Performance: The Ultimate Couch Potato Portfolio Guide

Updated for 2022, a look back at the performance of the MoneySense Canadian Couch Potato Portfolio Guide, looking at it all, from core to advanced portfolio models.

Updated for 2022, a look back at the performance of the MoneySense Canadian Couch Potato Portfolio Guide, looking at it all, from core to advanced portfolio models.

The MoneySense “Ultimate Couch Potato Portfolio Guide” shows the many ways Canadian investors can access a couch potato portfolio. You don’t have to use exchange-traded funds (ETFs) to hold a couch potato portfolio, but ETFs are certainly the most common route to creating a sensible, low-fee, globally diversified portfolio. You’ll also find couch potato basics, plus links to the couch potato portfolio models. Let’s compare the core couch potato portfolios with the advanced couch potato models.

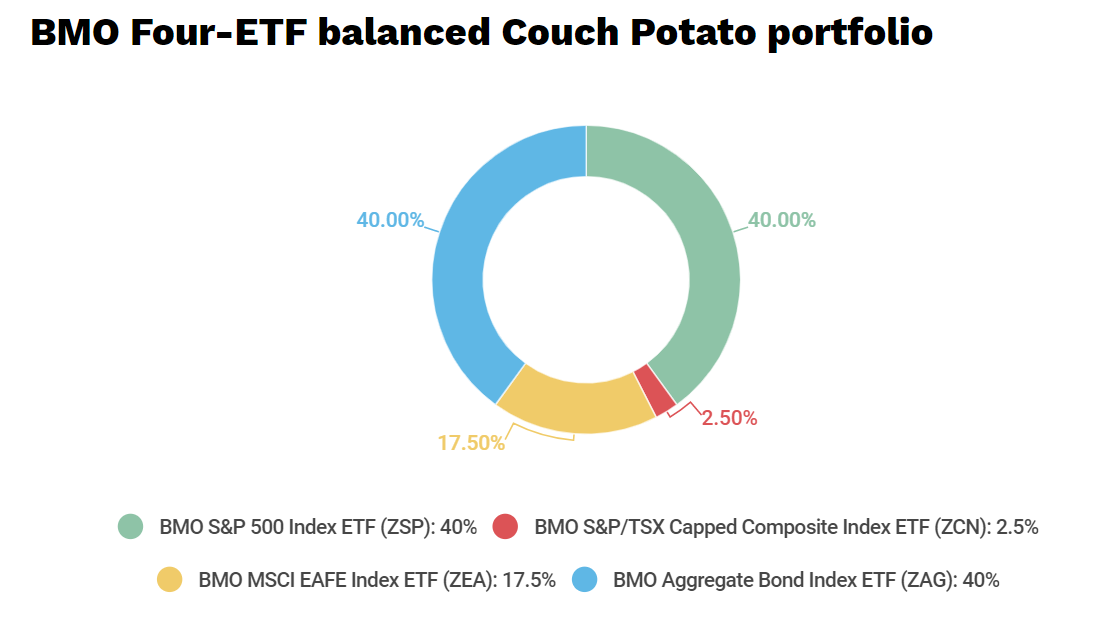

Here’s a core balanced couch potato portfolio. A classic balanced portfolio is typically made up of 60% stocks and 40% bonds. You could decide to increase growth (more stocks) or decrease it (fewer stocks), depending on your time horizon and tolerance for risk.

This traditional couch potato portfolio approach invests in Canadian stocks, U.S. stocks, international developed market stocks and Canadian bonds using ETFs or index mutual funds.

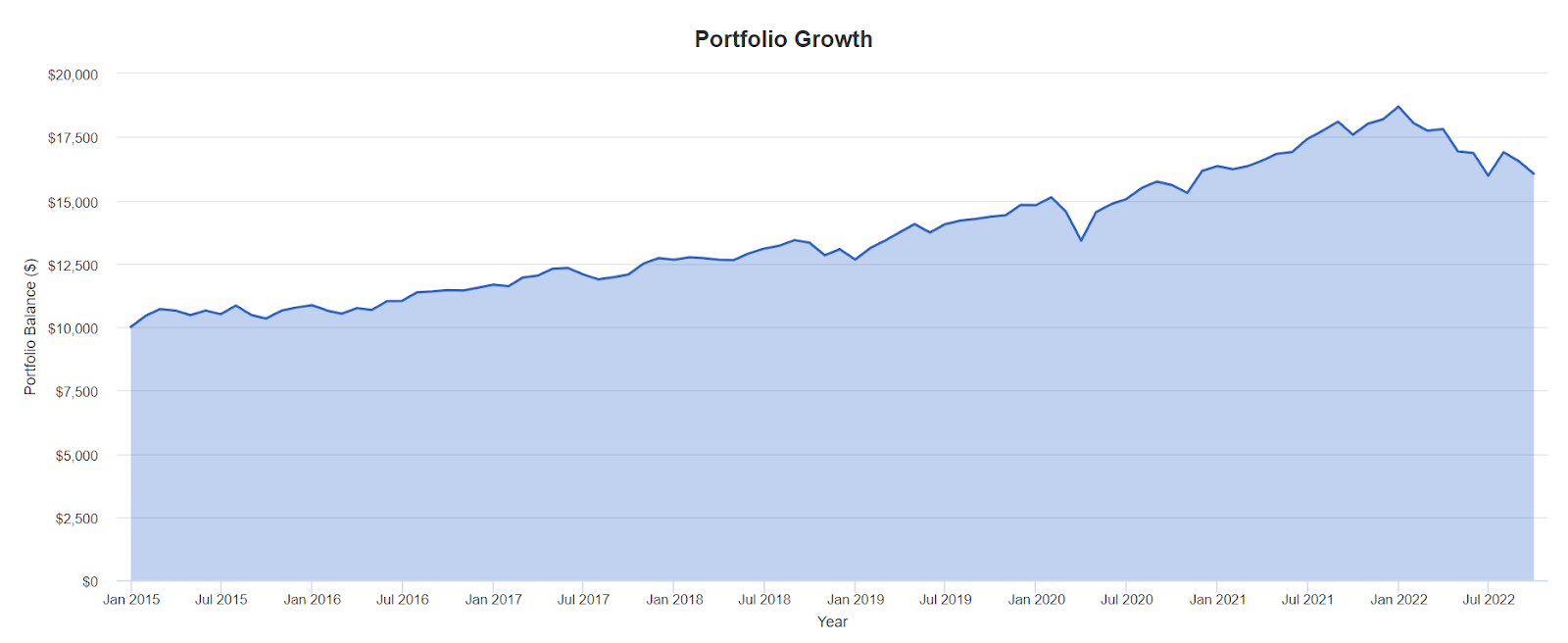

How has it performed? Here’s the total return (including dividends and dividend reinvestment) from January 2015 to September 2022. The time period for this evaluation is based on the availability of the actual BMO ETFs.

Source: portfoliovisualizer.com, January of 2015 to end of September 2022

Here are the returns for the individual assets for the period. All charts and tables in this post are courtesy of portfoliovisualizer.com.

The BMO Balanced Couch Potato Portfolio has delivered very solid annual returns since 2015. That said, the portfolio has come under stress over the last year, particularly in 2022 as stock and bond markets struggle with inflation and fears of rising interest rates. The balanced portfolio model is down 10.52% over the last year and is in the red 15.46% year-to-date.

Now let’s have a look at the returns for the other balanced models from the MoneySense Canadian Couch Potato Portfolio Guide, including iShares Balanced Couch Potato Portfolio and Vanguard Balanced Couch Potato Portfolio, along with the above BMO Balanced Couch Potato Portfolio.

You can see that the iShares two-ETF model underperforms the BMO four-ETF model for the 3-year, 5-year and full periods of evaluation. That is largely due to higher fees you would pay for the simplicity of the two-ETF model. Doing an extra bit of work and creating your own four-ETF couch potato model could be in your favour, if you’re comfortable with the additional portfolio rebalancing that would be required.

Both iShares and Vanguard offer ETFs with Canadian, U.S. and international stocks and Canadian bonds. You can build the four-ETF model using those ETF providers.

The Vanguard portfolio is the laggard, as the all-world ETF it offers 10% exposure to emerging markets. Unfortunately, these markets have performed poorly in recent years. Plus, Russia’s invasion of Ukraine and a potential redrawing of the global trade maps have put added pressure on the fund’s performance. Investors are surely taking the additional geopolitical risks of developing nations into consideration.

Yves Rebetez, partner at research firm Credo Consulting, suggests that many investors might consider passing onemerging markets (EM) for the time being. He and I DM’d on Twitter:

“Problems arise on democratic and individual freedoms. The composition of EM is a challenge. Saudi Arabia, China, Russia … well you get the gist of that argument which is why I respect the FRDM ETF.

“The environment is rather challenging to say the least … and personally yeah I’d rather, for the moment, miss out on any opportunity to invest in emerging markets. We can add in the fact that the strong U.S. dollar presents an additional risk to emerging markets.”

I will leave it up to you whether or not you add emerging markets (for example, via a global ETF that includes them) to your couch potato portfolio based on your financial goals and risk tolerance.

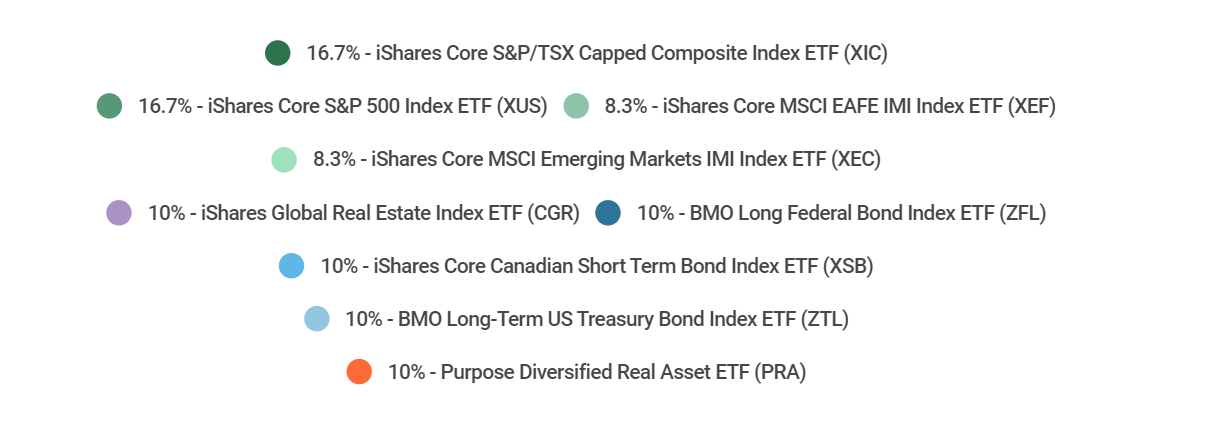

Next, let’s look at the performance of the advanced couch potato portfolios at various risk levels. These portfolio models are constructed as all-weather portfolios. They should be ready for changes in the economic environment, including inflation or stagflation.

I should note that the inflation-fighting assets—such as commodities, gold and commodity stocks—may not be necessary if you are in the accumulation stage, meaning you’re building up your portfolio. Over long periods of 15, 20 years or more, stock markets have made a wonderful inflation hedge. In retirement, or as we approach the retirement risk zone, protecting against near-term inflation risks is very important.

Here are the compositions for each portfolio type.

Let’s break down the performance of the advanced portfolios from January 2021 through to September 2022. This period takes into account the start date for the ETF assets available. And the start date coincides with the beginning of inflation worries in early 2021.

Admittedly, it’s a complete fluke that I looked at couch potato portfolios with inflation fighters just months before inflation and stagflation reared their ugly heads. Those readers who liked the idea of adding dedicated inflation-fighting assets have been rewarded.

When I compared the Advanced Portfolios in March 2022, the balanced growth portfolio was out in front, thanks to its greater allocation to stocks. That portfolio built up a nice lead in 2021. As of September 2022, the Conservative Portfolio has a slight lead, thanks to the greater allocation to the inflation fighters – that Purpose Real Asset ETF. The Balanced and Balanced Growth models are essentially tied.

And here are the returns for the portfolio assets for the same period.

See how Canadian stocks led the way on the equity front, as emerging markets (XEC.TO) are at the back of the pack. Emerging markets are under pressure due to inflation and the war in Ukraine. Also, emerging markets can perform poorly when the U.S. dollar runs strong, and it’s nearing the highs of the last 10 years.

The Purpose Diversified Real Asset ETF and real estate investment trusts (REITs) responded as expected; they thrived during unexpected inflation. That said, recently, REITs have struggled due to recession worries. The Canadian stock market did well overall, due to energy and commodities exposure. Every asset is negative in 2022, except for the real asset fund.

In an environment of rising rates, the longer-dated treasuries ZFL.TO and ZTL.V fell dramatically in price, compared to the shorter-dated bond ETF XSB.TO. The longer-duration bond ETFs have more price sensitivity to rising rates.

Here is a comparison between the Advanced Portfolio models from January 2015 through September 2022. The BMO Balanced Portfolio would have outperformed the Advanced Balanced Portfolio for this period. Once again, the inflation fighters can be a drag on portfolio performance during disinflationary times (what we experienced from 2015 to 2020).

We might be in the early innings of inflation. So, keep in mind, there hasn’t been a true test of inflation assets. Stagflation—when inflation is high and growth is slowing—can last for several years. Just look at the stagflation of the 1970s as it seeped into the 1980s (more on that later).

Investment assets have yet to see ongoing inflation or stagflation pricing, although asset performance in 2021 and 2022 is hinting at how they might react in a prolonged inflationary environment.

We are currently in a stagflationary environment. But, of course, no one knows if we are in the early stages of stagflation or if the central banks can tame inflation by raising rates—and hence, cool off price increases. From the National Post, a repost of a Financial Times article:

“The stagflationary shock of 2022 is truly global, with diverging growth and inflation expectations across most countries with many different factors exacerbating the trend in a synchronized way.

“In country after country, similar trends can be seen playing out—a surprise surge in prices and decline in activity over the past few months—as expectations for the year deteriorate.”

The period of stagflation related primarily to the 1973 oil crisis, when oil nearly quadrupled in price, lasted for several years. It’s up to you to decide whether you want additional dedicated inflation-fighters in your portfolio in case this stagflationary environment might persist.

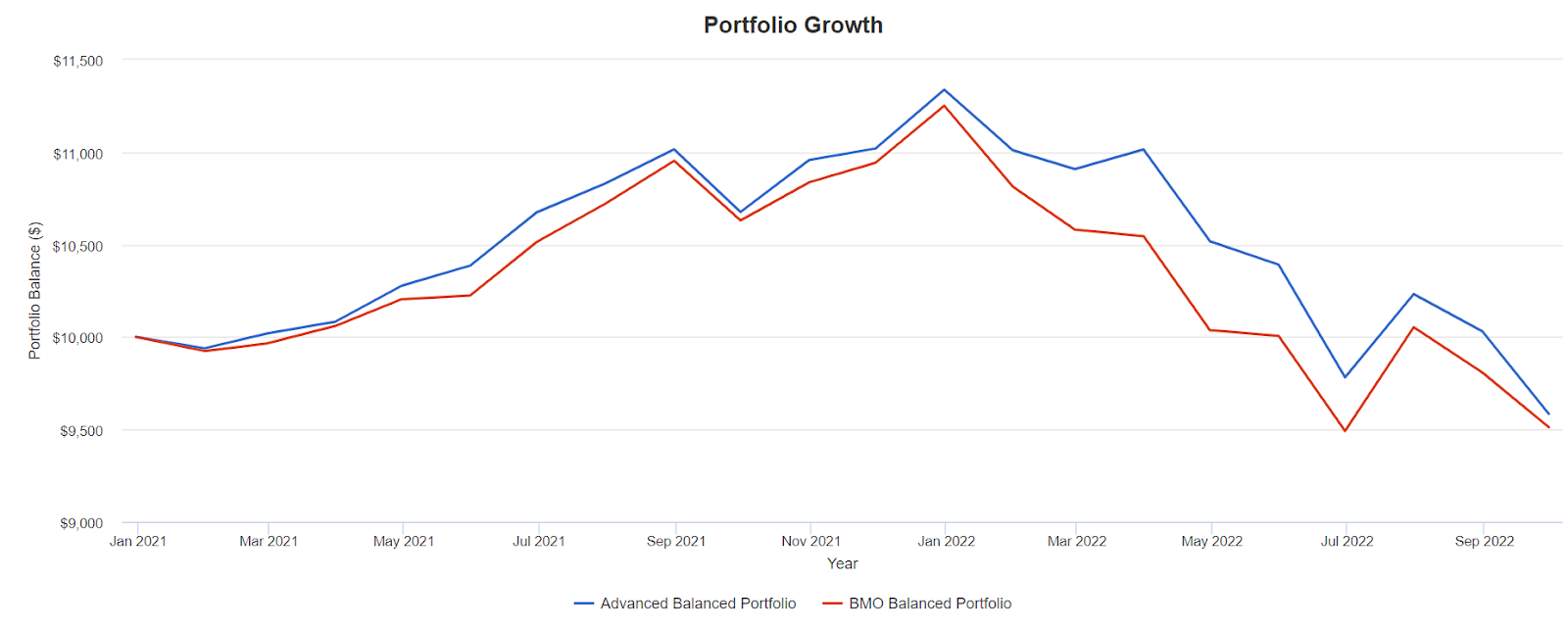

So, how do these portfolios stack up against each other? Here’s the near-term comparison of balanced portfolio models, core versus advanced.

The BMO balanced model is down 5% since January 2021, while the advanced balanced model is now not that far behind. The market appears to be thinking that inflation might be tamed. The inflation-fighting assets began to fall in the second quarter of 2022.

If we look back to 2015, we’ll find that the core model outperforms. (I’ve substituted for long-term treasuries to create the chart with an approximation.)

Over the long run, the BMO Balanced portfolio delivered an annual return of 5.9% annual, versus 4.7% for the advanced model. We would expect the core model to outperform in a disinflationary period, or when inflation is mostly under control. If we remain in an inflationary or stagflationary environment, the advanced couch potato model should outperform the core portfolio.

All that said, there is often very little cost to adding that inflation protection, according to what I see in my research. And in most periods between the 1970s and now, adding gold, commodities and REITs as increased the performance of a balanced portfolio.

Here is a wonderful visual presentation on inflation, stagflation and deflation.

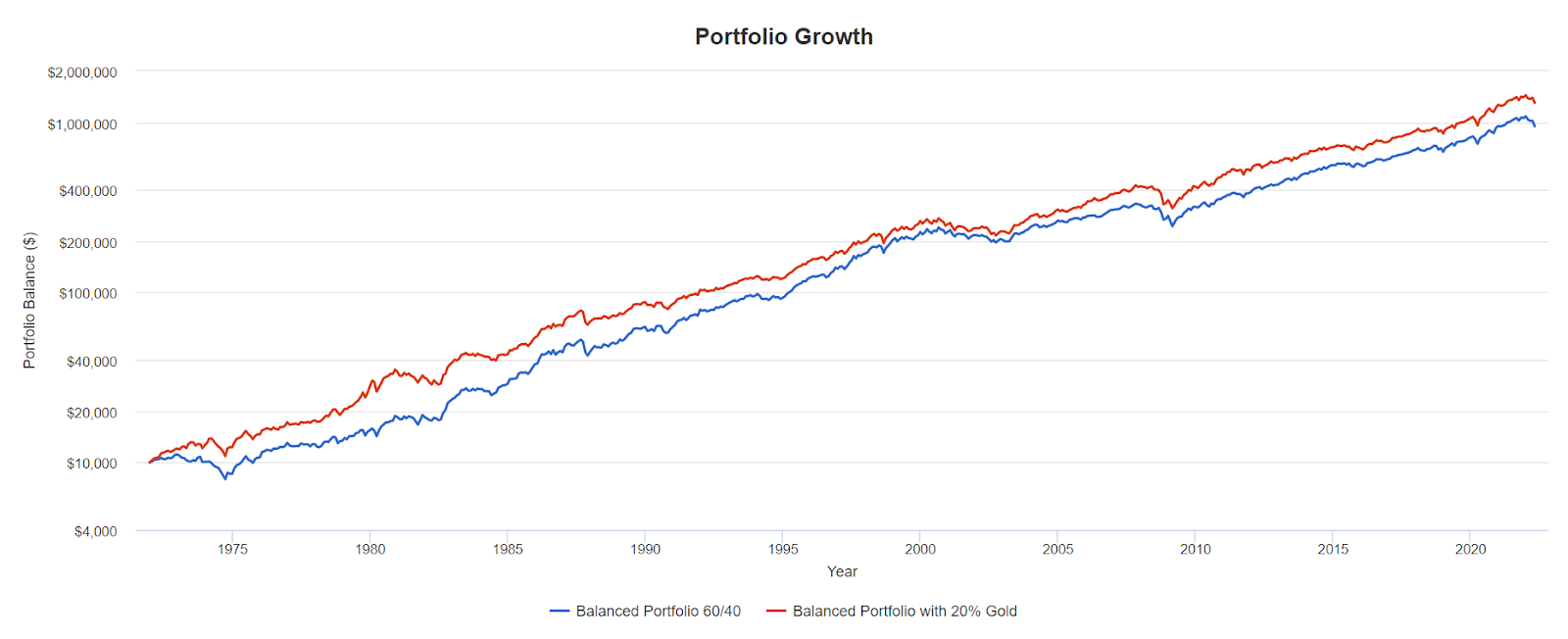

See the chart below for how a 60/40 U.S. balanced portfolio looks against a balanced portfolio with 20% bonds and 20% gold. The commodities allocation is not available on Portfolio Visualizer from 1972, so I used gold as the inflation-fighter. Gold is also known as a “safe haven asset,” as it typically performs well when stock markets correct in aggressive fashion.

Once again, whether or not to add gold and commodities is a personal call for the self-directed investor.

For my wife and myself, I hold gold, bitcoin, energy stocks, commodity stocks and commodities in modest amounts in our balanced growth portfolios, creating my own version of an all-weather portfolio. Being in semi-retirement, I need and want that financial (and emotional) protection from raging inflation or stagflation.

For those who may build their own couch potato ETF portfolio, check out the MoneySense ETF Finder Tool and the best ETFs in Canada.

MoneySense contributor Dale Roberts is a proponent of low-fee investing, and he owns the blog cutthecrapinvesting.com. Find him on Twitter @67Dodge for market updates and commentary, every morning.

In this chart, we have a look at the advanced portfolio models at the three risk levels. CAGR represents the compound annual growth rate or annualized return. I have also added Vanguard’s VBAL.TO as a core balanced portfolio benchmark.

When I compared the Advanced Portfolios in March 2022, the balanced growth portfolio was out in front, thanks to its greater allocation to stocks. That portfolio built up a nice lead in 2021. As of September 2022, the Conservative Portfolio has a slight lead, thanks to the greater allocation to the inflation fighters – that Purpose Real Asset ETF. The Balanced and Balanced Growth models are essentially tied.

And here are the returns for the portfolio assets for the same period.

See how Canadian stocks led the way on the equity front, as emerging markets (XEC.TO) are at the back of the pack. Emerging markets are under pressure due to inflation and the war in Ukraine. Also, emerging markets can perform poorly when the U.S. dollar runs strong, and it’s nearing the highs of the last 10 years.

The Purpose Diversified Real Asset ETF and real estate investment trusts (REITs) responded as expected; they thrived during unexpected inflation. That said, recently, REITs have struggled due to recession worries. The Canadian stock market did well overall, due to energy and commodities exposure. Every asset is negative in 2022, except for the real asset fund.

In an environment of rising rates, the longer-dated treasuries ZFL.TO and ZTL.V fell dramatically in price, compared to the shorter-dated bond ETF XSB.TO. The longer-duration bond ETFs have more price sensitivity to rising rates.

Here is a comparison between the Advanced Portfolio models from January 2015 through September 2022. The BMO Balanced Portfolio would have outperformed the Advanced Balanced Portfolio for this period. Once again, the inflation fighters can be a drag on portfolio performance during disinflationary times (what we experienced from 2015 to 2020).

We might be in the early innings of inflation. So, keep in mind, there hasn’t been a true test of inflation assets. Stagflation—when inflation is high and growth is slowing—can last for several years. Just look at the stagflation of the 1970s as it seeped into the 1980s (more on that later).

Investment assets have yet to see ongoing inflation or stagflation pricing, although asset performance in 2021 and 2022 is hinting at how they might react in a prolonged inflationary environment.

We are currently in a stagflationary environment. But, of course, no one knows if we are in the early stages of stagflation or if the central banks can tame inflation by raising rates—and hence, cool off price increases. From the National Post, a repost of a Financial Times article:

“The stagflationary shock of 2022 is truly global, with diverging growth and inflation expectations across most countries with many different factors exacerbating the trend in a synchronized way.

“In country after country, similar trends can be seen playing out—a surprise surge in prices and decline in activity over the past few months—as expectations for the year deteriorate.”

The period of stagflation related primarily to the 1973 oil crisis, when oil nearly quadrupled in price, lasted for several years. It’s up to you to decide whether you want additional dedicated inflation-fighters in your portfolio in case this stagflationary environment might persist.

So, how do these portfolios stack up against each other? Here’s the near-term comparison of balanced portfolio models, core versus advanced.

The BMO balanced model is down 5% since January 2021, while the advanced balanced model is now not that far behind. The market appears to be thinking that inflation might be tamed. The inflation-fighting assets began to fall in the second quarter of 2022.

If we look back to 2015, we’ll find that the core model outperforms. (I’ve substituted for long-term treasuries to create the chart with an approximation.)

Over the long run, the BMO Balanced portfolio delivered an annual return of 5.9% annual, versus 4.7% for the advanced model. We would expect the core model to outperform in a disinflationary period, or when inflation is mostly under control. If we remain in an inflationary or stagflationary environment, the advanced couch potato model should outperform the core portfolio.

All that said, there is often very little cost to adding that inflation protection, according to what I see in my research. And in most periods between the 1970s and now, adding gold, commodities and REITs as increased the performance of a balanced portfolio.

Here is a wonderful visual presentation on inflation, stagflation and deflation.

See the chart below for how a 60/40 U.S. balanced portfolio looks against a balanced portfolio with 20% bonds and 20% gold. The commodities allocation is not available on Portfolio Visualizer from 1972, so I used gold as the inflation-fighter. Gold is also known as a “safe haven asset,” as it typically performs well when stock markets correct in aggressive fashion.

Once again, whether or not to add gold and commodities is a personal call for the self-directed investor.

For my wife and myself, I hold gold, bitcoin, energy stocks, commodity stocks and commodities in modest amounts in our balanced growth portfolios, creating my own version of an all-weather portfolio. Being in semi-retirement, I need and want that financial (and emotional) protection from raging inflation or stagflation.

For those who may build their own couch potato ETF portfolio, check out the MoneySense ETF Finder Tool and the best ETFs in Canada.

MoneySense contributor Dale Roberts is a proponent of low-fee investing, and he owns the blog cutthecrapinvesting.com. Find him on Twitter @67Dodge for market updates and commentary, every morning.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Google to the moon, Meta, IBM, and Canadian railway stocks are down, automakers have a good earnings day, Verizon...

Borrowell’s co-founder and COO on the best and worst financial advice, and the biggest money lesson she’s learned from...

New analysis from the National Institute on Ageing makes a strong case for delaying Canada Pension Plan payments to...

You can still benefit from deferring Canada Pension Plan payments with less than maximum contributions.

A pattern in the markets works—until it doesn’t. Investors will be better off focusing on the fundamentals.

Two siblings’ complex inheritance provides a case study in minimizing death taxes.

Understanding industry jargon can make you a better real estate investor.

Capital gains tax inclusion rate will increase (for some), Netflix chills, U.S. bank earnings solid, and will the loonie...

Learn how the federal government’s 2024 budget can affect you and your money.

A question re BMO Balanced Couch Potato Portfolio returns shown here. The first line of returns, shown early in the article just under the first graph, shows one set of data. Just below, when comparing the same BMO portfolio with two other providers’ portfolios, you seem to show different returns for the BMO portfolio for the same periods. Am I missing something or is there a discrepency or error here? Thanks

Hi Stephen, Thank you for letting us know. The data contained in the graphic was old. We have updated the table to reflect the most recent data.