Making sense of the markets this week: November 24, 2024

Nvidia doubles revenue in one year, Canadian inflation moves in the wrong direction, Target misses badly, Walmart beats earnings expectations, and Canadian grocery store stocks are up big.

Advertisement

Nvidia doubles revenue in one year, Canadian inflation moves in the wrong direction, Target misses badly, Walmart beats earnings expectations, and Canadian grocery store stocks are up big.

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

Nvidia is now the world’s largest company. You know it’s growing quickly when there are massive Super Bowl-level parties for its quarterly earnings calls. It seems that no matter how high expectations get for the stock, the unprecedented growth of profits just continues to clear the projected earnings bar. At this point, I’m not sure anything can stop the chip-making super conglomerate.

All numbers are in U.S. dollars.

While share prices were down about 2% in after-hours trading on Wednesday, they’re still up more than 200% in 2024. It seems the tech industry just can’t get enough of Nvidia’s one-of-a-kind semiconductor chips. Given how profitable tech companies are, there appears to be a nearly-infinite amount of money to spend on the hardware that will power the infrastructure of the AI age.

Here’s how Nvidia rose so high and so fast:

CEO Jensen Huang stated in the earnings call that, “Almost every company in the world seems to be involved in our supply chain.” That might be an exaggeration—but still, who says that?!

Nvidia’s new Blackwell chip has begun shipping to AI heavyweights like Microsoft, Oracle and OpenAI. Its CFO Colette Kress said, “Both Hopper and Blackwell systems have certain supply constraints, and the demand for Blackwell is expected to exceed supply for several quarters in fiscal 2026. In other words: “We’re selling these things faster than we can make them, and we can make a lot.”

The financial fundamentals behind the rise of Nvidia are a great counter to the “bubble” argument. Back in 2000, during the Dot-Com Bubble, there were some crazy stock-rising stories. The market capitalization of Pets.com went from $300 million to $0 in less than a year. The thing is, Pets.com never made any actual money. (It’s kind of like Truth Social in a way.) Nvidia just made $19.3 billion in three months! (After making $9.24 billion during the same quarter a year ago.)

I have no idea what the fair value of an incredibly profitable company like Nvidia should be. But until another chipmaker can start stealing away a chunk of the market share, it appears that an incredible amount of the tech world’s profits will eventually find their way into Nvidia’s coffers.

Read more:

Get up to 3.00% interest on your savings without any fees.

Lock in your deposit and earn a guaranteed interest rate of 3.50%.

Open a High Interest Savings Account right now and earn 4.60% interest for 5 months. Only on eligible deposits up to $100,000.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

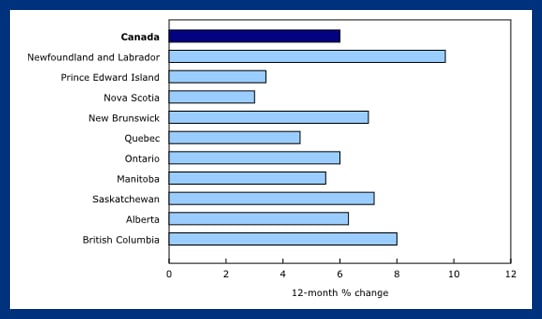

While falling gasoline prices led to a moderate 1.6% annual inflation rate in September, Statistics Canada revealed that October’s annual inflation rate had ticked back up to 2%.

Even though gas prices continue to fall, food and shelter make up such a large amount of what Canadians spend, they dominate the overall inflation picture. Shelter makes up 28.6% of what Canadians spend, and food has now increased to 16.7%. Consequently, while items like clothing and transportation aren’t really going up, food and shelter pull up the annualized average to 2%. The inflation rate for shelter is coming down slowly, but it continues to be a pain point for many Canadians.

| CPI tems | September 2024 | October 2024 |

|---|---|---|

| All | 1.6% | 2.0% |

| Food | 2.8% | 3.0% |

| Shelter | 5.0% | 4.8% |

| Household operations, furnishings and equipment | -0.2% | -0.1% |

| Clothing and footwear | -4.4% | -2.3% |

| Transportation | -1.5% | 0.2% |

| Health and personal care | 3.1% | 3.1% |

| Recreation, education and reading | 0.0% | -0.9% |

| Alcoholic beverages, tobacco products and recreational cannabis | 3.0% | 3.0% |

While prices for services rose at an annual rate of 3.6% in October, prices for goods were up just 0.1%. (Generally speaking, service would include items such as haircuts, housekeeping services, or dental care. Goods would be everything from TVs to shoes.) Property tax increases are always a focus of the October inflation report, since that is when they are recalculated each year. This year, property taxes rose 6% (compared to a 4.9% increase last year).

This inflation increase is going to make it harder for the Bank of Canada (BoC) to justify large interest rate cuts going forward. If inflation remains stubbornly high, we may see the BoC scale back on its forecasted interest rate cuts. Given the U.S. election results that we commented on last week, “higher for longer” interest rates may very well be the new probable path forward.

One of the biggest surprises on Wall Street this week was the massive earnings miss by Target. Shares were down 21% on Wednesday after Target revealed it is having difficulty generating sales revenue despite a heavy discounting strategy.

It’s been a big week for big U.S. corporate retailers. All numbers below are in U.S. dollars.

Target CEO Brian Cornell blamed the bad quarter on “lingering softness in discretionary categories,” as well as poor inventory management. Target incurred increased shipping costs as it paid high fees to rush goods into its warehouses ahead of the port strike in October. These costs, combined with flatlining demand, led to a costly inventory build-up. Shares are now at a 52-week low.

In stark contrast to the large earnings miss by Target, its big blue competitor continued to show why it is best-in-class. Walmart beat earnings—yet again—and showed the financial consistency that investors love. Aside from better inventory management, the biggest reason for Walmart’s higher sales numbers likely relate to the different product mixes of the two retailers. At this point, Walmart is a massive grocery store with a large everything-else-store attached, as 60% of Walmart’s U.S. business is groceries (while only 23% of Target’s sales are groceries).

While online sales were up 10% for Target, they were up 22% for Walmart. Walmart Chief Financial Officer John David Rainey stated that customers continued to be “focused on price and value.” He added that tariffs could force Walmart to increase prices, but that it was too soon to say what merchandise would feel the tariff pinch the hardest.

Shares of Lowe’s dropped about 3% on Tuesday when it announced an earnings beat, but a slight miss on revenues. CEO Marvin Ellison said that management believes customers are delaying home improvement projects until rates have finished coming down. They anticipate sales to pick up in 2025.

After a couple years of bad headlines, grocery stocks have had an excellent 2024.

Two of Canada’s largest grocery chains reported their earnings this week.

Despite these two grocery retailers beating earnings and revenue projections slightly, the share prices of both dropped slightly after announcing earnings.

Metro’s $1 billion supply chain investment is coming to completion. And Metro’s CEO Eric La Flèche commented, “This transformation will provide capacity for future growth and efficiency while strengthening our market position. With the significant investments in the modernization of our supply chain behind us, we are well-positioned for growth to create long term value.” Note: A labour strike in the third quarter cost Metro about $27 million, after tax.

George Weston saw its Loblaw retail subsidiary slightly increase revenues year over year. Loblaw makes up the vast majority of George Weston’s holdings, and includes not only the Loblaws-braded grocery stores, but all also discount grocery chians as well.

Another George Weston subsidiary, Choice Properties Real Estate Investment Trust, has a more nuanced earnings story. It reported strong operation results for the quarter, as rental rates rose from retail and industrial clients. However, one-time adjustments to earnings showed a massive decrease of $595 million (97.5%) in fair value adjustment of Choice Properties’ Trust Unit liability.

Basically, the real estate trust subsidiary has been doing better than it did last year and, consequently, it’s valued more now than it used to be. Because it’s now worth more, the former tax write-off of $610 million is now a tax write-off of only $15 million. All and all, it was mostly just creative accounting that was largely forecasted in advance, as proven by the lack of volatility in the stock price.

George Weston’s share price has done quite well this year and is up almost 33% in 2024. Metro is up just over 27% by comparison.

You can see how both grocery conglomerates stack up against other Canadian retail stocks as MillionDollarJourney.com.

Share this article Share on Facebook Share on Twitter Share on Linkedin Share on Reddit Share on Email

Which ETFs should you invest in? Which ones best suit your risk tolerance? What about personal ethics? Check out...

Copper production lifted First Quantum, while Intact faced higher catastrophe claims. Catch up on the latest quarterly results from...

A reader just wants an assessment of her and her husband’s finances. Turns out that’s the cornerstone of financial...

Dividend ETFs do not guarantee market-beating returns. They boost your portfolio thanks to factor exposure and behavioural benefits.

Nearly one in four Canadians say they or a family member fell victim to a scam in the past...

Find the best GIC rates in Canada. Plus, everything you need to know about how they work.

From home office costs to travel expenses, discover the tax deductions employees may qualify for and how to claim...

Rogers' latest deal weighed on earnings, while Teck benefited from stronger copper markets. Here's the full roundup

Before buying a home in Canada, U.S. citizens should understand the cross-border tax and ownership rules that can have...

Why do we know we're overpaying and still do nothing about it? A personal look at loyalty, inertia, and...