RRSP vs TFSA: Which should you top up in retirement?

The TFSA wins because it's flexible

The TFSA wins because it's flexible

Q: I’m a 60-year-old retired school teacher as of this past July 2017. I have $44,000 in unused RRSP contribution room. Should I max out my contribution room on my 2017 taxes? Or just stick to topping up my TFSA?

—Chris

A: Hi Chris. Thanks for the question. Please note that RRSP only counts as a deduction against “earned income” which includes:

If your income is not from one of these sources it is likely not considered “earned income” meaning your RRSP contribution will not be a deduction. If you do have earned income then let’s note a few things:

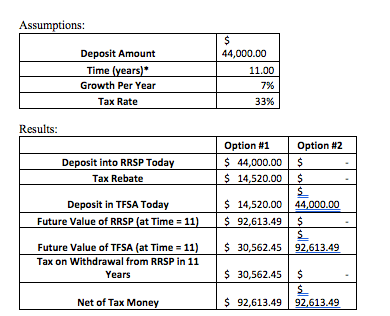

Since you are retired, I am assuming your income will stay fairly constant moving forward and you will not change tax brackets. As such, you are likely unable to take advantage of the tax deferral the RRSP offers. This is illustrated in the example below.

Option #1: Deposit $44,000 to max your RRSP today and deposit the tax rebate into your TFSA today. Let both grow for 11 years until age 71 at which time you must convert your RRSP and begin drawing on it.

Option #2: Deposit $44,000 into your TFSA today and leave it to grow until age 71; at 71 you will not be forced to draw on this money.

Conclusion: Both result in the same end value since you are facing a constant tax rate. Further, your RRSP must be converted upon your 71st birthday whereas you can leave your TFSA to grow for as long or short as you desire. Additionally, it is usually recommended to draw out of your RRSP rather than your TFSA earlier in retirement as your TFSA will incur no tax upon your passing or any withdrawals as compared to your RRSP which will be taxed fully.

What we can conclude is this. If your income will be staying constant throughout your retirement I would advise you to top up your TFSA rather than your RRSP for the following reasons

I would still suggest topping up your TFSA even if you see your income dropping in the future due to the preferential tax treatment it receives upon your passing and the flexibility it provides as compared to your RRSP.

Andrew Fox is a certified financial planner with Fox Wealth Mangement in Calgary.

MORE FROM AN INVESTMENT EXPERT:

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Doing home renovations? Find out if there are any tax incentives that Canadians are able to claim.

You can amend previous tax returns to include new information, such as investment management fees for a non-registered account....

Money in a LIRA or LIF is intended to last a lifetime, making it difficult to access more than...

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...

Do Canadians have to file a trust tax return this year? What is a bare trust? What are the...

Changing your status to common-law has an impact on your tax return and government benefits. Here’s how to know...

Would leveraging the equity in a home to invest in dividend-paying investments lead to tax repercussions?

The flat-rate home-office expense deduction is no longer available for 2023. But eligible employees who work from home can...

Just because you paid loads into a program doesn't mean you'll get EI benefits when you retire