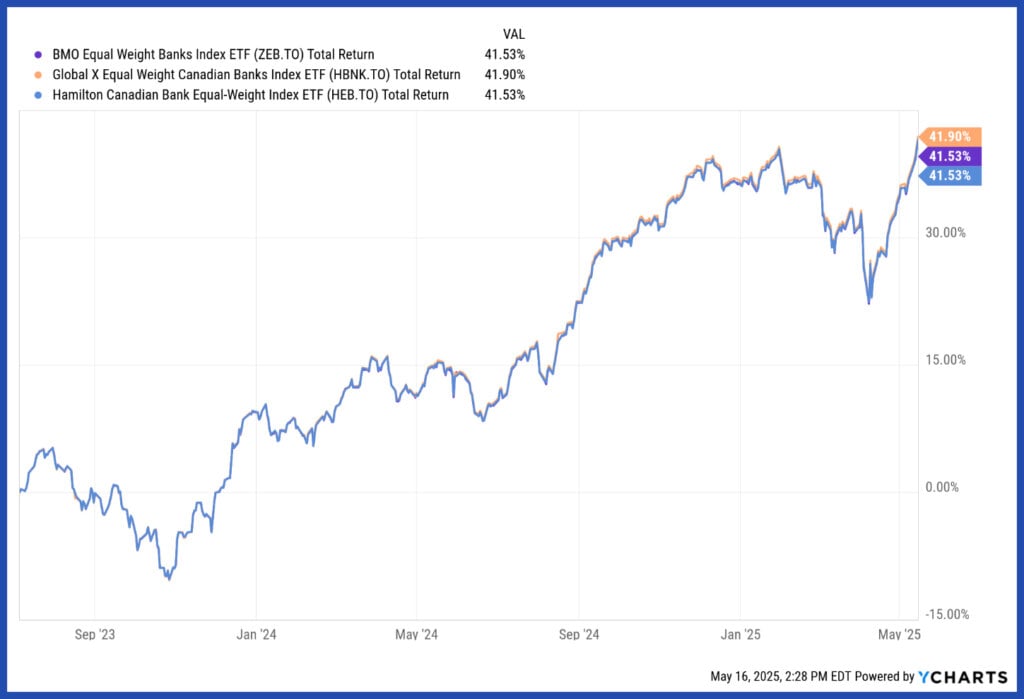

The simplest and most popular Canadian bank ETFs you’ll come across are the equal-weighted ones. These include the Global X Equal Weight Canadian Banks Index ETF (HBNK), BMO Equal Weight Banks Index ETF (ZEB), and Hamilton Canadian Bank Equal-Weight Index ETF (HEB).

All three track the Solactive Equal Weight Canada Banks Index, which, as the name implies, assigns an equal weight—around 16.67% each—to the Big Six banks mentioned earlier, rebalancing periodically to maintain that allocation.

This avoids the flaws of a market cap-weighted strategy in such a concentrated sector, where giants like Royal Bank of Canada (RY/TSE) and TD (TD/NYSE) would otherwise dominate the smaller banks like CIBC (CM/NYSE) and National Bank of Canada (NA/NYSE). It also creates a natural buy-low-sell-high effect as the index systematically trims winners and adds to laggards during each rebalance.

All three ETFs pay monthly distributions, which is a nice upgrade from the underlying bank stocks themselves, which pay quarterly. As of May 14, the distribution yields were:

Tax efficiency is solid, as most of the income is classified as eligible Canadian dividends, with occasional return of capital.

In terms of costs, ZEB is the priciest with a 0.28% MER (management expense ratio), largely due to its size and brand recognition. HEB, meanwhile, says it’s waiving its 0.19% management fee through January 31, 2026. And it most recently reported a 0.25% MER as of February 28, 2025. HBNK looks to be the cheapest of the bunch, with a 0.04% MER and a 0.01% TER. They’ve all posted more or less the same returns historically.

Use case: These bank ETFs are ideal for investors who want straightforward, no-frills exposure to Canadian banks, are agnostic about which bank will outperform, and appreciate the convenience of monthly distributions, even if it means paying a small fee for that automation.

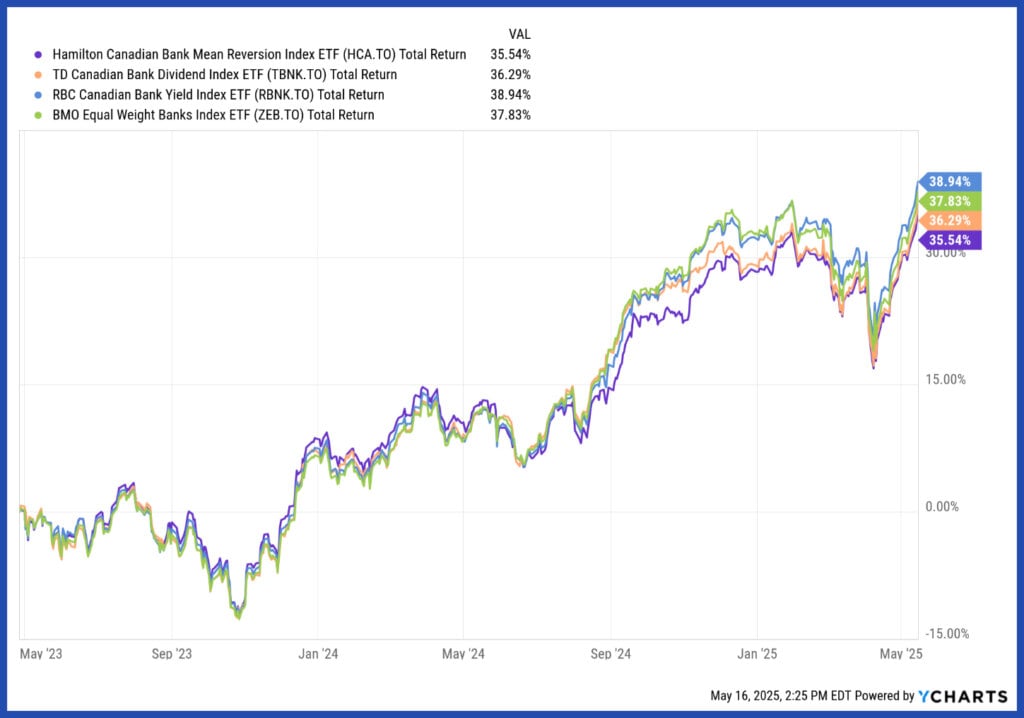

Fundamental weighting is a strategy where ETF holdings are allocated based on financial metrics—rather than stock price or market cap—with the goal of better reflecting a company’s economic importance.

You may already be familiar with market cap and equal weighting, but fundamental weighting assigns weights to bank stocks based on specific criteria, and there’s no universal standard—it all depends on how the ETF is built.

For example, the TD Canadian Bank Dividend Index ETF (TBNK) tracks the Solactive Canadian Bank Dividend Index, which uses a rules-based methodology to rank the Big Six Banks by dividend growth. More weight tends to be allocated to those with stronger dividend growth histories.

In contrast, the RBC Canadian Bank Yield Index ETF (RBNK) tracks the Solactive Canada Bank Yield Index, where banks are weighted based on indicated dividend yield—essentially the forecasted dividend as a percentage of share price. This aims to tilt the fund toward higher-yielding banks at any given time.

Then there’s the Hamilton Canadian Bank Mean Reversion Index ETF (HCA), which tracks the Solactive Canadian Bank Mean Reversion Index TR. Every quarter, HCA typically allocates 80% of its portfolio to the three banks that have underperformed recently, and 20% to the three that have outperformed, banking (pun intended!) on the idea that underperformers could bounce back.

These custom strategies can come at a higher cost. TBNK charges a 0.28% MER, RBNK comes in at 0.32%, and HCA tops the list at 0.45%. So far, those extra fees haven’t translated into major outperformance. From May 2023 to May 2025, total returns for these ETFs have been within about 1% cumulatively above or below the simpler equal-weighted ZEB.

Use case: These ETFs just might be a fit if you want to get a little fancier with your exposure—making a more active bet on which banks will outperform based on dividend growth, yield or price reversion—and are comfortable paying higher fees for the possibility (not a guarantee) of outperformance.

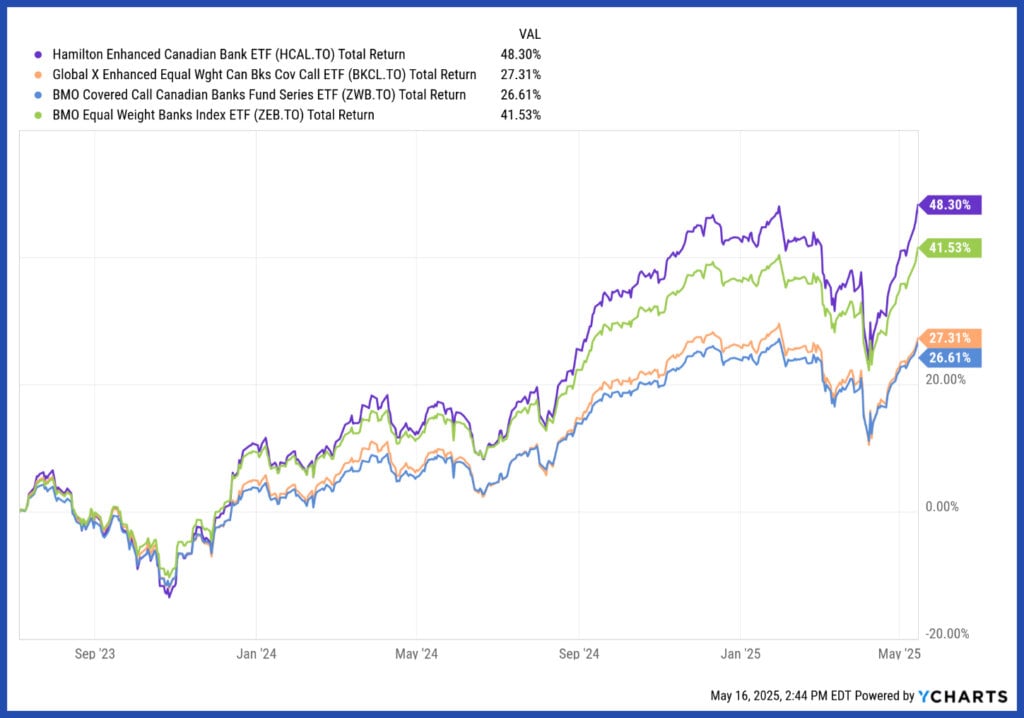

These ETFs fall under the umbrella of alternative strategies, meaning they go beyond traditional long-only buy-and-hold approaches. They often employ derivatives or leverage, aiming to enhance some aspect of exposure, whether that’s yield, price returns or both.

A classic example is the BMO Covered Call Canadian Banks ETF (ZWB). It holds all six major banks, mirroring ZEB, but it layers on a covered-call strategy by selling options on its holdings. This caps upside but boosts income, generating a yield made up of dividend income, capital gains and return of capital.

BMO sells these calls out of the money and on a discretionary basis, meaning not every position is covered at all times, giving the portfolio slightly more upside potential compared to systematic call-writing strategies. You could get a solid 6.66% distribution yield, but with much more muted price appreciation.

The Hamilton Enhanced Canadian Bank ETF (HCAL) can be used for a different approach. It doesn’t use options at all. Instead, it applies 1.25 times (125%) leverage to the Solactive Equal Weight Canada Banks Index, the same one used by ZEB, HEB and HBNK.

Unlike typical leveraged ETFs that reset daily via swaps, HCAL borrows money using cash margin loans, which means its returns aren’t distorted by daily compounding. This setup amplifies both upside and downside, and also boosts yield to 6.42%, as distributions are paid on the larger notional exposure.

Then there’s Global X Enhanced Equal Weight Canadian Banks Covered Call ETF (BKCL), which is meant to blend both strategies. It invests in a Global X ETF that writes bank covered calls, then borrows to push exposure to 1.25 times, aiming to combine high yield with modest growth.

It currently offers a 15.01% yield, but there’s no free lunch—income can fluctuate month to month. And, there’s no guarantee the ETF’s price will hold up as premiums vary and leverage amplifies swings.

All three ETFs carry also much higher fees than the aforementioned funds: ZWB at 0.71% MER, BKCL at 2.15% MER (including leverage costs) with a 0.35% TER, and HCAL with a total MER of 2.16%.

Their performance has been mixed. Both ZWB and BKCL, even with higher income reinvested, have underperformed ZEB on a total-return basis, mostly due to the drag from a capped upside. HCAL, by contrast, has outperformed, but not in a perfect 1.25-times multiple. For example, if ZEB returned 41.53% over a given period, 1.25 times would suggest 51.91%, but HCAL delivered less due to the cost of borrowing.

Use case: These enhanced bank ETFs may appeal to income-seeking investors looking to boost cash flow or make tactical plays on Canadian banks. But they come with added risk and higher fees and should ideally be held in registered accounts—like a tax-free savings account (TFSA) or a registered retirement savings plan (RRSP)—to avoid the added tax burden.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The first quarter finally broke the pattern of steadily rising markets, but energy stocks soared.

Geopolitics, rising oil prices and ETF inflows are shaping Bitcoin’s outlook. Is now the right time for Canadian investors...

Wealthsimple's direct indexing brings a tax-saving investing strategy to a wider group of investors, but the number likely to...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

In the likelihood of a protracted conflict, these experts think people in or close to retirement need to review...

Look under the hood before buying some popular Canadian sector ETFs. There may be alternatives that better represent the...

Lululemon profits dip, Couche-Tard surges, and Power Corp declines. Here’s what investors need to know about Q4 results...

U.S.-Iran tensions have shaken markets, but experts urge investors to stay disciplined, avoid emotional moves, and use volatility to...

Canadian companies face a turbulent quarter, with Algoma Steel losing big and Transat posting gains amid major corporate moves.