By Kyle Prevost on August 30, 2024 Estimated reading time: 8 minutes

Making sense of the markets this week: September 1, 2024

By Kyle Prevost on August 30, 2024 Estimated reading time: 8 minutes

Did Nvidia fail to meet expectations? Plus, why National Bank is a star among the mixed bag of Canadian bank results, Couche-Tard’s plans to make international acquisition history, and stock markets in 1900 versus today.

This article is 1 year old. Some details may be outdated.

Advertisement

Photo by 何 夏 from Pexels

Kyle Prevost, creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course, shares financial headlines and offers context for Canadian investors.

Advertisement

Advertisement

Nvidia earnings land on the moon—shareholders were aiming for the stars

Pretty much any other company in the world would be thrilled to post Nvidia’s quarterly earnings numbers, but right now Nvidia isn’t “any other company.”

Nvidia earnings highlights

All numbers below are in USD.

Nvidia (NVDA/NASDAQ): Earnings per share came in at $0.68 (versus $0.64 predicted), while revenues totalled $30.04 billion (versus $28.70 billion predicted).

Revenues were up 80% year over year. Net income was up 268%. Nvidia has so much extra revenue, it spent $50 billion to repurchase its own shares.

Despite the growth and overall earnings numbers, Nvidia shares were down 7% in immediate after-hours trading after the Wednesday close. It fell 6% on Thursday but was up 1.3% before trading began Friday. Other AI-linked chip stocks slipped in sympathy Thursday morning, with AMD, Broadcom and Micron falling 1.6 to 2%.

Nvidia is still up 150% year-to-date and more than 900% since the end of 2022. But it’s interesting to see the company’s expectations finally overshoot its ability to produce unprecedented profits. There are no large-cap stocks in the world that have had the meteoric rise that Nvidia has realized over the past few years. And, consequently, no other company’s shareholders have the same unquenchable thirst for record growth.

Nvidia CEO Jensen Huang said the company is on pace to meet its ambitious production targets for the new Blackwell chip technology, calling anticipation for the technology “incredible.”

While gross margins slipped to 75.1% from 78.4% last quarter, they’re still up from 70.1% a year ago. That level of gross margin is astounding. For context: A company like Canadian National Railway, which operates in an oligopoly and has one of Canada’s highest gross margins, comes in at around 41%. Canadian conglomerates like Enbridge and Telus come in at 17% and 9%, respectively.

Overall, it appears to be a case of analysts being tired of looking uninformed at every earnings call, as Nvidia’s ability to produce profits raced past their expectations. They have finally adjusted for this breakneck speed at which the company is growing, and now quarterly earnings predictions will have to normalize a bit going forward.

MoneySense is an award-winning magazine, helping Canadians navigate money matters since 1999. Our editorial team of trained journalists works closely with leading personal finance experts in Canada. To help you find the best financial products, we compare the offerings from over 12 major institutions, including banks, credit unions and card issuers. Learn more about our advertising and trusted partners.

Banks are less scared of Canadian defaults

Last week TD reported its earnings, and while its Canadian-based revenues were very strong, those fundamentals were overshadowed by U.S.-based penalties. This week, Canada’s other five big banks reported earnings.

Canadian banking highlights

Here’s how Canadian banks performed in the three months ending July 30, 2024:

Bank of Montreal Financial Group (BMO/TSX): Adjusted earnings per share of $2.64 (versus $2.76 estimated by analysts) and revenues of $8.19 billion (versus $8.24 billion estimated).

The Bank of Nova Scotia (BNS/TSX): Adjusted earnings per share of $1.63 (versus $1.62 estimated) and revenues of $8.36 billion (versus $8.53 billion estimated).

Royal Bank of Canada (RY/TSX): Adjusted earnings per share of $3.26 (versus $2.95 estimated) and revenue of $14.63 billion (versus $14.37 billion estimated).

Canadian Imperial Bank of Commerce (CIBC/TSX): Earnings per share of $1.93 (versus $1.74 estimated) and revenues of $6.60 billion (versus $6.27 billion estimated).

National Bank of Canada (NA/TSX): Adjusted earnings per share of $2.68 (versus $1.80 estimated) and revenues of $2.98 billion (versus $2.86 billion estimated).

While National Bank and RBC again proved why they are considered “best in class” as Canadian banks, the through line of the last quarter was that several banks had to set aside less money than expected in order to cover bad loans—provisions for credit losses (PCLs).

For example, CIBC had a good earnings report after its PCLs totalled $483 million, which was down $253 million from last year. That’s an automatic $253-million boost to its bottom line, and it indicates the bank isn’t as worried as it was last year in regards to Canadians defaulting on debts. While RBC’s $659 million in PCLs was a bit higher than last year’s $616 million, it was down substantially from last quarter’s $920 million, and it was well below analysts’ expectations. National Bank posted similar PCL numbers relative to last year. On the other hand, BMO set aside $906 million for PCLs, much higher than last year’s $492 million. Similarly, Scotiabank had to set aside $1.05 billion, higher than last year’s $819 million. Much of Scotiabank’s underperformance can be accredited to its Latin America banking assets.

It appears that Canadian investors and those abroad were paying close attention to those bottom lines. CIBC and National Bank saw 6.45% and 5.86% boosts to their share prices after quarterly earnings announcements. RBC and Scotiabank were both up a little over 2%. BMO was the laggard of the group, with its share price falling 6.45% after its earnings announcement.

With RBC successfully integrating HSBC Canada’s assets into its firm, the Canadian banking scene now looks towards next week’s shareholder decision on National Bank’s proposed takeover of Canadian Western Bank. Shares are up 23% already this year (after taking a brief dip on the news they were willing to pay a large premium to secure the CWB deal), and it appears that the market is satisfied that National Bank will be able to unlock value as it attempts to expand into western Canada.

Because I grew up in near Winnipeg, the Slurpee Capital of the World, I thought I knew everything the 7-Eleven universe had to offer. Then, I visited Japan and Thailand last year. I realized that I hadn’t seen anything yet. (All figures in U.S. dollars in this section.)

In much of Thailand and Japan (among other places in Asia), the convenience store is a daily touchstone stop. In Tokyo, there are more than 3,000 7-Eleven stores, a large part of the country’s 56,000-plus convenience store locations. While 7-Eleven was a big part of my childhood, it pales in comparison to the role it plays within many Asian communities.

So, it quickly caught my attention when Canadian corporate darling Alimentation Couche-Tard (ATD/TSX) announced it was making a friendly takeover bid for Tokyo-based Seven & I Holdings Co (SVNDY/NIKKEI). The possible deal is historic for many reasons.

The acquisition of Seven & I Holdings Co is the largest-ever Japanese target of a foreign buyer.

It’s the first test of new 2023 takeover rules by Japan’s Ministry of Economy, Trade and Industry (METI), designed to make foreign acquisitions more welcoming and Japanese companies more internationally competitive.

It would likely top Enbridge’s $28 billion acquisition of Spectra Energy Corp back in 2016, to become Canada’s largest-ever corporate takeover.

It would combine Couche-Tarde’s convenience store empire of 16,700 stores in 31 countries, with 7-Eleven’s 85,800 stores in 19 countries.

By combining ATD’s and 7-Eleven’s U.S. market share, Couche-Tard would control more than 12% of the U.S. convenience store market, with the closest competitor being Casey’s General Stores at only 1.7%.

It’s a massive bite to take for ATD, currently valued at about $56 billion, since 7-Eleven is currently worth about $38 billion.

The potential acquisition is so large that many analysts believe ATD would have to raise $18 billion in new equity to complete the deal. That would be the biggest stock offering in Canada by a wide margin. It would also be in addition to the $2 billion in cash on hand ATD has, and its ability to borrow about $20 billion. There’s speculation that Canadian pension plans would be a key source of capital in order to get a deal done.

Neither company disclosed the precise terms of the deal, but Couche-Tard described the offer as “friendly, non-binding.” That’s a key differentiator from a “hostile takeover.” (A hostile takeover is when a company tries to purchase more than half of another company’s shares on the free market against the wishes of the targeted company’s management, thus taking over operational control.)

This move is not totally out of the blue for ATD, as the company has taken big acquisitional swings before. The Quebec-based operator has a long history of successfully integrating new acquisitions. Its attempt three years ago to purchase French grocery chain Carrefour for $25 billion was scuttled at the last minute by the French Finance Minister citing food security issues. Similar protectionist governmental instincts could prevent this massive deal from getting done.

That said, Couche-Tard has been circling (Circle K-ing?) 7-Eleven for over two years now. Perhaps it believes it has what it takes to navigate the new Japanese corporate legal waters and get the deal done.

While there will likely be some nervous customers of 7-Eleven (nobody wants to see change at their favourite corner store), Seven & I Holdings’ shareholders must be happy. Shares were up 22% upon announcement of the proposed acquisition.

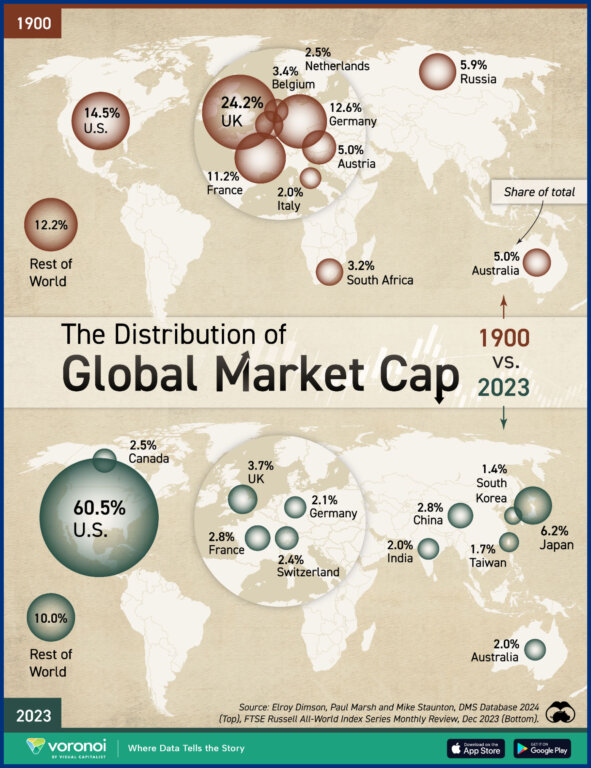

It’s always worth keeping the long run in mind when thinking about trends and market forces. When we consider just what an incredible run the U.S. stock market has achieved over the last few years, it’s important to remember that it’s unlikely to continue that outperformance forevermore.

You can see that the U.K.’s relative dominance of the world’s stock markets at the time still doesn’t even come close to the U.S.’s share today.

The sun never sets on the Nvidia/Apple/Microsoft/Google Empire.

In 1900, the largest companies were primarily railways. Today, Union Pacific (the largest railway company in the world) is only the world’s 98th biggest company by market cap. And, interestingly, Canada’s two big railways are number two and three on the list respectively. Get off the tracks when AI companies are coming through…

While today’s tech giants may seem unstoppable, remember that, at one point, railway dominance felt similar.

As a whole, we see that Europe’s share of the world’s stock markets has fallen from 67% in 1900 to just over 11% today. We don’t think it’ll take 123 years for India’s and other Asian stock markets to take an increasing share of world commerce.

Kyle Prevost is a financial educator, author and speaker. He is also the creator of 4 Steps to a Worry-Free Retirement, Canada’s DIY retirement planning course.