Finding the right cover

Retirement planning? Decide which insurance is right for you

Retirement planning? Decide which insurance is right for you

When finance professor Moshe Milevsky teaches insurance to a new group of students, he shows the class a picture of two people, a 30-year-old and a 70-year-old, then asks: “Who needs more life insurance?” The near-term chance of dying is higher for the 70-year-old so, without fail, most students point to the senior.

Which is the wrong answer. The need for life insurance is based on the probability of a dire financial event, but “it’s the small probability that creates the need for insurance, not the high probability,” says Milevsky, who teaches at York University’s Schulich School of Business. As you can see, insurance principles can be somewhat counter-intuitive. That means it’s easy to misunderstand where insurance makes sense and where it doesn’t. As a result, you should think through your insurance needs carefully and critically. That’s especially important at retirement, where other types of insurance needs change significantly. In what follows, we’ll review key insurance products (excluding basic products such as home, auto and travel insurance) and gauge their appropriateness in retirement.

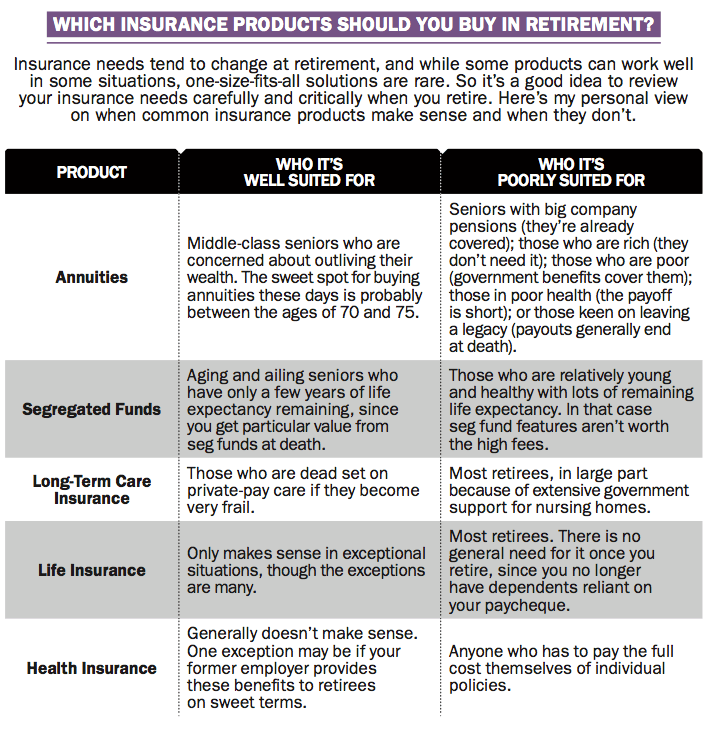

Let’s start with two investment products with an insurance aspect: annuities and segregated funds. Then we’ll move on to pure insurance products like life insurance, health insurance and long-term care insurance. (For a quick guide, check out “Which Insurance Products Should You Buy in Retirement?,” below.) In the end, you should ask yourself how you might cover the possibility of financial misfortune in old age where insurance isn’t appropriate. The simple answer: Save for it and build a healthy retirement nest egg.

You need insurance to protect yourself from the low probability of an event that is financially catastrophic. As Milevsky points out, if you buy insurance for a high probability event, the payout you would receive when the event occurs would essentially give you back the insurance premiums you paid less the insurance company’s “load,” which is composed of administrative costs, sales commission and profit. On the other hand, if the event you want to insure against isn’t catastrophic, then it’s just one of many possible everyday costs that you would absorb. While you need to budget for possible financial setbacks, it doesn’t make sense to pay insurance companies to cover them when you can save money by paying them directly and cutting out the middleman.

Of course, applying these principles isn’t always straightforward. In the world of insurance, there are lots of special situations. Also, the need for insurance is somewhat subjective. As Milevsky points out, “what is catastrophic to you isn’t necessarily catastrophic to me.”

Ultimately, think through your insurance needs for yourself. Now let’s move on to consider specific products, starting with those that mix investments with insurance.

The only insurance guide you need »

Annuities provide you with set payouts guaranteed for life. They’re another category of investments to potentially add to your portfolio alongside stocks and fixed income, and a great product for many middle-class retirees who are concerned about outliving their wealth.

Think of annuities as a bond ladder, with an insurance component that varies the length of the payouts according to how long you live. The longer you wait before buying an annuity, the higher the payout rate, and also the fewer payouts you’ll collect. Essentially, the insurance value gradually increases as you get older and as the probability of living that long decreases.

Unfortunately, annuity payouts are hurt by low interest rates. As a result, many experts say the sweet spot is to buy annuities gradually between the ages of roughly 70 and 75. That provides you with more value than if you buy at a younger age.

Segregated funds are essentially mutual funds offered by insurance companies, but they come with guarantees that ensure you’ll get the value of your original investment back if you hold the funds long enough. The fees are typically 2.5% to 3.25% a year, which is higher than mutual funds because of the cost of the guarantees. In my view, the fees are too high to justify buying seg funds in most situations.

However, the peculiar nature of the product and its guarantees make seg funds attractive for seniors who are particularly old and frail. Let me explain why that is. Typically, these days segregated funds come with one of two standard guarantees: Either you’ll get back 75% of your original investment (if you hold it for 10 years), or 100% of your original investment (but you might need to hold it for 15 years). In most situations, that doesn’t really help you much, because in the event of a big market downturn, the odds are very strong that markets will eventually recover on their own while you’re waiting for the guarantee period to elapse.

But these guarantees come with a sweetener for old folks—the guarantee applies immediately if you happen to die before the period is up. So if you’re down to just a few years of life expectancy, the value of the 100% guarantee is actually quite high, because of the high odds of hitting a market downturn without a full recovery in that time.

In addition, seg funds are paid out directly to the named beneficiaries after your death, bypassing probate. That will save you some money in probate fees, but it also saves time. Jim Otar, a financial planner and retirement researcher (retirementoptimizer.com), says segregated funds are typically paid out to beneficiaries in less than a month following a death, whereas it typically takes one to one and a half years to distribute money from investments that go through the probate process in Ontario. When a will is contested, it can take much longer, he adds.

In my view, this makes the 100% guarantee version of the seg fund a great product if your remaining life expectancy is down to a few years. It doesn’t make much sense for the young and healthy. If you do buy this product, look for funds with lower fees. Otar (who believes this product can make sense for investors younger than what I’ve described) says that if you have $250,000 to invest, you can find good segregated funds with fees of 2.1% or 2.2%, which is closer in cost to typical mutual funds.

Should I have life insurance in retirement? »

Life insurance is a core product while you’re working and have a family to support, but it doesn’t generally make sense for retirees. While your children will probably be sad to have you pass on, there’s no financial calamity to insure against. (Instead they might get a nice inheritance.) However, as Milevsky says, that general conclusion “is a good beginning to the conversation, but it doesn’t cover the many exceptions.”

Here are some circumstances where life insurance can make sense. One example occurs if you have a family cottage that you want to pass on to your kids, but you don’t have other means to pay the capital gains tax that occurs at your death. Another example is where you’re the owner or part-owner of a small business, in which case life insurance can pay the capital gains tax when you die and perhaps extract value for your beneficiaries without requiring the sale of the business. It can also make sense where you have a good pension that your spouse is heavily dependent on and the payouts to your spouse will be sharply reduced when you die.

In addition, Milevsky points out that “permanent” life insurance products with a saving and investment component allow for tax-free accumulation (known as “inside buildup”). That provides a tax-deferral opportunity if you’ve used up your TFSA and RRSP room, he says.

With long-term care insurance, you buy it and start paying premiums when you’re relatively young, in order to help cover care costs should they occur later in life. The payouts are typically triggered if you meet a particular threshold of disability (typically involving at least two of six activities of daily living: bathing, dressing, feeding, toileting, continence and transferring to and from bed). Severe cognitive impairment also typically qualifies.

The rationale for LTCI in Canada is questionable. Your eventual need for care isn’t really a low probability event—some estimates place your odds of requiring nursing home level care at 50% or higher. But the biggest issue to me is it doesn’t mesh well with government support. You may not be frail enough to qualify for LTCI payouts when you need just a little help with activities of daily living and want to move to a private retirement home (which can be expensive but isn’t government subsidized). But when you’re frail enough to qualify for LTCI payouts, you’re probably ready to move into a government-subsidized nursing home (in which case government has your back already). “It’s definitely something that you save for rather than buy insurance [for],” says Peter Benedek, of retirementaction.com.

Get the right insurance and save money »

What this type of insurance covers for retirees can vary but it often includes various health costs not covered by provincial health-care programs, such as dental costs, glasses, hearing aids and prescription drugs. People grow accustomed to this coverage as part of their benefits package at work, then wonder whether they should pay for them out of their own pocket when they retire. Your employer pays a relatively modest load factor as part of a group benefits plan, but you pay much more through an individual policy.

In addition, payouts are generally capped at relatively low levels, which means they don’t provide much help if your expenses reach catastrophic levels. If you go through an insurance company, you essentially pay the full costs through your premiums plus a sizeable markup to cover the insurance company’s costs and profit. As a result, you should view these types of costs as everyday expenses for which you should budget and pay yourself. One exception that may make these policies worthwhile is if your former employer extends coverage to retirees with a subsidized group plan.

When it comes to prescription drugs, provincial programs provide patchwork coverage, in some cases specifically for seniors, in other cases for all residents. While these programs vary widely in structure and subsidy level, generally they at least protect seniors from having to bear drug costs at catastrophic levels.

One of the best insurance products for retirees happens to be unavailable in Canada. “Longevity insurance is something that can have a big impact in ensuring people don’t outlive their wealth,” says Peter Benedek, an advocate of this product in Canada at retirementaction.com for years.

The way it typically works in the U.S. is you buy longetivity insurance (also called a deferred annuity) around the time you retire, perhaps at age 65. The potential payment from the insurance starts much later, perhaps at age 85. It’s like an annuity, except the payouts don’t start right away. As a result, you get a lot more bang for your buck in protecting yourself later on. It provides a lot of insurance value against the financial downside of living a long life.

Benedek says that the federal government needs to be the catalyst to get this product off the ground. He says Ottawa should change the rules to allow people to use some of their RRSP/RRIF money to buy longevity insurance without taxing it immediately or running afoul of RRIF minimum withdrawal requirements.

The U.S. has similar rules in place that apply to their RRSP and RRIF equivalents. A reasonable rule, says Benedek, would be to allow seniors to draw up to $125,000 or 25% from their RRIF, whichever is less, without tax consequencesto buy this product.

If that were to happen, and you were to live a long life and start receiving payouts later, they would then be fully taxable just like a regular RRSP/RRIF withdrawal. That way seniors get longevity protection and the government still gets its tax money.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Surging auto insurance rates squeeze drivers, fuel inflation.

Canadians are travelling the world for concerts and other events. Here’s how to see the Eras Tour abroad—maybe for...

Tech industry warns that the budget's capital gains proposals could cause “irreparable harm.”

Insurance is high on frequently stolen vehicles. Here’s how to reduce your premiums.

These impressive travel cards can help turn your everyday spending into flights, hotels and more.

When you die, capital gains tax might apply to some of your assets. Can life insurance help shelter your...

What is car insurance, how much does it cost, and how can you find the best coverage for your...

Created By

Kruzee

Average asking rent prices reach $2,193 in February, up 10.5% from 2023.