When interest rates and inflation rise simultaneously

It's happened before and it wasn't pretty

It's happened before and it wasn't pretty

Bond yields remain near historic lows with long-term Canadian government bond yields hovering near 1.7% this week. That doesn’t leave much room for error. If interest rates rise, bond prices will fall. Rising inflation could also wipe out the small gains.

More ominously, interest rates and inflation could climb at the same time like they did in the 1970s. It’s a period that older investors remember all to well and one that younger investors should learn from.

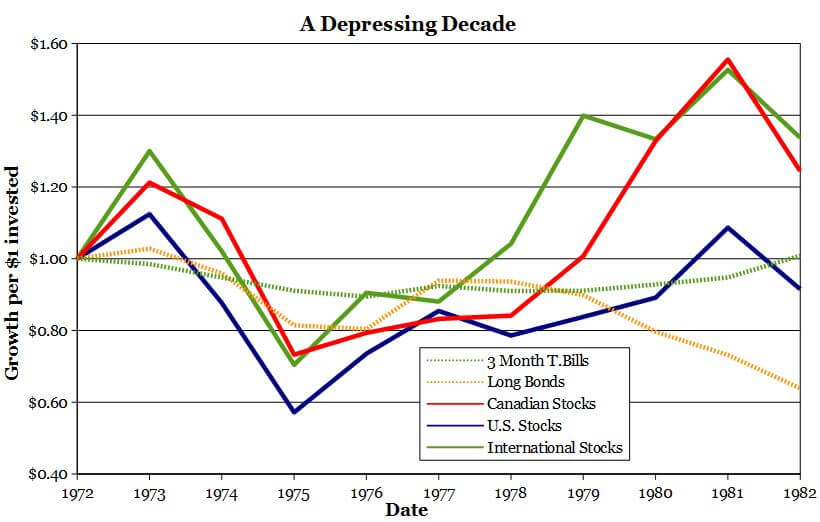

You can get a sense of how dire the situation was by examining the accompanying graph. It shows the growth (per dollar invested) of five different asset classes during the 10 years from 1972 to 1982 when interest rates and inflation climbed sky high. The graph shows annual total returns, including reinvested dividends and interest payments, in Canadian dollar terms. The returns have also been adjusted for inflation. Mind you, taxes and fund fees have not been included in an effort to avoid the overuse of anti-depressants.

Long Canadian bonds were the hardest hit. They suffered a cumulative loss of 36% over the course of the decade. But that shouldn’t come as a big surprise because bonds with long maturities tend to be very sensitive to changes in interest rates. A small rate decline will boost their prices mightily while a tiny rate increase will causes their prices to plummet.

On a more positive note, fixed-income investors who stuck with 3-month Canadian treasury bills eked out a total gain of 1% from 1972 to 1982.

Stock investors had a particularly rough time during the market crash of 1973-1974. By the end of the 10 year span, U.S. stocks (S&P 500) lost 9% while Canadian Stocks (TSX 300) gained 24% and international stocks (EAFE) climbed 34%.

A 40% bond and 60% stock portfolio with an equal amount of money invested in each asset class—rebalanced annually—would have gained a total of 14% in inflation-adjusted terms or about 1.3% annually from 1972 to 1982, before taxes and fund fees.

It was a hard period for retirees. Given the frothy state of the markets, I fear we’re heading into a similar low-return era. You might want to prepare by saving more and spending less.

Investors following the Dogs of the Dow strategy want to buy the 10 highest yielding stocks in the Dow Jones Industrial Average (DJIA), hold them for a year, and then move into the new list of top yielders.

The Dogs of the TSX works the same way but swaps the DJIA for the S&P/TSX 60, which contains 60 of the largest stocks in Canada.

My safer variant of the Dogs of the TSX tracks the 10 stocks in the index with the highest dividend yields provided they also pass a series of safety tests, such as having positive earnings. The idea is to weed out companies that might cut their dividends in the near term. Just be warned, it’s a task that’s easier said than done.

Here’s the updated Safer Dogs of the TSX, representing the top yielders as of August 23. The list is a good starting point for those who want to put some money to work this week. Just keep in mind, the idea is to hold the stocks for at least a year after purchase – barring some calamity.

| Name | Price | P/B | P/E | Earnings Yield | Dividend Yield |

|---|---|---|---|---|---|

| CIBC (CM) | $101.35 | 1.94 | 11.09 | 9.02% | 4.78% |

| National Bank (NA) | $46.77 | 1.69 | 13.56 | 7.38% | 4.70% |

| Shaw (SJR.B) | $26.39 | 2.14 | 9.56 | 10.46% | 4.49% |

| BCE (BCE) | $61.97 | 4.33 | 19.61 | 5.10% | 4.41% |

| Emera (EMA) | $47.81 | 2.01 | 14.74 | 6.78% | 4.37% |

| Bank of Nova Scotia (BNS) | $67.35 | 1.65 | 12.03 | 8.31% | 4.28% |

| TELUS (T) | $43.28 | 3.17 | 18.11 | 5.52% | 4.25% |

| Bank of Montreal (BMO) | $86.35 | 1.49 | 12.79 | 7.82% | 3.98% |

| Royal Bank (RY) | $82.23 | 1.95 | 11.95 | 8.37% | 3.94% |

| Sun Life Financial (SLF) | $41.64 | 1.37 | 12.5 | 8.00% | 3.89% |

Source: Bloomberg, August 23, 2016

Notes

Price: Closing price per share

P/B: Price to Book Value Ratio

P/E: Price to Earnings Ratio

Earnings Yield: Earnings divided by Price, expressed as a percentage

Dividend Yield: Expected-Annual-Dividend divided by Price, expressed as a percentage

As always, do your due diligence before buying any stock, including those featured here. Make sure its situation hasn’t changed in some important way, read the latest press releases and regulatory filings and take special care with stocks that trade infrequently. Remember, stocks can be risky. So, be careful out there. (Norm may own shares of some, or all, of the stocks mentioned here.)

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

The first home savings account was created to help you save more money for a home purchase. Here’s how...

Presented By

National Bank of Canada

Find out what non-registered accounts are, how they compare to registered accounts and which investments are best for non-registered...

MoneySense was born 25 years ago. This list of 25 financial innovations shows how much personal finance has changed...

Sponsored By

Embark Student Corp.

How can you choose the best ETFs for you? Watch this video before you use an ETF screener.

Find out which Canadian robo-advisor tops our 2024 list, and which robo is right for you and your investing...

Is it easy to buy and sell stocks and ETFs? Is it safe for Canadian investors? Find out the...

GICs were embraced by many Canadian investors last year, whether conservative or not. With rates expected to fall again...