New mortgage rules to steer consumers to big banks

They'll also limit choice and increase the cost of borrowing

They'll also limit choice and increase the cost of borrowing

Are you thinking about going to one of the smaller non-bank lenders for your next mortgage? If your property is worth more than $1 million you may be out of luck.

That’s just one of the conditions consumers shopping for a mortgage will now need to consider as the latest round of federal mortgage rules take hold. Under the new rules non-bank lenders will likely have to turn away sizeable portion of mortgage seekers, leaving the big banks as their only option. For consumers it will mean less choice and higher rates on their next mortgage.

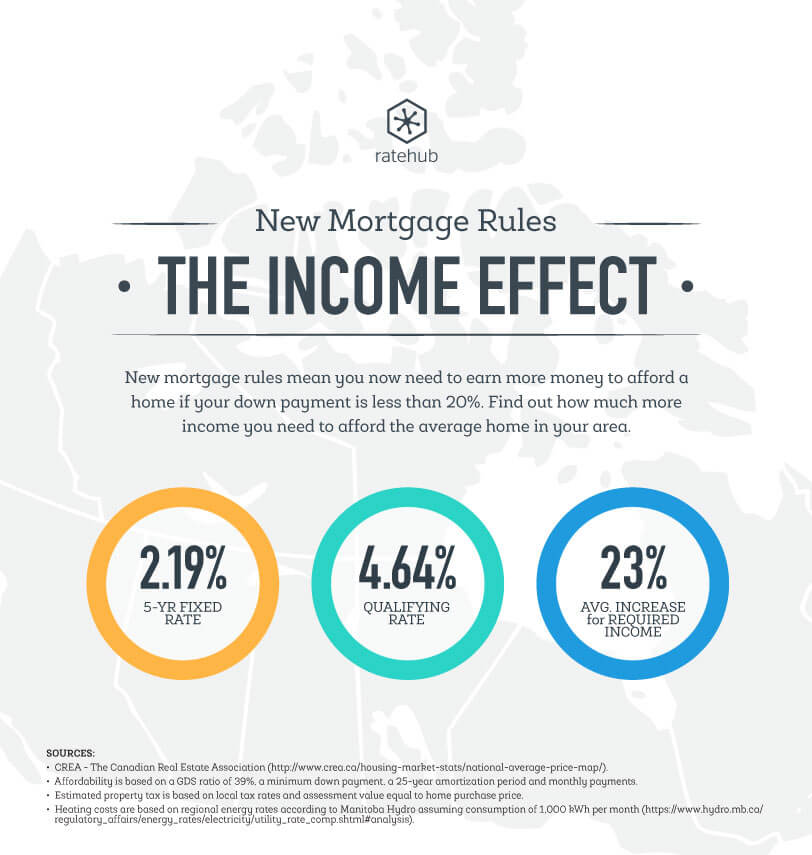

The new regulations, which kicked in on Nov. 30, impose stricter limitations on the types of mortgages that will qualify for mortgage insurance. In the past these tighter rules targeted risker, high-ratio mortgages, but the government is extending some of these same rules to less risky low-ratio loans.

Although the mortgage insurance is meant to protect lenders, the changes are going to trickle down to a sizeable segment of consumers looking for a new mortgage or preparing to refinance an existing one. Here’s a breakdown of the loans that will no longer qualify for mortgage insurance:

Based on the nature of mortgages affected, consumers in Vancouver in Toronto stand to see the greatest impact. According to Robert McLister, the founder of RateSpy, this will affect mono-lenders like Home Trust, First National and Home Trust from serving this portion of the market.

Typically these non-bank lenders need to insure all of the mortgages in their portfolio in order to be able to raise capital to lend out, he explains. Now lenders that want to service this very lucrative portion of the market will have to borrow from one of the big banks, which is going to raise the cost of capital.

“That’s is going to come at a premium,” says McLister. Anyone looking to borrow for a home worth more than $1 million should expect to pay higher rates. “Most of the mortgage finance companies have temporarily or permanently halted mortgages on properties on $1 million or more or have announced rate premiums.” At least for now, companies like Marathon Mortgage and Xceed Mortgage have pulled some of these products (like refinances) altogether, he adds.

While he doesn’t expect smaller lenders will completely disappear from this segment of the market, the new regulations will mean paying rate premiums of between 15 to 25 basis points. “It makes them less competitive than the banks,” says McLister, who adds the banks are already extremely aggressive at courting qualified borrowers.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Equifax Canada says it’s exploring how rent data could factor into credit scores to help make credit and financial...

Extreme weather is the new norm, so it’s smart to prepare for power outages. Battery backup power could be...

When is capital gains tax payable on the sale of property? And at what rate are capital gains taxed?...

Understanding industry jargon can make you a better real estate investor.

Learn how the federal government’s 2024 budget can affect you and your money.

The data behind the top places to buy real estate in Canada.